Life Savers

St. Germain Investment Management Gets Personal

When gauging the reputation of St. Germain Investment Management, Tim Suffish says, one measure is the number of non-clients who call out of the blue.

When gauging the reputation of St. Germain Investment Management, Tim Suffish says, one measure is the number of non-clients who call out of the blue.

“It happens all the time,” he said. “People call with questions, and we just give the advice. We’re more than happy to take the calls. It’s a sign that the company is doing things right when random people call us and are reaching out for something. They’re always shocked and appreciative when one of the financial advisors spend time on the phone with them with no expectation of anything in return.”

Suffish, the firm’s senior vice president of equity markets, said it’s a reflection of the name St. Germain has built in Greater Springfield for the past 90 years. But the company, launched by D.J. St. Germain in 1924, hit some, well, depressing times in its early days.

“D.J. did fantastic with his investments the first five years. Then 1929 came along and wiped out a decent portion of his net worth,” said Mike Matty, the company’s current president, adding that surviving the Great Depression sparked the firm’s long-standing focus on investing conservatively.

“He realized that not losing an investment is every bit as important as making money. That has guided our conservative philosophy, and it’s the way we continue to make money,” Matty said. “During the most recent downturn, eight or nine people said to us, ‘we know we’re not going back to the old highs,’ and yet, this week, we’re at new highs. We hit a billion last year in assets under management.”

Matty, however, prefers to talk about people, not numbers, when considering how St. Germain has grown since the days of D.J.

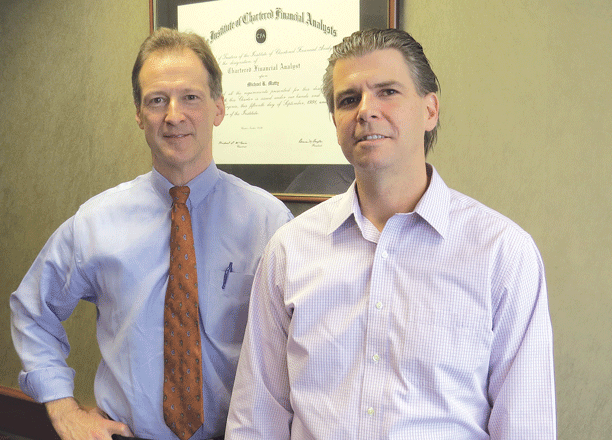

Mike Matty, president of St. Germain Investment Management

Suffish said there’s a certain satisfaction that comes with helping clients — whose only exposure to retirement savings to that point might be a company-sponsored 401(k) plan — really think about what they want from their golden years.

“They’re thinking about retirement, planning to leave their job and go from earning and putting money away for retirement to taking money from their retirement account,” he said. “It’s huge. People who haven’t gone through it don’t realize how … not traumatic, necessarily, but how serious it is, and the consideration and planning that goes into it.

“Once you’re into retirement, you want to make the most of it, so you don’t outlive your money,” he went on. “That’s our meat and potatoes; the most important thing we do is sitting down and talking with clients, people entrusting us with everything they have to last them through their last days.”

Human Touch

Matty said St. Germain had long been known strictly as an investment manager, but about a decade ago, the company began to broaden its scope to all-around financial planning.

“We now do comprehensive financial planning with people. We take a look at where their income streams are in retirement; are they adequately covered? And we’re the go-to call for people on other financial questions — buying a car, refinancing a house, whatever it may be, we get a call. That’s worked out very well for us.

“Life has gotten much more complicated these days,” he continued. “People get exposed to an immense amount of information overload on the Internet. Can you sit down and Google it? Sure, but you’ll see 150,000 results. People say to us, after trying to figure it out on their own, ‘I want to talk to someone who actually walks the walk before I do this.’ That’s what we’re great at.”

Mike Matty, left, and Tim Suffish say their most important job is talking one-on-one with clients and understanding their expectations for life after retirement.

Suffish said a client was in reviewing his account recently and saw a photograph of D.J. St. Germain with a 1930s-era Packard. “He said, ‘I remember going for a ride in that car.’ The company has been here a long time, and the experience has been consistent. People change sometimes, but the St. Germain way keeps people here a long time.”

Still, the company has experienced a growth spurt in the past decade. When Suffish came on board in 2004, he was the seventh employee; now 20 people work there. But that growth has not come at the expense of the personal touch that has long been a priority.

“When people pick up the phone and call us, they get a receptionist, not voice mail. An automated voice drives people crazy,” Matty said. “It’s one of many small touches, one of the things that sets us apart from a lot of other financial firms out there. If you’ve got a half-million parked with a big brokerage firm, you’re a cog in the wheel there. To us, you’re a client. You’re going to hear from us, and we want to hear from you. You’re not just a nameless, faceless account number. We want to get to know you.”

And know your partner as well — even if that meeting comes late in the game.

“In a lot of cases, one spouse will open an account,” he said, and after that client dies, “we almost become a surrogate spouse for the survivor because they know nothing about the household finances.”

In such cases, the survivor’s concerns often boil down to one simple question.

“They ask, ‘can I live in the lifestyle I know now? That’s all I need to know.’ They don’t want to talk about realized gains versus unrealized gains. They say, ‘I’m a machinist. I’m hiring you guys to manage the money because that’s what you do.’

Such clients appreciate a conservative approach that stays the course, Matty said. “To us, the name of the game is giving people most of the upside and preventing them from losing much on the downside. More people get scared out of the market by losses than pulled into it by greed. And they pull out at exactly the wrong time.”

Age-old Concerns

Matty said a client’s age plays a factor in asset allocation, or what percentage of money is tied up in stocks, bonds, and other vehicles.

“We’ve extended out in the past few years beyond just a conservative stock philosophy,” he added, noting that equity-income accounts — a type of mutual fund that invests in companies with a history of solid dividend payments — have become a prominent part of the roster.

“Even with what we do on the management side, making sure we build a diverse portfolio, those types of stocks are still going to be a bumpy ride,” Suffish said. “When there’s a scare overseas or interest rates do something funny, those stocks will move around a bit.” But, he added, building a portfolio that focuses on income generation through dividend growth is a good fit for many clients.

Beyond that, conventional wisdom on asset mix has shifted over the years, he said. It used to be that subtracting one’s age from 100 gave the recommended percentage of assets in stocks. Now, it’s closer to 120 minus one’s age.

“But everyone is unique,” he added, and financial advisors must take into consideration factors like Social Security projections, pensions, retirement-account balances, expected inheritance, and overall lifestyle expectations.

“If somebody is 75 years old and has all their needs met by income sources like pension and Social Security, that client can afford to be more invested in stocks,” Suffish said. “The most important thing at St. Germain is the conversation between the financial advisor and the client. It’s not like picking Coke over Pepsi; that’s a very small factor. The most important thing is the conversation between the financial advisor and the client, us knowing them and their situation, and getting the financial mix right.”

It’s definitely a more complex financial world, Matty said.

“Fifty years ago, when you turned 65 years old, you could rely on Social Security and probably had a pension. Life expectancy was not a whole lot longer after retirement, and you had some pretty reliable income sources. People had more homogeneity,” he told BusinessWest.

“Now, we have 65-year-olds taking up skiing. They plan to live 30 more years. People are saying, ‘I don’t think Social Security is going to be there for me.’ Virtually no one has a pension anymore. There’s no homogeneity,” he went on. “A client might say, ‘I’ve got aged parents, and I’m taking care of a special-needs son, who will probably live with me forever. And there’s longevity in my family; people live into their 90s.’ Everyone is unique. In these circumstances, we really need to spend time getting to know you.”

Clients run the gamut, Matty said, from individuals with accounts large enough to grab the attention of a larger firm to people who have worked hard their entire lives to amass a couple hundred thousand dollars, or less.

“I tell these folks, ‘I know to you it’s a lot of money; it’s all you’ve got. I want to treat you with respect.’ We absolutely can take on folks who have millions, but if your money is significantly less, that’s fine by us too. People here are not paid on commission. They’re perfectly happy to sit down with a guy with $150,000 or a guy with $1.5 million.”

Committed, Not Commissioned

That policy of no commissions is uncommon in the industry, Matty said. “I don’t want to incentivize people here to do anything other than what’s in the best interest of the client. If they have cash in the bank, let them keep it in the bank. I’d rather spend time working with people, making a little bit off them every year, and keep them another 90 years, rather than get a big commission off them, then go out and find new clients next year. We have people here whose great-grandparents had accounts — people who have been here since the 1930s.”

St. Germain’s independence also allows advisors to give non-biased information, he said. “We’re not trying to sell any products to you. And at a lot of financial firms, people who work at the firm don’t have their money invested there. That’s not the case here.

“We live here, we work here, and we’re part of the community here, and we do our share to support the community that has supported us for the past 90 years,” he continued. “We try to give back at both the corporate level and personal level; virtually everyone here is volunteering or serving on boards, as well as all the financial support we give.”

Still, Matty said, what many clients appreciate most is simply being able to call and speak to someone with answers.

“I think we’re easy to talk to,” he said. “It’s a simple point, but it means an awful lot. Some people might prefer a website, but I find, especially as people get older, they want to call and talk to the same person, and not have to explain their circumstances every time. As clients get older, they really appreciate that.”

It’s an approach that has worked since D.J. St. Germain drove that Packard around Springfield — and will continue long after those who remember him are gone.

Joseph Bednar can be reached at [email protected]