Housing Affordability Remains a Thorny Problem

Finding a Way Home

By Jeffrey Liguori

In many ways, the U.S. economy is still dealing with the effects of the global financial crisis of almost two decades ago. It was a massive reset of our entire financial system, with one segment, residential real estate, still evolving from that disruption.

The boom of housing and real estate prices, exacerbated by exotic derivative investment vehicles tied to mortgages of borrowers with poor credit, led to an historic bust in the real estate industry. Following the crash, banks significantly tightened up their lending standards, and home building, illustrated by housing starts, collapsed as demand for new homes evaporated.

Consider this: the number of new housing units rose from roughly 1.65 million to a peak of 2 million per year from 1999 to 2005 before contracting to fewer than 500,000 in 2009. By contrast, the number of 20- to 30-year-olds in the country, the typical first-time homebuyer, which drives much of the market, increased from 72 million to 78 million from 1990 to 2000. And while that is a modest increase of about 8% over a decade, the growth in that cohort of the population grew by nearly 40% in the prior decade, from 1980 to 1990.

Jeffrey Liguori

“When the Fed raised rates to fight inflation from 2022 to 2024, mortgage costs climbed rapidly, and higher rates reduced the number of homeowners willing to sell or upgrade. Contrary to economic theory, supply shrank while demand stayed high, putting home ownership out of reach for many.”

The combination of population growth and a booming economy prior to 2007 worsened the housing availability issue, which was already running short of demand. The economic downturn simply put that supply and demand imbalance on hold. Until COVID.

Today, housing affordability remains a significant problem. COVID stimulus and the shift to remote work caused demand to surge, driving up prices. When the Fed raised rates to fight inflation from 2022 to 2024, mortgage costs climbed rapidly, and higher rates reduced the number of homeowners willing to sell or upgrade. Contrary to economic theory, supply shrank while demand stayed high, putting home ownership out of reach for many.

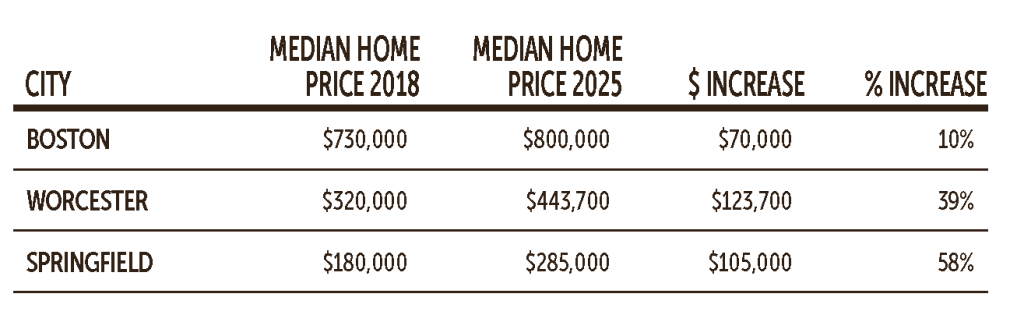

Individuals and families at the lower end of the economic scale are at a greater disadvantage, consistent with our bifurcated economy, as illustrated here:

Recently, President Trump proposed the idea of a 50-year mortgage as a solution to the housing affordability problem. The concept may have originated from Bill Pulte, director of the Federal Housing Finance Agency (FHFA), who has strong ties to the homebuilding industry. Pulte’s grandfather, William Pulte, founded Pulte Homes, now the third-largest home builder in the U.S., with annual sales exceeding $17 billion.

The FHFA is central to residential real estate as an overseer of the mortgage market and conservator of Fannie Mae and Freddie Mac, which protects taxpayers and maintains the stability of the housing finance system. The FHFA, with its access to valuable data and policy tools, is in a unique position to help alleviate the issue.

Extending the term of a mortgage from 30 to 50 years means lower monthly payments for the borrower. To put affordability in perspective, prior to the pandemic, the median home price in the U.S. stood at approximately $260,000, with a 30-year fixed mortgage rate averaging 3.8% and 20% down, resulting in monthly payments near $1,200. Currently, the median price has risen to about $420,000, while mortgage rates have increased to around 6.4%, pushing monthly payments above $2,100.

This means the cost of purchasing a typical home today is more than double what it was before the pandemic and requires significantly more cash down. The cost has put buyers on the sidelines. But the persistent shortage of supply has kept prices stable at historically high levels. J.P. Morgan estimates there is a shortage of almost 3 million homes, which could take a decade to resolve.

The chief economist for the National Assoc. of Realtors, Lawrence Yun, says the “small savings” on monthly payments for a 50-year mortgage has tradeoffs. For one thing, building equity in one’s home, often the largest asset to most families, would take considerably longer.

According to Yun, “it would also take almost 40 years to pay off half the balance, meaning most borrowers would not begin building meaningful equity until the final decade.” Which simply reinforces the current problem of existing homeowners not trading up because financing costs are too high. It is unlikely that someone would use their current equity and take on a loan for another 50 years just to be able buy a nicer home at the same monthly cost.

And what if this type of mortgage sparks demand for homebuyers? Without greater supply, it will undoubtedly drive up prices, thus not solving the affordability problem at all.

Analysts say that, to implement a 50-year mortgage, Trump would need Congress to repeal the law that prohibits government-backed loans with terms longer than 30 years. Some believe regulators have the executive authority to create this type of loan.

Jim Millstein, who served as the Treasury Department’s chief restructuring officer from 2009 to 2011, noted that “a lot of so-called innovations occurred to make mortgages more affordable prior to the financial crisis. It proved to be a disaster.”

Time will tell if this is a crisis in the making or the start of a solution to the housing problem.

Jeffrey Liguori is executive vice president of Bradley Foster & Sargent Inc.