The Basics of IRMAA

By Erica Beaudry

I’ve previously written articles about some of the basics of Medicare, like “Navigating the Medicare Maze,” in which I introduced the concept of working with an independent broker such as myself to help guide you through the enrollment process, or “Medigap vs. Medicare Advantage: What’s the Big Deal?” which looked at how both Medigap and Medicare Advantage plans can be fortification tools that help limit the liabilities one is exposed to when covered by Original Medicare (the red, white, and blue card) alone.

Erica Beaudry

“The Social Security Administration determines you owe an income-related monthly adjustment amount, it will send you a notice for the amount of your new premium and the reason for its determination.”

Today, we break down IRMAA, or the income-related monthly adjustment amount, which some folks pay for their Medicare Parts B & D coverage.

IRMAA is a surcharge that is determined by the Social Security Administration and is based on income reported two years prior. The amount is calculated annually, so if your income changes, so might your IRMAA.

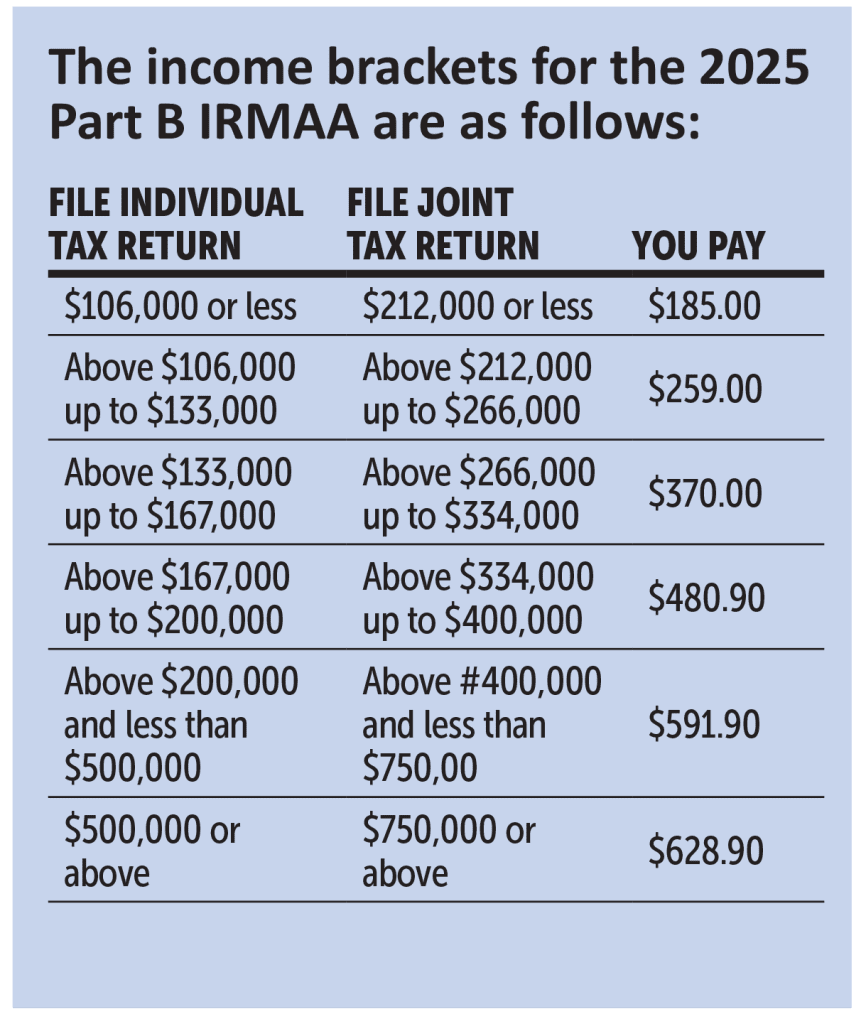

The base rate for Medicare Part B in 2025 is $185. Depending on your modified adjusted gross income as reported on your IRS tax return from two years ago, you may have to pay the standard Part B premium and an income-related monthly adjustment amount.

If the Social Security Administration determines you owe an income-related monthly adjustment amount, it will send you a notice for the amount of your new premium and the reason for its determination. If you disagree with that determination, you have 60 days from the date of notice to appeal. Life changing events such as loss of income, death of a spouse, marriage, or divorce could be grounds for a redetermination, as well as inaccurate or outdated tax information.

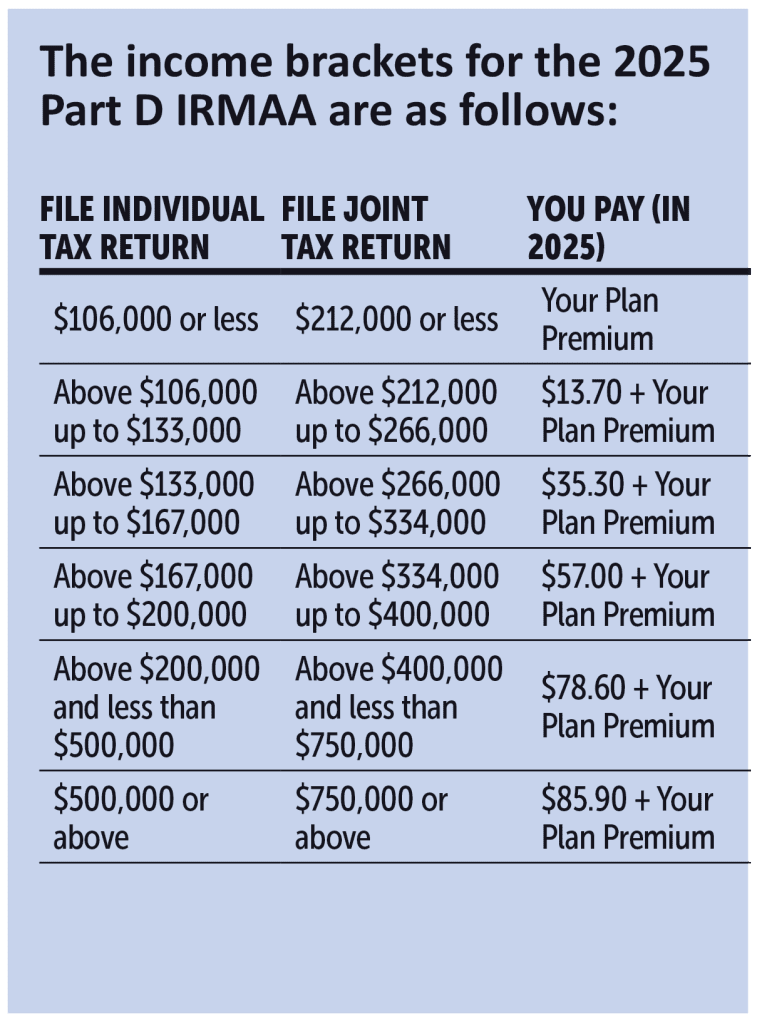

IRMAA also comes into play with your Part D, or drug coverage. The same set of parameters are used to calculate the surcharge for Part D. The important part to remember is that the Part D IRMAA is in addition to any premiums associated with your Part D coverage, but is paid directly to the Social Security Administration the same way you pay for your Part B premiums.

A couple of scenarios worth mentioning that can affect your income-related monthly adjustment amount are the sale of a primary real estate property or winning the lottery. Both life events will increase your income for the year they occur in and may therefore result in an IRMAA surcharge two years later. Both life events are generally not appealable, meaning that you are more likely to lose an appeal filed on the grounds that your income increased in any given year due to these events occurring. With real estate properties, some exceptions are made when the property has been income-producing.

If your head feels like it is spinning after reading this, don’t worry. Take the headache out of understanding Medicare by working with a professional such as myself who will help you sift through all the details that come with enrollment and coverage.

Independent Medicare specialists do not work for the insurance carriers. Instead, we provide an independent, unbiased view of insurance options available to seniors and Medicare recipients at no cost to the people we serve. We focus on Medigap, Medicare Advantage, and prescription drug plans.

Our service to you doesn’t end when you enroll in a plan. We live in your community and are here to answer your questions on bills, drug plans, provider services, extra benefits, and much, much more year-round.

Erica Beaudry is a local, licensed, independent insurance broker with EA Financial Solutions, focusing on Medicare. She does not work for and is not affiliated with Medicare. She can be reached at [email protected] or (413) 626-9906.