Chicopee Savings Seeks to Soar on the Wings of Creativity

CSB President Bill Wagner

Like all financial institutions in the region, Chicopee Savings Bank is struggling to grow in a challenging environment marked by historically low interest rates, razor-thin margins, and unparalleled competition. Despite the hurdles, the institution has managed to grow market share, increase deposits, and, in general, position itself for when there is less turbulence.

Bill Wagner says that the last time Chicopee Savings Bank drew out a five-year plan was as it was making its conversion to a publicly traded institution in late 2006.

It was solid in most respects, he said, but it couldn’t possibly have taken into account the events that would trigger the so-called Great Recession less than two years later, not to mention a string of governmental actions to stem its impact. These steps have brought interest rates to historic lows, cut bank margins to razor-thin levels, and, ultimately, made it extremely difficult, if not impossible, for financial institutions to post the kind of solid growth that was commonplace in the decade preceding the crash.

It didn’t anticipate the housing bubble, which was aggravated significantly more than past housing bubbles by the failure of certain types of financial institutions that engaged in the secondary mortgage market, he explained. “There were two years of extremely high unemployment that weren’t in the plan, either, and we didn’t anticipate the unprecedented interference in the free-market cost of money by the Fed and the Treasury Department.

“We don’t do five-year plans anymore,” Wagner added with a wry smile. “That’s too far ahead to plan; we do three years now; every year we do a three-year plan.”

And even three years is a virtual eternity in the current environment, marked by challenging conditions, a lack of confidence among business owners, virtually non-existent organic growth in the business community, and spiraling competition in all areas, especially commercial lending.

In this climate, said Wagner, the dean of the local bank presidents now in his 27th year at the helm at CSB, the goals are to take advantage of the opportunities that do arise, work diligently to create new opportunities, and properly position the institution for the time when conditions improve. Meanwhile, the bank needs to remain true to its mission, be a positive force within the community, and, in a word, be creative.

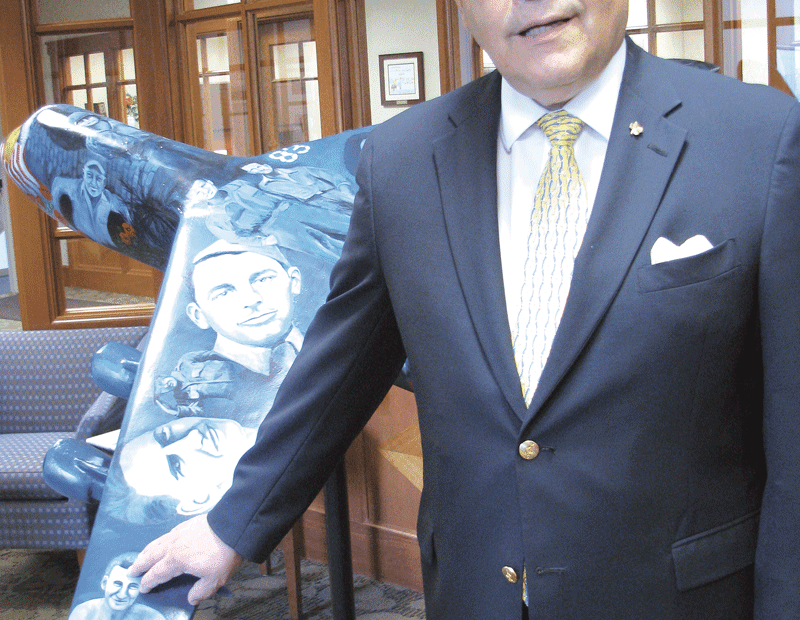

And CSB is doing all of that, he said, listing, as evidence, everything from positive gains in market share in commercial lending across the region to some new products and services, such as a rewards checking program, and even the fiberglass replica C-5 Galaxy transport plane now sitting in the bank’s headquarters on Center Street.

It is one of three planes sponsored by the Chicopee Savings Bank Foundation in a program to raise funds for a new senior center in the city. Like Springfield’s sneakers, West Springfield’s terriers, and Easthampton’s bears, the planes, with 7-foot wingspans, are themed artistically, and sponsored by area businesses and individuals. The plane in the lobby is called “In Your Honor,” and features the likenesses of Chicopee veterans who have fought in each of the nation’s wars.

“This is what it means to be part of the community,” Wagner said of the bank’s contributions to the program as he looked over the plane and pointed out veterans of various conflicts. “We’ve been here for nearly 170 years, and we’re going to keep on being here.”

And CSB will keep on slugging it out in a difficult environment where the choppy air is persistent and gaining altitude is a real challenge.

He’s Not Winging It

As he wrapped up his talk with BusinessWest, Wagner gave a quick tour of the Central Street facilities, focusing on the C-5 model and the many pieces of artwork hanging in his office, the hallways, and especially the ground-level conference room, which was the last stop.

There, among several framed pieces, are paintings by local artist Ted Fijal of Chicopee landmarks. There’s one of the main administration building at Elms College that dominates the back wall, and another looking down the hill on Springfield Street past the old Rivoli Theater and City Hall to the massive Cabotville Industrial Park, which has played such a big role in the city’s business history, dating back to the days when Civil War uniforms were manufactured there.

The artwork, along with the plane in the lobby, provide evidence of CSB’s devotion to the city that’s been its home since 1854, said Wagner, as does the fact that, while other institutions have removed geographic references from their names, this one hasn’t.

Nor has it struck the word ‘savings’ from the name either, years after most all other institutions thought it prudent to remove the adjective in a nod toward their institutions’ broader mission.

Rather than acknowledge change with new signage, CSB has done it with action, said Wagner, noting everything from the bank’s conversion to a public institution five years ago to its geographic expansion efforts (most recently in South Hadley and Ware; more on that later) to its ongoing evolution from a savings bank to an institution with a host of commercial and consumer products.

And that evolution continues, even in this current, ultra-challenging environment, said Wagner, adding that the bank continues to make solid gains in the realms of commercial lending and commercial real estate.

Indeed, as he looked over the latest statistics concerning commercial loan volume in individual communities, especially in the $100,000-to-$3 million range, or what he called the bank’s “sweet spot,” Wagner said CSB continues to grow market share.

“We’ve been pretty successful, in spite of the environment we’re in, in growing our commercial-loan department and maintaining asset quality,” he said, noting that, in many area cities and towns, the bank is at or near the top in volume of those sweet-spot-sized loans, and total volume of outstanding loans has gone from $51 million in 2008 to $75 million in 2010 and past $80 million this year. In the area of commercial real-estate loans, the numbers have risen from $150 million outstanding in 2008 to $178 million through the first half of this year.

It has been helped in these efforts, he continued, by continuing consolidation in the banking community (Berkshire Bank’s merger with Legacy is the latest example; see story on page 32) and movement away from such institutions and toward smaller community banks on the part of many business owners. But he also credits the bank’s team of experienced lenders that have enabled CSB to grow market share at a time when there has been marginal business growth across the region.

“It’s very difficult to grow as we have,” Wagner explained. “We have a solid, seasoned commercial lending team, we have a lot of technical skills, and we have the ability to service commercial accounts at a level business owners are comfortable with. We seldom lose a good commercial account, and we certainly gain a good deal more a year than we lose.”

And beyond sheer volume, the commercial portfolio boasts great diversity, he said, adding that this has been another asset during the recession and modest recovery. “It’s enabled us to go through this environment, knock on wood, without too many bruises and cuts; we’ve had higher-than-normal losses, but they’re still well within industry averages.”

Taking Flight

When asked what was in the bank’s latest three-year plan, Wagner said he wasn’t at liberty to reveal any specific details — in keeping with the rules governing the dissemination of information involving publicly traded institutions.

Speaking in general terms, though, he said there are no immediate plans for additional territorial expansion, and that one of the immediate goals is to grow the South Hadley and Ware branches, both opened in 2009, which are off to decent starts given the conditions.

Those branches represent the bank’s first foray in Hampshire County (although South Hadley borders Chicopee), and the Ware office represents its deepest move east. It was a common-sense move, said Wagner, adding that the location — near the Wal-Mart that serves the Greater Palmer area and not far from turnpike exit 8 — is ideal, and Ware, although headquarters to Country Bank, is not in the ‘overbanked’ category as so many area communities are.

“I went out to Ware one day to look at a piece of property and went by the Wal-Mart, and the place was packed,” he said while recounting how the journey to Ware started. “I drove through the shopping center and said to myself, ‘in this whole 10- or 12-town area, this has to be the busiest place.

“We thought that this would be the place to put a bank, and thus far, it’s worked out for us,” he continued. “It’s probably going to take a little longer than most branches, but it’s still progressing at an acceptable rate.”

While building up deposits in the new branches and gaining market share in commercial lending and deposits, the bank is taking other steps that would fall into the realm of building volume and effectively positioning itself for the day — whenever it comes (the Fed recently announced that it would keep its interest rate at nearly zero through the middle of 2013) — when interest rates start to rise and paper-thin margins start to increase.

“We’re going to continue to operate our franchise in the best interest of our stockholders and our customers,” he said. “And we’re going to continue to try the commercial sector as well as the retail sector, and try to be creative and differentiate ourselves from other banks.”

Rewards checking is one example of this creativity, Wagner said, adding that the product, rolled out several months ago, pays interest on accounts that maintain a certain level of activity in electronic banking services. It has helped the bank grow its retail portfolio in the same manner it has registered gains on the commercial side of the ledger.

“As a result of that and other efforts, we increased our demand deposits by $11 million over the past three months,” he explained. “This is part of our plan to continue to develop a high percentage of core deposits so that, when rates do go up, we have cheap money on our books.”

Meanwhile, the bank will continue its mission within the community, he said, adding that, beyond the planes purchased to help build the new senior center in Chicopee, the institution has been aggressive in its efforts to help victims of the recent tornadoes.

The bank has partnered with Salvation Army, the O’Connell Oil Co., and Channel 22 to assist in tornado-relief efforts. As of late July, more than $60,000 had been raised at CSB’s nine branches, and through parallel efforts involving the bank’s foundation and O’Connell’s convenience stores, the total has exceeded more than $120,000.

Soft Landing

Through nearly a half-century in banking (48 years to be exact, starting at the old Security National Bank in downtown Springfield), Wagner says he has been through six major bank crises by his count.

That includes the so-called ‘machine-shop recession’ of 1972, he said, recalling that, with severe cutbacks in defense spending as the Vietnam War was winding down, most of the machine shops in the area were hurt, and many didn’t survive. There was also the housing bubble of 1976, the deep recession of the early ’90s, which was particularly hard on banks, and others to follow. Comparing the current crisis to the one 20 years ago, he said the earlier one claimed more banks, obviously, “but this one has been very painful; it’s like comparing a broken arm to a broken leg — it all depends on whether you’re sitting or standing as to which one hurts more.”

Though they were all different in some respects, he went on, the common denominator with each crisis was the need for creativity and cautious aggressiveness to maneuver through the choppy air and be better positioned for when the skies cleared.

This time of challenge is no different, continued Wagner, who was exercising some plane speaking — literally and figuratively.

George O’Brien can be reached at [email protected]