Chapter and Verse

The 401(k) Coach Gets Write to It

Charlie Epstein says that, as he was pondering a title for his recently released book, he was, for a very short time by his estimation, thinking about something Steven Covey-like — “maybe ‘Nine Habits of Highly Successful Savers.’”

Charlie Epstein says that, as he was pondering a title for his recently released book, he was, for a very short time by his estimation, thinking about something Steven Covey-like — “maybe ‘Nine Habits of Highly Successful Savers.’”

But while those habits, or principles, as he calls them, are, indeed, the foundation of the book, and he has a patent pending on them, he opted instead for a phrase he started putting to use several years ago — ‘paychecks for life’ — because he believes it’s far more forceful, attention-grabbing, and to the point.

And it also helps him in his quest to entertain as well as educate, a quality he maintains is missing from most everything else that has been written on the subject.

“When I was starting in the retirement industry and reading through what was available for educational material … it was absolutely atrocious,” Epstein, president of Epstein Financial Services and the 401(k) Coach, told BusinessWest. “The average person comes into a 401(k) meeting with the expectation that they’ll be asleep in 10 minutes. You have to create a Disney-like experience for people today; you have to entertain them.

“That’s hard to do, but the principles are engaging — and they’re simple,” he went on, while explaining his approach taken with Paychecks for Life: How to Turn Your 401(k) into a Paycheck Manufacturing Company, a detailed look at effective retirement saving — although Epstein doesn’t use the word retirement any more.

Well, he does, but only in an exercise he’s probably repeated several hundred times, in which he asks the person he’s sitting across from (be it a reporter, client, or potential client) to give Webster’s definition of the term. Usually he doesn’t wait long before giving the answer himself — ‘to be put out of use’ — and then asking, “do you know anyone who’s working to be out of use?”

So he’s created the phrases ‘desirement,’ ‘desirement plan,’ ‘desirement mortgage,’ ‘desirement years,’ and others, which are at the heart of his motivation to pen and then self-publish Paychecks for Life.

“My book is not about how to invest your money better,” he explained. “It’s about the nine principles to get you to save smarter, and then how to maximize this mechanism that the government calls the 401(k).”

Elaborating, Epstein said he wrote the book ($22.99 hardcover, available through Amazon and paychecksforlife.com) to change people’s attitudes about saving for the years after they’re done working. When asked what needs to be changed, he said many things, but especially the still-wildly held opinion that Social Security or a company pension will be there and be an adequate source of income, and also the sentiment among many people that they simply cannot afford to save for retirement — or save enough to create what Epstein calls a paycheck-manufacturing company.

Elaborating, Epstein said he wrote the book ($22.99 hardcover, available through Amazon and paychecksforlife.com) to change people’s attitudes about saving for the years after they’re done working. When asked what needs to be changed, he said many things, but especially the still-wildly held opinion that Social Security or a company pension will be there and be an adequate source of income, and also the sentiment among many people that they simply cannot afford to save for retirement — or save enough to create what Epstein calls a paycheck-manufacturing company.

Which brings Epstein to one of those nine principles, the ‘desirement mortgage’ (which he calls the centerpiece of the book), and the many parallels he makes between this and a traditional mortgage.

Indeed, Epstein advises individuals to follow what he terms the “home-ownership formula for success” when they craft a retirement-savings strategy, with the following thought processes:

• You identified your dream house and what it would cost;

• You committed to paying for your dream house within a certain period of time;

• You calculated what it would cost, i.e. what you could afford to finance each month as a mortgage payment;

• You saved for your down payment;

• You adjusted your plan and budget to overcome unforeseen financial obstacles that might prevent you from achieving your dream of home ownership;

• You never stopped believing you could save for and finace your goal of home ownership; and

• You achieved your dream (desirement) and purchased your first home.

For this issue, BusinessWest turns some of the pages in Epstein’s book, in a figurative sense, while talking with the author to gain some perspective about how he came to write Paychecks for Life, and why he firmly believes it will successfully change some mindsets.

Past Is Prologue

“Your Annual Eviction Notices.”

That’s the title Epstein put on one of the earlier, introductory chapters of his book, and it’s a phrase designed to grab some attention, but also to drive home his points about Social Security and company pensions.

He notes that, when most people get their annual Social Security statements in the mail, they immediately turn to the page that breaks down what they’ll receiving in benefits if they retire at 62, 65, and 67, respectively. What just about everyone neglects to do, Epstein goes on, is look at the first page, where the following notice is printed:

“Social Security is a compact between generations. Since 1935, America has kept the promise of security for its workers and their families. Now, however, the Social Security system is facing serious financial problems, and action is needed soon to make sure the system will be sound when today’s younger workers are ready for retirement. In 2015, we will begin paying more in benefits than we collect in taxes. Without changes, by 2037 the Social Security Trust Fund will be able to pay only about 76 cents for each dollar of scheduled benefits.”

While discussing this fine print, as he called it, Epstein digressed to talk about why he and many others believe the Social Security system must be changed — with wealthy Americans removed from it, among other adjustments — but quickly returned to the matter at hand, which was getting readers to think well beyond checks issued by the U.S. Treasury when they consider their desirement years.

And the same goes for pension plans, he writes. “In 2007, of all the Fortune 500 pension plans that existed in 1996, 25% had been terminated, closed, or frozen. Between 1996 and 2007, Fortune 500 plans were closed or frozen at the average rate of 3% per year. In 2006, Verizon and IBM shocked the corporate world by freezing their pension plans (managers only in the case of Verizon), which created a standard that others soon followed.”

Which brings Epstein back to the 401(k) — the vehicle that enables employees to put a portion of their current income (a contribution) into several investments on a pre-tax basis — which has been the victim of some negative PR in recent years. Examples include the term ‘201(k),’ used often during the height of the Great Recession, when participants were seeing their balances take hits of 30% or more, and also a Time magazine cover which came out in October 2009 with the headline, “Why It’s Time to Retire the 401(k) (and What You Can Do Instead).”

“That was the worst journalism I think I’ve ever seen in my life,” he said of the Time article, adding that such bad press helped inspire Paychecks for Life. But the seed had actually been planted well before, when the idea of the 401(k) as a paycheck-manufacturing plant started gelling in his imagination.

But merely having such a plan isn’t enough to meet that mission of providing paychecks for life, Epstein told BusinessWest, noting that this simple fact is what compelled him to draft his nine principles for carrying out that task — and then writing about them. They are, in order:

• Act like an entrepreneur;

• Determine your desirement mortgage;

• Use other people’s money to capitalize your business;

• Harness the power of compound interest;

• Use technology to save automatically;

• Manage risk by outsourcing;

• Control fees and expenses;

• Guarantee your paychecks for life with annuities; and

• Take advantage of tax benefits with a Roth.

All the principles are important, said Epstein, noting that, together, they send a clear message — that, for a 401(k) to work as designed, the participant must take full ownership of it. His book, in essence, explains how to do that.

The Plot Thickens

It all starts, literally and figuratively, with that part about thinking like an entrepreneur, writes Epstein, who adds to the generally used definitions of that term his own spin: “one who figures out what products and services are needed and then finds the people (talent) who can make the idea become reality, all the while spending less money than will be received. In other words, one who recognizes opportunities and seizes them.”

It all starts, literally and figuratively, with that part about thinking like an entrepreneur, writes Epstein, who adds to the generally used definitions of that term his own spin: “one who figures out what products and services are needed and then finds the people (talent) who can make the idea become reality, all the while spending less money than will be received. In other words, one who recognizes opportunities and seizes them.”

Elaborating, Epstein notes that, when he asks many business owners to identify their retirement plan, they almost always answer, ‘you’re sitting in it.’ The bottom line is that entrepreneurs work hard to create value in their business so they can later transform it into paychecks for life. Employees need to do the same thing, he writes, through a 401(k).

“Your employer is saying, in essence, ‘I’m going to give you an opportunity to build a business inside my business that you can sell someday,’” he explained. “The government calls it the 401(k); I call it your own personal paycheck-manufacturing company, the single greatest mechanism you have to accumulate wealth in the most tax-advantaged way — but you have to act like an entrepreneur.”

There are similar calls to action, supporting charts and graphs, acronyms (such as YEM, your employer’s money; and USM, Uncle Sam’s money), and what Epstein calls ‘paychecks-for-life action steps’ for each of the principles. Consider these as typical:

• “The dollars you invest in your PCM Co. are like the employees your boss hires to work in his or her company, only better. Your employees work 24/7/365 and never complain. Hire as many as you can as fast as you can.”

• “To act like an entrepreneur, you must practice marginal thinking. Always think and act in small increments. The results will be exponential.”

• “Uncle Sam’s money (USM) is offered to you interest-free. You can either take it now and invest in your PCM Co. or let Uncle Sam keep it, never to be seen again.”

• “Think of your desirement mortgage the same way you do your home mortgage. Use the lowest interest rate possible and sleep at night. Treat it with respect. Never gamble with it.”

• “Slow and steady wins the race. Compounding takes a while to get started, but once it does, the process accelerates, and your savings grow more substantially every year.”

Epstein also uses a number of catchphrases and mantras he hopes will become part of the reader’s vocabulary, such as the ‘10-1-NOW’ rule.

The ‘10’ stands for 10% of the participant’s pay — the number Epstein and other experts say is needed to generate those paychecks for life. As for the ‘1,’ if you can’t save 10% now, increase the contribution by 1% of your earnings until you get to 10%.

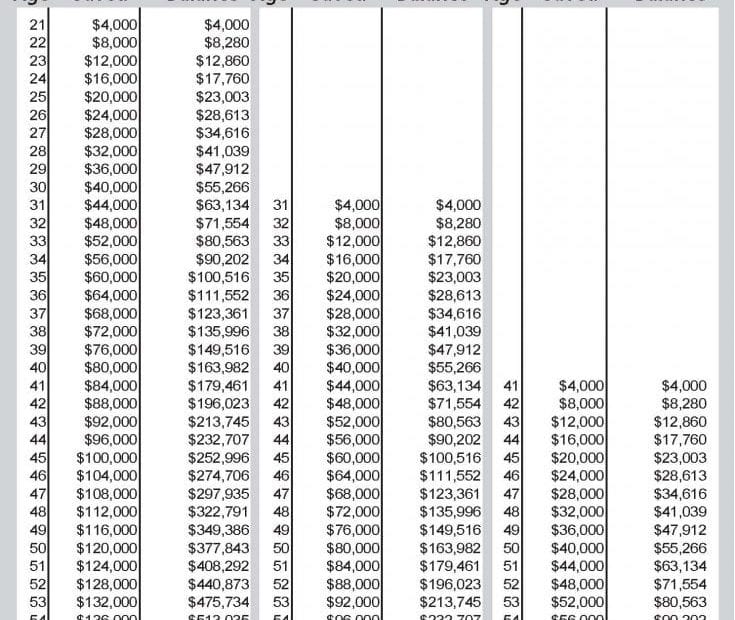

“If you can get a participant to increase their contribution by just 1% to 2% a year, the impact is hundreds of thousands of dollars,” he said, making use of the chart that appears on page 36 to drive home his point.

Overall, Epstein said he tried to make the book entertaining — and he believes he’s done that — “but you can’t get away from the numbers — although I made the numbers simple.”

As for his own numbers, Epstein said the initial printing of the book was for 5,000 copies, which are selling well thus far. There are two main audiences, he continued, listing the “advisor world” and individuals, with the former being the primary target at present.

More than 1,000 copies have been sold to date, with Legg Mason putting in an order for 500, he told BusinessWest, adding that Epstein Financial and the 401(k) Coach is in the process of packaging the nine principles so that advisers can effectively purchase material to teach them to clients and potential clients.

“There will be a video for each principle, and instructions on how to teach them,” he explained, “because advisors need to know how to teach these principles and educate and entertain people.”

As he talked about Paychecks for Life, Epstein — recently named one of the Top 100 Most Influential People by 401(k) Wire — repeatedly referred to it as his first book, with the clear implication that there would be more.

He gave no specifics on potential subject matter for future works, but hinted strongly that they will be similar in their intent to inform, educate, and help people enjoy a long, comfortable desirement.

And they will undoubtedly entertain as well, as Epstein strives to not only keep people awake through an intense discussion of effective 401(k) management, but firmly focused on his now-copyrighted and registered phrase ‘desirement planning.’

George O’Brien can be reached at [email protected]