A list of the region’s largest credit unions

Click here to download the PDF

Charlie Epstein

For the majority of people, saving in their 401(k) over the last few years may have felt like putting their chips down on red number 7 at the roulette table and praying for the ball to fall on that number.

If you had invested in the S&P 500 index for 10 years ending Dec. 31 2008, your average annualized return would have been -1.38% At that time, financial magazines were hyping the “new normal” and the “death of equities.” Fast-forward four years, and the 10-year return was +7.10%. Investing, in any asset class, is a long-term proposition. Just ask Warren Buffett.

So what’s the real message, for both 401(k) participants and their employers who create plans? That we need to begin to focus more on the most important part of the retirement equation. This is ascertaining the income placement for retirement, or what I like to call ‘paychecks for life.’ By receiving education through the advisory firm on their 401(k) plan, participants can use this benefit prudently and not haphazardly from trending financial propaganda.

Here are some steps that should be taken right now:

• Education sessions: Make sure your current advisor and 401(k) carrier provide regular education meetings that not just focus on investment performance, but teach your employees how to calculate exactly what they need to save every month, at a reasonable rate of return, to accumulate enough money at retirement to pay for all the things they desire to do. I call this ‘desirement’ planning.Why? Because Webster’s definition of retirement is to “put out of use.” I don’t know anyone working today who wants to be out out of use when they retire.

Working today should allow you to retire successfully and do all the things you desire to do tomorrow.

• Annual gap statement: Your current 401(k) record keeper can now provide each employee a gap report to show them, based on their current savings rate and a reasonable interest assumption, how much money they will have at retirement. Many of the providers will convert this lump-sum number into a monthly benefit — or paycheck for life. Your employees can see how much money they would actually have every month coming to them from their future 401(k) value. For many employees, this benefit is an eye-opening number and something they can easily relate to their current paycheck. It will indicate to them if they are on track or how far they are from replacing their present-day income.

• Plan level employee success: Ask your current record keeper if he or she can provide you with an overall plan-level participant report. This will allow you to analyze plan level demographics and how efficient your employees’ savings behaviors are. The data will allow you and your advisor to customize education meetings for employees who potentially have a major shortfall in obtaining a successful retirement. These outcomes are very effective in getting employees to increase their savings rate or adjust their investment allocations, and even with getting non-participants to start taking advantage of the benefit.

• Bold plan design: National 401(k) studies have proven that employers that implement automatic features encouraging their employees to save and progressively save more will improve the plan’s performance, resulting in healthier 401(k) balances for participants.

Here are the best automated features you should consider adding to your 401(k) plan:

— Automatic enrollment: All employees, once eligible, are automatically enrolled in the plan. They always have the option to opt out. The more successful plans automatically enroll their employees, not at the minimum 3% savings rate, but at the employer matching rate, which could be 6%. To be eligible to participate in the Exxon Mobil 401(k) plan, an employee must save a minimum of 10%. That’s bold plan design, but it works. The truth is, employees must be saving at least 10% of their pay to achieve a paycheck for life. For older employees, the rate may be higher.

— Automatic increase: One way to get employees to the magic 10% savings rate is to automatically increase their contributions by 1% per year. This is incremental success, and it works. If your employees are at 6% today, you will do them a great service by automatically increasing their contribution by 1% a year until they get to 10%. Again, employees always have the option to opt out of this feature.

These simple steps — customized education, income-gap statements for all your employees, along with two automatic plan-design features — will go a long way toward helping your employees view their 401(k) as a personal paycheck-manufacturing company. Leave the gambling to the casinos.

The Department of Labor greatly encourages you to use these automatic features, to such a degree that, if you follow the proper steps in communicating these automatic features to your employees, they will be granted fiduciary protection.

Charlie Epstein is the author of Paychecks for Life. His book teaches nine principles to help employees turn their 401(k) plans into paycheck-manufacturing companies; [email protected]. His book is available at www.paychecksforlife.org and at amazon.com.

Dan Eger

Congress is continually adjusting, changing, and, quite frankly, confusing us with continual depreciation-rule amendments. Lawmakers say this is all intended to stimulate the spending habits of companies. However, at the end of the day, it causes confusion to the business owners, internal accountants, public accountants, salesmen, and anyone else who tries to remember the actual deprecation rules from year to year.

To help you transition from prior rules to the current rules under the new American Taxpayer Relief Act of 2012, a comparative summary has been provided below. Understand that the new rules listed are as of the date of this publication and, as always, are subject to change.

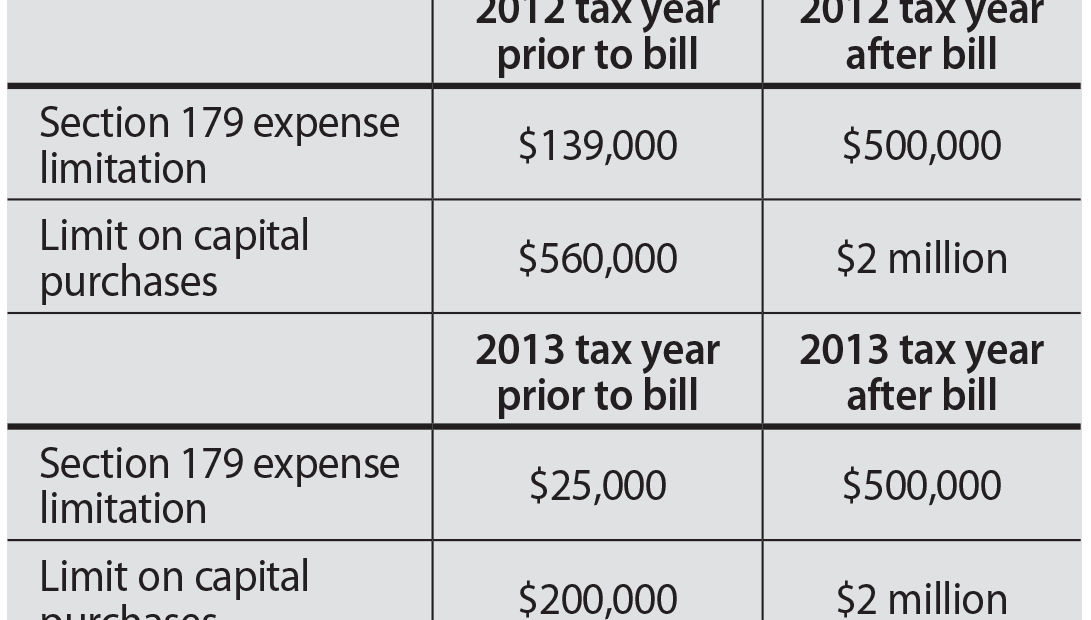

• Section 179. The deduction limit was increased with the Small Business Act of 2010 and extended thereafter with the addition of the American Taxpayer Relief Act of 2012. This deduction applied to both new and used capital equipment and ‘off-the-shelf’ software. You generally need taxable income in order to take this deduction, unlike bonus depreciation, which can be taken regardless of taxable income (i.e., you can generate a taxable loss with bonus deprecation).

Be aware that Section 179 limitation rules state that, for every dollar spent over the capital purchase limit, there is a dollar-for-dollar reduction in the deduction. That means, in 2012 and 2013, if you spend more than $2.5 million on qualified items, your Section 179 deductions have been completely phased out.

• Bonus depreciation. The 2012 American Taxpayer Relief Act has extended the 50% first-year depreciation under Code Sec. 168K. The qualified assets need to be acquired and placed into service before Jan. 1, 2014. It is available only on new equipment — meaning its first use by anyone (qualified leasehold rules are discussed later). In addition, there is no capital purchase limit on spending like in Section 179 rules. In 2012 you can deduct the first 50% of the asset cost as bonus depreciation; the remaining basis is then depreciated under normal rules. In 2011, the bonus depreciation was 100% of the asset cost, effectively allowing a full and immediate deduction.

One drawback is that most states do not recognize bonus depreciation, and you cannot take the additional expenditure. You may need to weigh this against the fact that, for state purposes, most states allow Section 179 deductions to the extent of the federal limit.

In 2011, qualified leasehold improvements, qualified restaurant property, and retail improvements were allowed to use a reduced depreciable life of 15 years. With the new 2012 relief bill, this is extended to anything placed into service after Jan. 1, 2012 and prior to Jan. 1, 2014; the extension allows for the 50% bonus depreciation and 15-year depreciable life.

• Auto and truck depreciation. Various rules dictate what you can deduct:

• Passenger autos: the maximum deduction 2012 is $11,060.

• Trucks and vans: the maximum deduction in 2012 is $11,160.

• Heavy SUVs used 100% for business: uses are eligible for 50% bonus. A SUV is considered heavy if it has a gross vehicle weight rating of more than 6,000 pounds but less than 14,000 pounds.

Additionally, a heavy SUV qualifies for Section 179 expensing of up to $25,000. (As a planning tool, you would be able to take bonus of 50% of the cost first, and then take the Section 179 of $25,000).

• Many vehicles, which by their nature are not likely to be used for personal purposes, qualify for a full Section 179 reduction in cost. They include the following:

— Heavy non-SUV vehicles with an open cargo area of at least six feet in interior length (like a full-size pickup truck);

— Vehicles that seat nine-plus behind the driver’s seat (like shuttle vans); and

— Vehicles with a fully enclosed driver’s compartment/cargo area, with no seating available behind the driver (basically a classic cargo van).

As stated previously, these favorable bonus depreciation provisions are scheduled to expire on Dec. 31, 2013. If you wish to take advantage of these provisions, you should plan to have the qualifying items acquired and placed in service by then. After that date (unless the laws are changed), there will be no more bonus depreciation. In addition, after 2013 the Section 179 deduction rules are scheduled to revert to the 2003 limit of $25,000 total deduction on $200,000 of qualified additions.

If you have any questions regarding depreciating assets, be sure to consult your tax advisor.

Dan Eger is a tax associate for the Holyoke-based public accounting firm Meyers Brothers Kalicka, P.C.; (413) 322-3555; [email protected]

Mary Meehan says women are becoming more prominent in many fields, from medicine to management to law, and her loan portfolio reflects that.

But he can’t. As the bank’s senior vice president and director of government-guaranteed lending, he more accurately characterizes his role as embracing already-existing trends, from the ever-increasing number of female business owners to the evolving priorities of the U.S. Small Business Administration.

The SBA — which guarantees loans by commercial banks and other lenders and provides capital to small businesses that are often unable to qualify for conventional credit — has, in fact, recognized Webster as Connecticut’s top lender to women-owned and minority-owned businesses.

“I would love to say it was my strategy to focus on minority- and women-owned businesses, but, honestly, it has been a policy of the SBA to really focus on four main areas: minorities, women, veterans, and rural businesses. We’ve done tremendously well with the first three,” Polito said, noting that Webster’s geographic footprint, in largely urban areas, doesn’t facilitate very much lending in rural markets.

“We have a lot of women, veterans, and minority businesses. And it’s something I really do want to focus on,” he continued. “One-third of my portfolio at Webster Bank is women owners — and that includes women only, not husband-and-wife teams. When I speak to my branch managers — who are mostly women — I’m really proud of that. I think it’s putting your money where your mouth is — not just saying it, but doing it.”

United Bank is doing it as well, having been named Massachusetts’ top lender to women-owned businesses for the past two years. Barbara-Jean Deloria, the bank’s senior vice president of commercial and retail lending credits two factors for that success.

“First, having commercial lenders who are women has been an influence on our ability to market to other women,” she told BusinessWest. “Obviously, in the past, the commercial-lending world has been dominated by male lenders, and by having more women in the marketplace attracts that business niche. Also, there are definitely more women-owned businesses that have surfaced in the past 10 years.”

Lenders both regional and national have noticed. In 1995, Wells Fargo made a commitment to lend $1 billion to women who owned businesses. Earlier this month, the financial-services giant said it would lend $55 billion to such companies by 2020.

Lisa Stevens, Wells Fargo’s lead executive for small business, issued a statement that “women-owned businesses are among America’s fastest growing segments, and we are honored to support their role in shaping the future of small business.” In fact, some 30% of U.S. businesses are owned by women — a number that continues to grow.

For this issue’s focus on banking and finance, BusinessWest sits down with several of the region’s commercial-lending players to talk about that trend, and what it means for lenders, borrowers, and the economy as a whole.

Growing Clout

Mary Meehan, first vice president of Commercial Loans at PeoplesBank, has experienced similar success lending to women.

“Roughly 40% of my portfolio is women business owners,” Meehan said, a number that includes manufacturing companies, commercial enterprises, and a range of other types of businesses. “We also have women who own investment and real-estate properties, and female doctors in medical offices; that whole area continues to grow as more women go to medical school. In fact, lending to women has also grown as more women get their MBAs or go to law school.”

Clearly, she said, this trend in commercial lending is being driven by larger economic and demographic shifts, from more women entrepreneurs to more daughters stepping into the CEO role in family enterprises, when sons used to dominate succession. “That’s a natural progression in terms of family-run businesses in general.”

The role of women in the region’s business landscape is even more impressive, Meehan said, considering that the 40% figure she cited doesn’t include nonprofits — which form a considerable niche in Western Mass. and at PeoplesBank; many such organizations are run by women.

The increasing profile of women’s business, in fact, is one reason why the SBA and other agencies have chosen to recognize entities that lend to women, said Dena Hall, senior vice president of Marketing and Community Relations at United Bank. “That they’ve designated an award for lending to women is significant.”

Richard Collins, United Bank’s president and CEO, welcomes the opportunity. “We are always eager to help women in business achieve their goals,” he said. “Their success is always significant to the growth of the economy, and their contributions are more vital than ever in today’s economic environment.”

Statistics from the federal government’s National Women’s Business Council (NWBC) back up that perception with hard numbers. Women-owned firms make up 28.7% of all non-farm businesses across the country and generate $1.2 trillion in total receipts. A full 88.3% of these firms are non-employer firms, while the remaining 11.7% have paid employees, employing a total of 7.6 million people.

In addition, women-owned businesses make up 52% of all businesses in health care and social assistance while other top industries for women include educational services (46% are women-owned), waste management and remediation services (37%), retail trade (34%), and arts, entertainment, and recreation (30%).

However, bank and government lending remains a largely untapped resource, according to the NWBC, as 56% of women-owned businesses used personal or family savings to start or acquire their business, compared to fewer than 1% who used a business loan from the federal, state, or local government or a government-guaranteed business loan from a bank.

However, for those who pursue SBA and other types of loans, Deloria said women are more educated than ever about the resources available to them. “I think women-owned businesses are very proactive on doing the research; even before they come in to see me, they recognize that the SBA is a really good resource for them. Most of the time, they’ve already researched that aspect of it.”

Polito agreed, and added that women tend to carefully consider the perspective the prospective lender brings to the table. “I don’t want to generalize, but it has been my experience, when I do meet with women-owned businesses, I find they’re more willing [than men] to listen to recommendations and guidance about what I’ve seen with other businesses of a similar size or a similar business model. They’re more willing to listen and take guidance from the bank.”

Forging Ties

That sort of openness and teamwork lends itself to a successful loan, Meehan said, especially when it comes to solo or small businesses. “We have a focus especially on the small-business side, a focus on our branches and lending to someone who comes into the branch. The manager is focused on developing that small-business relationship.

“We go through the same due diligence process, male or female, of getting to know the customer’s business and everything that entails.”

And there’s no shortage of resources available to educate borrowers on what the process entails. Deloria said she’s been active with the Women’s Chamber and other business-networking groups and found them to be effective ways to meet business owners and share information.

“We’re trying to offer more education, identify women’s organizations in the communities we serve to do more outreach,” Polito added. “Frankly, its intimidating for pretty much everyone, and often very intimidating for women- and minority-owned businesses, to walk into a bank and apply for a loan. But I don’t want people to feel that way.”

He said loan officers at Webster “put their noses to the grindstone” for every application that comes in, rather than turning down a potentially promising loan after a cursory look at a credit score. “Two people have to decline a loan. What we’ve instituted for many years is a second-look process. When a deal is declined, we have a second reviewer look at it to make sure we can’t do it.

“Even an SBA guarantee can never make a good loan out of a bad loan,” he added. “But if we can get the loan over the hump for approval, we’ll do it; we’ll take that chance.”

That’s because a successful loan benefits everyone: the bank, the borrower, and, in theory, the customers and employees of the company — which is increasingly likely to be run by a woman.

“The business works or it doesn’t — male or female, and no matter what the color of their skin is,” Polito concluded. “So, the more outreach we can do, the better. Everyone wins when you get capital into the market.”

Joseph Bednar can be reached at [email protected]

Paul Scully says Country Bank’s community involvement extends beyond philanthropy to financial-education programs for young and old.

Specifically, Kolb — the bank’s senior vice president and chief commercial banking officer, who came on board six months ago — said he wants to take a “barbell approach” to growing its loan portfolio. Picture Country’s reach geographically, he said, with Springfield and Worcester representing the weights and all the smaller towns in between, where Country has a branch presence, as the bar.

“If we want to continue to grow the portfolio, we have to put our toe in the waters of other areas,” Kolb said, noting that the bank does not have physical branches in those two larger cities, but sees opportunities there. “We’re looking to do more in the Worcester market and the Springfield market … we want to expand our presence in those markets.”

As a mutual savings bank with $1.4 billion in assets, and boasting 14 branches and 245 employees — Country has the reach to grow, said its president, Paul Scully, but continues to maintain an emphasis on small communities.

“We’re still focused on providing a full range of consumer and business products and services within our marketplace, and we view our marketplace as the geography between the Worcester and Springfield areas,” he noted. “Our branching strategy is the same: smaller towns.”

However, he noted, “branch locations don’t matter as much anymore; between mobile banking, remote capture, and other services, customers have really caught on to the fact that they can do all their banking and really never go into a branch. Technology has allowed us to expand our product offerings within more urban marketplaces without having a physical presence there.”

And growth is what Scully has in mind.

“Last year we originated about $105 million in commercial loans — pretty respectable, considering what the market was and what the competition is,” he said, noting that the bank boasts a loan portfolio of $838 million. “A lot of banks are looking for the same opportunities as we are, but there aren’t as many opportunities to go around. What every bank tries to do is differentiate themselves from the crowd.”

One of the ways Country has always tried to do so is through an emphasis on service.

“We look at ourselves as a small business,” Scully said. “We’re a good-sized bank, but we’re still a small business able to offer personalized service. We don’t have a high level of turnover; people who come into the branches see the same people who have been working with them for a long time. Customers are recognized and feel comfortable with the people they’re doing business with. They’re not calling an 800 number where someone across the country is answering. The service element is really a key factor in our success and has set us apart since 1850.”

Added Kolb, “on the commercial side, as an organization, we provide a nice match for what the market demands. We’re not too big and not too small.” But he also echoed Scully’s sentiments about service.

“The money’s still green at the bank across the street. It’s a pretty homogenous product. We all make mortgages and commercial loans; we all do deposits,” he said. “But what really differentiates us is service. It’s not just a tagline; it’s something that’s ingrained and apparent.

“When you walk around the teller line, the average tenure there is 20 years. In the business lines, it’s 10 to 15 years. They don’t stay here because it’s a local, sleepy bank in Massachusetts; they take a lot of pride in the relationships they’ve forged. It is the difference between us and the bank across the street.”

Wiring of the Green

Bob Kolb says Internet and mobile banking are key to a bank’s success today, but so is the personal service available at a branch.

“There are still customers out there that like to see the branch bank on the corner,” he explained. “Having that visibility is important, and it’s never going away; it’s the doorstep to us being active in the community. And giving back to the community is really part of the culture at Country Bank.”

But technology has certainly changed the way customers interact with banks, Scully told BusinessWest.

“We’re pretty much able to have a full range of products to meet everyone’s expectations, from savings accounts straight through to mobile banking and e-bill payment,” he said. “Last year, we converted our ATMs to digital ATMs, so there are no more envelopes; you put the check right into it. That’s the convenience factor; it expedites the transaction for a person sitting in their car with a couple kids or a dog who wants to be somewhere else.”

Those high-tech advances extend to remote capture for businesses that can conduct transactions without going to a branch, and retail online banking has come into its own as well, but there’s no longer as dramatic a split in the ages of people who use it.

“We used to think of it as a generational thing, with the older client base wanting to come into the branch,” Scully said. “People still want to know the branch is on the corner, but we’ve learned that age doesn’t matter. Almost everyone uses a computer, and we have a lot more seniors using e-billing and other technology, and we have people feeling more and more comfortable with security.”

For that reason, the bank’s educational outreach spans generations as well. Country conducts a banking program in area elementary schools, building early financial literacy by teaching students about savings and investment and providing them with passbooks to open their own in-school accounts. It has since expanded that to a ‘credit for life’ program for high-school seniors, teaching them about credit scores and smart handling of paychecks and expenses.

“But the other thing we’re focused on is the senior piece,” Scully noted. “We do a lot with senior centers, talking about banking technology and security, so they don’t feel intimidated using a computer for their banking.”

When Social Security switched over to electronic payments, “we did a lot with senior centers about what that change means and why e-banking is very secure,” he added. “Once seniors feel more comfortable with the technology and understand that their money is not at risk, they want to use e-banking; they want to use mobile banking.”

“The key,” added Kolb, “is to make those channels available, whether through the computer, at a branch, or on the phone, whether someone is 18 or 88 years old.”

In fact, Scully said, there’s no reason why remote banking shouldn’t be embraced by seniors. “Once people realize, ‘OK, I don’t have to go out in the snow and possibly fall down,’ suddenly they feel really good about it.”

For younger customers, he added, “it’s all about smartphones. They’re not looking to have a passbook; they don’t want to bring in some clunky old thing.”

Hometown Appeals

The Country Bank name is only 32 years old, but the institution has been around since 1850, when it was known as Ware Savings Bank. It took on its current name after a 1981 merger with Palmer Savings Bank; another merger with Leicester Savings Bank 17 years ago further increased the bank’s holdings.

From the time of the name change, Scully said, it has been important to communicate a sense of community ties. That’s why the name of each branch reflects its hometown: Country Bank of Ludlow, Country Bank of Palmer, etc. “We like to think of ourselves as that town’s small-town bank, their community bank,” he said — despite the occasional confusion of a customer who goes into a branch in a different town and wonders whether he can bank there because of the different name.

The small-town focus is a positive when it comes to lending, Kolb said.

“Small business is really the backbone of America, and it’s certainly the backbone of the small areas we operate in,” he told BusinessWest. “In Central and Western Mass., it’s about small business; it’s about Main Street. With our branch network and experienced lenders on the commercial side and on the mortgage-origination side, that puts us in a great spot to serve the community with the resources of a big bank, yet we’re small enough to be able to jump in the car and see someone at 7 at night, or be reminded when walking down the aisle of the grocery store that you need to see somebody.”

The hometown emphasis is also at the heart of Country’s philanthropic efforts. In 2012, Scully noted, the bank donated more than $600,000 to community organizations.

“They’re causes that people don’t think about because they don’t necessarily apply to their life, but there are so many people whose lives are affected,” he said, citing the bank’s support of domestic-violence task forces, food pantries, and other organizations. “Unless you need that service, you might not pay attention to the fact that their funding sources have been reduced, or that their needs have grown.”

But the bank offers more than money, he was quick to add, noting that management staff alone volunteered more than 1,400 hours last year at community events — “that’s personal time, nights and weekends” — and the bank has been expanding volunteer opportunities for all employees as well. “Now we have more than 100 volunteers giving back to the community.”

All the bank’s efforts — from its lending business to its charitable work — boil down to an effort to improve people’s quality of life,” Scully said. “Maybe we lend to a business that puts up a building and hires more people. Or we could be giving a scholarship to a kid who then graduates from college. Or we could be supporting social services. It’s all full circle, quality of life.”

Kolb was quick to note that “philanthropy is not something that drives revenue; it’s not a profit center. What it is, really, is part of the culture; it’s consistent with the mutuality of the company. What we’re trying to do for the communities we serve is not a revenue driver; it’s really part of who we are.”

Specifically, Scully added, “the profit is in the long-term impact in the community. Everyone benefits from it. And we didn’t start those things; it’s the legacy of the bank as it relates to every aspect of community life.”

Bottom Line

In many ways, despite its asset growth, some things have remained the same at Country Bank, Scully said. “Community banking is consistent banking. We’re taking what we believe we’ve done well and expanding it.”

And that requires constant reconsideration of business strategies. For example, “the [loan] portfolio is very heavy in real estate, so one of my objectives in coming here is to diversify the portfolio,” Kolb said, a process that will take some time considering an economy that is improving, but still far from thriving. “The idea is to start with small businesses and identify opportunities in that space where we can exploit our leverage with our infrastructure and the experience of our lenders and our service.”

Scully called today’s banking environment “an exciting time, but a challenging one,” but he noted that, particularly since the financial collapse in 2008 that was brought on partly by the misdeeds of the largest banks, there’s something appealing to many customers about a community bank’s consistency.

“That’s not to disparage super-regionals, but those organizations use their customer base as a means to produce revenue and income, which increase shareholder value,” Kolb noted. “What sets us apart, as a mutual bank, is that our depositors are in essence the drivers, and our mission is to service those individuals.”

“We have sort of a split personality,” Scully added. “Are we a big little bank or a little big bank? We’re sort of both; we can do almost any type of transaction a big bank can do, and by any standard we’re considered large, but by having a focus on the customer, the community perceives it as a little bank.”

But one that, barbells or not, is growing stronger.

Joseph Bednar can be reached at [email protected]

Jennifer Reynolds

In fact, in today’s business environment, very few companies do business in only one state. Further, it is not unusual to find that small to medium-sized closely held companies are doing business in several states — or even all 50. And it’s no secret that states are struggling financially. As such, they are all competing for your tax dollars.

A review of your company’s interstate activities can help comply with the various tax laws and identify valuable tax-saving opportunities.

So, how do you know if your business should be filing in other states?

A state’s power to tax your business depends on its connection (or nexus, as it is referred to in the world of accountants and attorneys) with the state. The level of nexus required, however, may vary depending on the tax involved. The four most prevalent state taxes are:

• Sales and use taxes;

• Corporate income taxes;

• Franchise taxes; and

• Payroll taxes.

Many early nexus cases involved sales and use taxes. Technically, the consumer is responsible for those taxes, but because of the impracticality of collecting them from individuals, states have placed this burden on the seller.

Do you have an economic presence?

Going back to the founding fathers, the Commerce Clause prohibited states from imposing tax on out-of-state businesses unless that business had a ‘substantial nexus’ with the taxing state. Substantial nexus, as you can imagine, can be interpreted differently by each person. So how do we know what constitutes substantial nexus?

Well, as with all interpretations of the Constitution, the courts interpret the meaning. Here, U.S. Supreme Court decisions have determined that, for purposes of applying the commerce clause, ‘substantial nexus’ means physical presence. Thus, states cannot constitutionally tax an out-of-state business unless that business has some form of physical presence in that state.

In its landmark 1992 decision in Quill v. North Dakota, the U.S. Supreme Court ruled that a state cannot require an out-of-state seller to collect sales or use taxes unless it has a substantial physical presence in the state. Again, the meaning of ‘physical presence’ depends on the facts and circumstances. But, in general, you have a physical presence if you maintain offices, stores, manufacturing or distribution facilities, property, or employees in the state.

In the age of e-commerce, it’s extremely easy for companies to do business remotely with customers in states or countries where they have no physical presence. Many courts and state legislatures believe that economic presence is a more relevant indicator of a business’s connection with a state.

Over the last few years, there has been a trend in the courts toward eliminating the physical-presence requirement, at least for purposes of income and franchise taxes. But for now, physical presence is still required today to trigger sales and use tax-collection obligations, but many states require only a very minimal presence to establish nexus, and the courts are agreeing.

However, under Federal Public Law 86-272, states are prohibited from taxing a company’s income if its only activity in that state consists of the solicitation of orders or the sale of tangible personal property that is approved and shipped from outside of that state.

One caveat, though: this law does not apply to intangible property. Hence, several recent cases have allowed states to tax an out-of-state firm’s income on intangibles such as credit cards or trademark licenses, even though the firm had no physical presence in that state. A substantial ‘economic’ presence was sufficient.

For example, Connecticut has now instituted a ‘bright-line’ economic nexus test. A taxpayer is deemed to have substantial economic presence if it generates receipts of $500,000 or more attributable to the purposeful direction of business activities toward the state, examined in light of the frequency, quantity, and systematic nature of a company’s economic contacts with this state, without regard to physical presence, to the extent permitted by the U.S. Constitution.

However, Public Law 86-272 will continue to restrict Connecticut’s ability to impose a tax on income derived within its borders from interstate commerce if that activity was only the solicitation of orders of tangible personal property, and where those orders are sent from outside of Connecticut for acceptance and subsequently shipped from outside of Connecticut. And Connecticut is not alone. More states are pushing for economic presence in lieu of a required physical presence.

Am I doubling my tax obligations by crossing state lines?

You might think that establishing nexus with a state increases your tax exposure, but in some cases it does the opposite.

Consider corporate income taxes. Many states determine the portion of your income subject to their tax using a three-factor formula based on the percentage of your sales, property, and payroll attributable to the state. (In some states, the sales factor is double-weighted.) Others use a single-factor formula based on sales. If you’re able to apportion some of your income to a state with a lower tax rate, it can actually reduce your company’s tax bill.

Taking the ‘I’ll take my chances and let them find me’ approach can be a gamble.

Revenue-hungry states will continue to extend the geographical reach of their tax laws, and state agencies will continue to communicate with each other about state taxes. Along with companies, state revenue departments are also becoming more sophisticated.

For example, many states are starting to query vendor files of customers within the state. In-state auditors are looking at invoices to ensure that proper sales and use taxes are being paid for the out-of-state businesses with potential nexus in their state. From there, the states are generating nexus questionnaires to businesses that appear in their audits but are not showing as being registered in their state.

States are not only going after current taxes, but targeting businesses and individuals for back taxes from the date they first started doing business in that state. In addition to the tax, states are imposing penalties for not registering to do business in the state (which itself requires a fee and generally requires the company to file annual reports). The penalties for not registering, and penalties and interest for late filing and payment of taxes, can be substantial.

How can I be proactive to determine my company’s exposure to other states?

To ensure compliance with all applicable laws, be sure to periodically review your business’s interstate activities either internally with your accounting staff or with a qualified tax or legal advisor.

A nexus study may help you to understand your company’s obligations in the various states. It helps to identify your company’s normal business activities in relation to the various nexus standards, based on the type of tax (i.e. income, franchise, payroll, sales and use, or even a ‘privilege tax’ imposed by some states) and the states with which you may have connections.

Having the information up front before you begin a job or do business in another state can help you manage your company’s bottom line. Managing and planning for potential filing and tax obligations in advance can mean the difference between a profitable job and an unprofitable job.

This article is intended to provide a general overview of the multi-state tax environment. As always, you should consult your tax and/or legal advisor regarding the applicability of this general information to your business’s specific situations.

Jennifer Reynolds is a tax manager with the Holyoke-based certified public accounting firm Meyers Brothers Kalicka, P.C.; (413) 322-3542; [email protected]

Sheryl McQuade calls Berkshire Bank’s blend of financial clout and personal service “thinking big and acting small.”

The Wall Street development is the bank’s recent move from NASDAQ to the New York Stock Exchange, which became official in November, around the same time that eight former Connecticut Bank and Trust (CBT) branches — which Berkshire acquired earlier in 2012 — officially converted to their new name, Berkshire Bank — CBT Region.

“Connecticut is a new market for us. We made an investment in Connecticut by way of our acquisition of CBT, and we did so because the Connecticut market offers significant opportunities for commercial and retail banking,” said Sheryl McQuade, senior vice president and regional commercial leader for the Greater Hartford market.

“We believe Berkshire Bank has a unique value proposition,” said McQuade, who admitted that any expansion into Connecticut is fraught with challenge, because the region is arguably as overbanked as Western Mass. “It’s not like we’re the first game in town there, but we believe, because of our size — which is about $5.5 billion now — matched with our product capabilities and diverse business lines, we can offer everything a large, regional bank can, but so do in a more nimble fashion.”

The Connecticut acquisition ostensibly benefits former CBT customers due to the banks’ comparative size; CBT had assets of about $280 million, and commercial loan limits of around $3 million, while Berkshire Bank can conduct deals in the $15 million range. McQuade also touted the bank’s growing suite of products in retail and business banking, insurance, and wealth management.

None of which, she said, will matter if Berkshire Bank doesn’t effectively integrate itself into the culture of its new communities, and that takes more than size. It’s a strategy that McQuade calls “thinking big and acting small,” and for this month’s focus on banking and finance, she and other bank leaders explained to BusinessWest exactly what that entails.

Growing Footprint

Berkshire Bank is no stranger to growth, having taken an aggressive approach to geographic expansion in recent years.

In the summer of 2011, the bank acquired Legacy Bancorp of Pittsfield, bringing 15 branches under its umbrella in Western Mass. and New York. That move came on the heels of other, smaller acquisitions, including New York-based Rome Bancorp earlier in 2011 — a series of moves that, including the CBT merger, has seen Berkshire expand its footprint from 43 to 75 branches in less than 20 months.

Last year, Sean Gray, executive vice president of Retail Banking, told BusinessWest that Berkshire Bank looks to organic growth first — as he put it, “getting the most out of our existing footprint.”

But the past decade has seen this Pittsfield-based institution make headway in New York, Vermont, Central Mass., and now Connecticut. Gray said Berkshire looks for banks that share a similar culture when seeking consolidation opportunities, but the leaders of its Springfield and Hartford markets say they’ve launched an ambitious strategy to introduce a unique, customer-focused culture in new branches.

For example, “we’re launching a new program called MyBanker,” said Lori Gazzillo, assistant vice president of Community Relations. “When we talk about relationship banking, we’re talking about personal bankers who work with individuals who have various financial needs, whether it’s loans or insurance or deposits. They can go to this one person for all their banking needs — somebody they can call about anything, who can connect them with the services they need.”

Branch design is also being overhauled to reflect a more personal, less institutional touch, McQuade said. The bank’s Springfield headquarters, where she and Chamberlain sat down with BusinessWest, is a good example, with its coffee station at the entrance, and where customers are invited to sit down with tellers, no longer separated by an impersonal counter.

“This will be the design going forward in our new branches,” Gazzillo said, adding that older branches will be renovated to match. “This new design enhances teller technology, and it’s a more personalized situation; it’s also more efficient as transactions go, and it’s more inviting, with a café and comfortable chairs and a common room.”

That common room is another way Berkshire is trying to connect with its communities. Each branch will offer local nonprofits and other organizations a space, equipped with multi-media, wi-fi, and videoconferencing equipment, to hold meetings. “It’s a way to offer something back to the communities we’re operating in,” McQuade said, “versus a lot of banks pushing people away from bricks and mortar and toward online banking.”

That’s a constant concern for banks these days, which are trying to serve two distinct constituencies — the traditional, older-skewing customer who prefers face-to-face transactions, and the younger, more mobile crowd that has embraced banking on computers, smartphones, and tablets.

“Berkshire Bank has really invested in a lot of products and technological capabilities,” McQuade said. “On the commercial side, we’re not dependent on branches to serve our customers; we have remote deposit and other tools that a large, regional bank would have.”

However, Gazzillo said, “we think it needs to be both. People are becoming more high-tech, relying on their phones and iPads, and we’re working on rolling out a mobile-banking platform. But customers still want to see someone on a personal level. It’s important to keep up with both, and we’re large enough to do that.”

Sue Chamberlain says it’s important to cater effectively to both the high-tech, mobile crowd and those who want face-to-face interaction.

Culture Change

Gazzillo knows that Berkshire — which dubs itself “America’s most exciting bank” in its marketing materials — has bitten off quite a bit with its recent acquisitions, but she feels the institution has the right strategy to thrive in a highly competitive financial-services landscape.

“We’re succeeding at a time, and in a banking environment, where it’s difficult for banks to succeed,” she said. “We have been expanding, and we’ve acquired a number of banks, but it’s a careful process of looking at the culture and philosophy of a bank and making sure it fits within our own banking culture.

“We’re doing it the right way,” she said, “by providing customers with the tools and resources they need, and a level of personal service that they want. I’m proud of that, and happy with what we’re doing.”

Reflecting that emphasis, Berkshire Bank delayed the changeover of CBT branches by about six months because the company was going through a major upgrade to its operating system across all branches, and didn’t want to put the new, Connecticut-based customers through two separate conversions.

Meanwhile, Berkshire is trying to ease the transition for Nutmeg Staters in other ways. “Part of that is by hiring capable, talented people who are seasoned and experienced in their own communities,” McQuade said. “I’ve hired several people in Connecticut who have a history and relationships in their markets.”

The bank remains committed, Gazzillo said, to meeting community needs as well, across its entire four-state footprint.

“We have a foundation, and as far as financial contributions go, we give $1.5 million,” she said, but added that money is just one element of community involvement; others include a volunteer culture and a benefit that offers employees paid time off to volunteer at nonprofits in their communities. “That’s a big component of who we are, of being a community partner.”

McQuade credited bank President and CEO Michael Daly, who recently added chairman of the board to his business card, for setting the institution — which originally focused mostly on commercial banking — on a path to strong growth across many niches.

“He had the vision to grow the bank’s commercial business, but in a relationship-banking fashion, principally because, in addition to all our capabilities in commercial banking, we have wealth management, an insurance group — a lot of things that can be leveraged as part of a deliberate, relationship-banking strategy,” she explained — one that attempts to draw in young customers and meet their needs for life.

And, now, aims to bring a little excitement to Connecticut, too.

Joseph Bednar can be reached at [email protected]

Charlie Epstein

• Create or review the investment policy statement (IPS). If your 401(k) plan was audited by the U.S. Department of Labor (DOL), which is a greater possibility now that the DOL has hired an additional 300 auditors, one of the first documents they will ask for is your plan’s IPS. The ideal IPS gives clear guidelines, creates a reasonable process, provides a roadmap for making sound, long-term-oriented investment decisions, and even outlines criteria for keeping the investment committee, or a solo-business-owner plan sponsor, on track.

• Benchmark plan fees and services. You should review your plan fees and services on an annual basis and, at least every three to five years, perform a full RFP (request for proposal) and benchmark your plan’s fees and services to determine the ‘reasonableness’ of the fees you are paying and the level and quality of the services you receive from all your service providers.

The onus is on you, the plan fiduciary, to benchmark the fee and service data you now possess. This can be a detailed and lengthy process, requiring considerable expertise. This is where the services of an advisor with the knowledge and expertise of the retirement-plan industry can be an invaluable asset.

• Perform investment due diligence. You should review your plan’s investment options and benchmark the performance and fees on a regular basis — either quarterly, semiannually, or annually — to insure your participants are receiving ‘best in class.’

• Assess the plan’s investment menu. In the current, dynamic investment environment, you should perform investment-structure evaluation as part of your regular due-diligence process. Some things to consider:

— Is your money market the most appropriate ‘cash’ account for your plan? Most are paying 0% after expenses today.

— Should you streamline the investment-fund lineup? Less is more. As a rule of thumb, 16 to 18 fund choices should be enough.

— Are diversification funds, such as real estate, natural resources, emerging markets, and inflation-protected bond funds appropriate options to add?

— Should you add low-cost index or ETF fund options to mitigate costs?

— If your qualified deferred investment account is a money-market or guaranteed account, you should consider changing to a target date, lifestyle, or age-based managed account for greater fiduciary protection.

• Examine your plan’s target-date fund. After the passage of the Pension Protection Act in 2006, plan sponsors rushed to add target-date funds as their qualified default investment alternative (QDIA), and many settled on their record keeper’s target-date fund. At least 50 to 60 new target-date fund options have been launched since 2006.

What seemed like a good fit six years ago might not be so today. You should consider re-evaluating your target-date fund for a number of reasons: performance, fees, and glide path — is your QDIA a glide-to or glide-through retirement glide path, and which do you deem appropriate for your employees? Actively managed target-date funds and funds with tactical and asset-protection strategies have entered the market. You should evaluate your target-date fund’s appropriateness at least once a year.

• Revisit auto features. I wrote an article titled “Bold and Scold” some time back. In it, I encouraged you and your plan advisor to consider adding auto features to increase the chances of your employees achieving greater success at retirement. You should add all auto features that the Pension Protection Act offers, not only because you are protected as a plan fiduciary, but because these feature automatic enrollment, automatic increase of employee contribution by at least 1% a year, and auto-default into your plan’s target-date fund; all have been proven to increase an employee’s chances of retiring with more money in their plan and thus more income at retirement.

• Increase employee education and communication. Your employees need help and encouragement to save an ever-increasing amount throughout their working years. Your 401(k) plan is the single greatest mechanism they have to achieve a successful retirement with what I call a ‘paycheck for life.’ In addition, the two largest assets your employees will own in their lifetime are their home and their 401(k) account balances.

They treat their home with respect. By this I mean they would never go to Foxwoods or Mohegan Sun and bet their home on ‘red 7.’ Yet, every day, they treat the 401(k) like a casino, because the average employee does not have the time, tenacity, or expertise to pick investments. They need help, and they need it on an ongoing basis. At a minimum, you should have your plan’s advisor available twice a year to provide group education and meet once a year, one-on-one, with all employees to assist them in making more informed and more appropriate saving and investment decisions designed specifically for their personal financial situation.

• Document, document, document. The DOL has essentially stated in numerous retirement-plan litigation cases that, if it wasn’t documented, it never happened. Make sure you document everything you do related to your company’s 401(k) plan. Record all investment due-diligence meetings and fee-benchmarking and RFP analysis. Record all education meetings and plan communications. Keep a plan file with all plan documents and reports. Be prepared for a DOL audit in advance.

I hope you will unwrap all eight of these plan recommendations and put them into action in 2013 and beyond. You will sleep easier, and your employees will be more successful in creating paychecks for life.

Charles D. Epstein is the author of Paychecks for Life: How to Turn Your 401(k) into a Paycheck Manufacturing Company. As the 401(k) Coach, he has been nominated one of the top 100 most influential individuals in the 401(k) industry by 401kWire; (413) 478-8580; www.paychecksforlife.org

Jeff Sattler says NUVO is on target with its goals for assets, revenue, and gaining respectability in the local banking market.

That’s because he’s been in their shoes.

Indeed, five years ago, he was one of the principals trying to lure investors and amass the capital needed to launch the venture that would become NUVO Bank, which he now serves as president.

“When you’re dealing with a banker, most of them haven’t owned a business — they have to critique the business owner,” he told BusinessWest. “I started this thing with the same mentality as other entrepreneurs — ‘I’m going to do this; there’s a market, and I’m going to make this work.’ And I had the same growth pains, issues, challenges, and fears that any entrepreneur has. I can talk the same language as that business owner.”

This linguistic ability is one of the factors that Sattler and NUVO’s CEO, Dale Janes, believe have contributed to the bank’s steady growth and recent momentum. Like most of its commercial clients, NUVO’s primary objective has been to gain a strong measure of respectability and build a solid foundation for growth, said Janes, adding that, despite being launched just as the worst downturn since the Great Recession was taking hold, the bank has, in his opinion, achieved that goal.

While other banks rush to add branches, Dale Janes says NUVO will stay with its business model and maintain one location.

Sattler agreed. “We’re profitable right on plan,” he said. “I don’t want to be the biggest in this market; I want to be the most profitable, and that’s return on assets, return on equity, efficiency ratios … key bank ratios that we want to be leaders in eventually, and we’re getting there now.”

Janes told BusinessWest that the institution’s first four-plus years in business have proven that its basic model — operating through one location with a reliance on technology that would ensure that most clients would rarely see that facility on the ground floor of Tower Square — works, and there is no need to change it.

“Our overhead is so low, we can afford to be aggressive on retail CD rates, savings rates, and the costs of accounts,” he said while citing the main advantages to being small and efficient. “The core of our model is small business, small business, small business — and it’s worked; about a year ago, it really started to kick in.

“With longevity comes credibility,” he continued. “So, more and more now, customers who used to do business with Jeff or with me are saying, ‘these guys are around, and they’re going to be here; let’s go check them out.”

Doing some quick math, Sattler noted that NUVO, which just passed the $100 million mark in assets, has something approaching 1% of the regional market, and is by far the smallest bank in the region. While that number may not sound impressive, he said — while noting that doubling or tripling it would still give the bank only 2% or 3% of a market dominated by huge national and regional players — it is a solid base on which to build.

And as he surveyed the local banking market, especially the smaller, community institutions, Janes, who has been in the business for more than 30 years, sees ample opportunity to grow.

“There is going to be more consolidation within this market; it’s inevitable,” he said with a large dose of certainty in his voice. “And with that consolidation, there will be opportunities for banks with the right products and the right approach to customer service. We’ve positioned ourselves to be one of those banks.”

For this issue and its focus on banking and financial services, BusinessWest looks at how far NUVO has managed to come in four challenging years, and what the future could hold for the institution.

By All Accounts

As he prepared to talk with BusinessWest, Sattler was closing on another small-business loan, giving NUVO just over 80 such clients in its portfolio.

That’s another comparatively small number, especially when put alongside the other institutions with downtown Springfield mailing addresses, but Janes and Sattler both take a ‘glass is much more than half-full’ mentality.

“Every new customer is another dot on the map,” said Sattler, adding that the bank’s approach from the day it opened has been to achieve to measured, smart growth, while also carving out a specific niche in the market — in this case, what would be considered small, or even very small, loans.

And both officers believe the institution has achieved those missions, while also establishing the NUVO brand across Greater Springfield and into Northern Connecticut.

“This is the reason why we knew we were going to be successful — we have a niche,” said Sattler, referring to the small-business loans like the one he closed on that afternoon late last month. “Everyone thought we were going to fail, but we succeeded, because we created that niche.”

Both men said that virtually every bank in the region can write the kinds of small loans that NUVO has made its specialty, but most don’t have the need or desire to do so, and can’t do it as well.

“We’ll look at every single deal, no matter what the industry,” he explained. “I won’t say ‘yes’ to every deal, but if we can’t do it, then nobody can do it.”

Meanwhile, another advantage is the aforementioned ability to “speak the language,” as Sattler described it.

“I appreciate their passion,” he said of entrepreneurs. “They have a vision of where they want to take their company, and I can relate to that. I try to get under the tent with them and say, ‘how are we going to make this loan?’

“They say, ‘Sattler, I’m not talking to you like a banker,’” he continued. “And I’m not; I’m a business owner, not just a banker, who started the same way most of these businesses started.”

Overall, the bank has been “on target” with everything from asset growth to profitability to brand recognition, said Janes, adding that the current momentum has manifested itself in a number of ways.

For starters, there have been roughly 18 months of continued monthly profits, he said, adding that another commercial-lending officer, the bank’s third, was recently hired, and another addition is planned for the first quarter of next year. Meanwhile, the bank is planning another capital raise — the prospectus is currently being finalized — to provide the wherewithal to continue growing.

“We’re doing well against our original plan, and super well against our model,” Janes explained. “We have a lot of focus and a lot of discipline around the business model; we can’t be everything to everyone, and we’re honest about that.”

Balance Statement

Moving forward, Janes and Sattler said NUVO is in the process of scripting a new three-year strategic plan.

When asked what it will likely include, they said, in essence, there would be more of the same that has marked the bank’s four-plus years of existence — with the emphasis on more.

The planned additions to the commercial lending staff — “we’re now building a lending team,” said Sattler — and the capital raise are part of this strategic initiative, noted Janes. Overall, he believes that, given the bank’s steady growth and the current landscape in financial services, NUVO is well-positioned to add market share for the short and long term.

Elaborating, he said there are two trends in the marketplace that are working in NUVO’s favor. The first is a significant shift among consumers, business owners, and investors away from large regional and national banks and toward community banks.

“And why not? They’re just smaller, and they have more flexibility and more options for the small-business customer,” he told BusinessWest. “And we plan to take advantage of that, especially on the investor side, because as we grow, we’re going to need to raise more capital.”

The second trend, although it has slowed in recent years, is a movement toward greater consolidation, said Janes, adding that the many publicly owned regional and community banks serving Western Mass. are both candidates for additional expansion themselves or targets for acquisition. And both scenarios, which will be driven by shareholders and their desire for better returns, bode well for banks like NUVO that can take on customers left wary by such transactions.

“This is a very challenging time to provide a return to your shareholders,” he said of the situation facing the public banks. “Everyone’s had what amounts to a free pass because of the recession, because everyone made bad loans and business slowed down, but that free pass is going to get called in, and banks are going to have to start producing, either a dividend or growth in the market price of the stock.

“People are going to instigate,” he continued, “and get these banks to either perform better on an earnings-per-share basis through the organic nature of their business, or by selling.”

And while NUVO has plans for more lending officers, employees, loans, and assets, one thing there won’t be more of is branches.

“People keep asking me, ‘why don’t you open a branch here?’” said Janes, adding that there have been many suggestions when it comes to ‘here.’

“That’s not who we are or ever intend to be,” he continued. “We will never have a huge branch network, and probably will not have a traditional branch. We will expand our footprint; we will take our model and replicate it somewhere else, in a market where there are a lot of small businesses. That was our intent, and it’s still our intent. We’re not ready for it yet, but our three-year plan contemplates something like that.

“Right now, we just want to dominate where we are,” Janes went on, “and earn our keep in this region.”

Despite its lone location, NUVO has been able to grow its presence and build its brand through track record and word-of-mouth referrals. And with presence and referrals, the bank has opportunities to show what it can do, said Janes, which is an important component in the growth equation.

“Once we get in front of people,” he said, “we’re pretty good at bringing in some business.”

Brand Equity

Looking at the numbers compiled by area banks for assets, deposits, and loans (see pages 38 and 39), Janes and Sattler know they will be looking up at the rest of the region’s banking community for quite some time.

But after four recession-riddled years, the bank is starting to see some real momentum. As Janes said, there is enough statistical and anecdotal evidence to show that the bank is indeed a proven commodity — and that things are truly looking up.

George O’Brien can be reached at [email protected]

Gary G. Breton

But wait. There may be some additional factors that you may not have considered.

First, ask yourself, what is the primary reason that you have made your decision? If it is a matter of you not being comfortable with your current account officer or what you feel are not competitive financing terms on your credit facilities, it might be better to have a frank discussion with the head of your commercial lender’s loan department in the first instance and with your account officer in the second instance. Many times, both of these concerns can be addressed in house in a timely fashion, and you could avoid the time and cost of taking your business elsewhere.

However, if you have taken these matters into account, and the basis for your decision involves other factors that you feel are not capable of being addressed by your current lender, understand that there are a number of potential benefits and costs associated with making such a move.

On the potential benefit side of the ledger, your new lender may be in a position to provide you with a new account officer who may be more in tune with your current and anticipated business needs. This officer should be someone with whom you are comfortable and share an open and honest mutual respect. He or she must have the ability to understand (as well as the desire to care about) your business to allow your company to be successful, and the lines of communication must be strong between the two of you.

Additionally, you may find that your new lender possesses the ability to respond to your financing needs in a timelier manner and with the requirement of less paperwork to support your request than your current lender. Another consideration is being sure that your prospective lender possesses the necessary financing products that may be specific to your business needs, such as letter-of-credit availability or asset-based financing.

You might also be pleasantly surprised by some of the terms of the financing commitment that is ultimately made by your new lender, which can include a more competitive interest rate as well as more palatable collateral and financial-covenant requirements than those that are currently in place with your existing financing. One key factor to keep in mind is that many of the terms and conditions of a financing commitment may be negotiable, including the size of any required loan-commitment fee.

While some of the possible benefits of such a move are highlighted above, there are also considerations that need to be given to the possible costs and disadvantages that may be associated with making such a transition. There is, of course, the amount of time you and your professional advisors will need to devote to produce the required paperwork to accompany your application for new financing, which will traditionally include your company’s history, prospective budget and business plan, current financial statements, and recent tax returns.

Additionally, if such financing will involve the pledging of real-estate collateral, the new lender will require a current appraisal to ascertain the fair market value of such property, as well as an environmental site assessment to determine the absence of any hazardous materials that might impact the value of such real estate prior to completing their financing. Also, if any asset-based financing will be part of your financing package, the new lender may also require a field audit/appraisal of your company’s raw material, work in process, and finished inventory. The costs of completing any such required reports generally are the responsibility of your company and can quickly add up to what may be considered a prohibitive figure.

Another major cost that may discourage your contemplated move is whether or not your current financing terms include a prepayment penalty that will be imposed if you elect to refinance with another lender. In many instances, these prepayment penalty formulas, when applied, can, in and of themselves, give a business owner pause on whether the contemplated move will be worth paying what may translate into a substantial sum of money. While many times, such prepayment penalties have been the primary factor in deciding to remain with one’s current lender, there are a number of instances where the cumulative weight of all the components considered by the business owner have outweighed the cost of incurring such a penalty.

So, you can see that the decision as to whether or not it may be in your company’s best interest to move to a new lender requires both a thoughtful and extensive evaluation of many important issues, including those identified above, so that the ultimate decision is grounded on a solid factual footing.

Gary G. Breton, Esq. is a partner with Bacon Wilson, P.C. and a member of its banking and finance department. His major emphasis of practice includes representation of financial-lending institutions, as well as both individual and business borrowers. He also represents numerous business clients in startup and ongoing business operations as well as the purchase and sale of businesses; (413) 781-0560; [email protected]

Charlotte Cathro

With a few changes to how data is accumulated and processed, this can be accomplished.

Managers need to frequently monitor the financial statements of a business. Management oversight is an important component of internal control to ensure that processes are running smoothly. Typically this includes a review of the actual results of the period in comparison to the previous period or an established budget. Reviewing this comparison highlights unexpected activity and may indicate errors or fraud. It may also alter the outlook for future periods, and budgets are most effective when they are flexible and adjust for business changes.

In these economic times, companies need to be able to react quickly to indications of a poor outlook. The business may have bank restrictions for its debt, and will want to monitor the status of these ratios to prevent noncompliance. Cutting costs and scaling back budgets might be necessary to stay afloat. On the other hand, if business results are better than expected, management can use this information to increase investment or expansion. When the review of the financial performance is done well after the period ends, management has less time to make such decisions.

Up-to-date cash-flow information indicates what money is available for use in operations and what excess can be invested or distributed to the owners. Some investment opportunities, such as acquisitions of brands or other companies, may present themselves suddenly and require a quick turnaround. Available cash may also allow the company to pay invoices before they are due in order to take advantage of vendor discounts. However, many companies don’t reconcile their cash to the bank until month’s end, and may not even be entering transactions on a daily basis.

Automation can speed up the financial-reporting process. Transactions that are recurring in the same amount, such as rent, depreciation, and amortization, can be entered in advance. Reversing entries can be set up within the system to reverse the following month. Many organizations are moving from batch-processed systems, which update the financial software on a periodic basis from subsidiary ledgers such as accounts payable and inventory, to real-time systems. These real-time systems process transactions to all related modules immediately. Without the need to post batches and check that they were properly transferred, month-end closing is therefore expedited. Ideally, with these systems, reports can be run daily showing the current financial standing of the business.

Use of the Internet allows for much more up-to-date information. Electronic fund transfers are fixed to be paid on a specific date, unlike checks, which are delayed by receipt and time to clear. Online billing and bank statements allow businesses to keep track of transactions long before they receive statements in the mail. Bank accounts can be reconciled on a daily or weekly basis. Expenses can be entered as soon as the desired period of activity is complete. Businesses should sign up to view activity online for banks and vendors that provide this service.

Some information might not be available within the time frame. For example, bills for less-organized vendors can be received well after the expense was incurred. In order to make sure that the financial statements are as reliable as possible, estimates should be recorded for income and expenses expected to apply to the period. Estimates are acceptable as long as they are reasonably developed and would not change the outcome of any decision-making. A review of the records from the last few periods can be undertaken to indicate what items might be currently missing. Once the documents actually come in, the estimates can be reversed and the actual amounts recorded.

Timely financial information does come with a cost. The reliability of the data should not be sacrificed for speed. In some cases, investment in more advanced accounting software may be required, as well as additional staff or overtime hours for existing employees. However, the increased time in the interim could offset the time required at month-end and year-end close. Both the financial cost and additional stress of providing more timely financial information should be determined and weighed against the benefit it provides.

Charlotte Cathro is a tax manager with the Holyoke-based CPA firm Meyers Brothers Kalicka, P.C.; (413) 536-8510; [email protected]

One of the great scams being perpetrated today is what’s known as tax-return identity theft. Unscrupulous thieves are using stolen identities to prepare tax returns on behalf of unsuspecting individuals, and reaping thousands of dollars per false return filed.

How big of a problem is it? Treasury Inspector General Russell George said back in May that criminals who file fraudulent tax returns by stealing people’s identities could rake in an estimated $26 billion over the next five years because the IRS cannot keep up with the volume of the fraud. That’s a sobering figure.

How do you know if you have been subject to tax-return identity theft? Basically, after you file your actual tax return, you will get a letter from the IRS that says something like, “thank you for filing your tax return. However, we already received your tax return back in February.” That should trigger a big alert that something is seriously wrong. Residents of Puerto Rico have it even worse, since they don’t need to file a U.S. tax return unless they have U.S. activity. As such, when their identities are stolen for tax-return purposes, they don’t even get a warning letter, because they may not have had to file a U.S. tax return. Thus they don’t even know their identities were stolen in the first place. As a result, Puerto Rico has become a priority for the IRS.

The identity thieves basically make up everything on the tax return and prepare the return in such a way that a huge refund is expected. The refund is sent electronically, and the thieves now have loaded-up debit cards. The average theft appears to be in area of $5,000, and the aggregate problem is in the billions of dollars.

It is absolutely imperative that people be more diligent with respect to whom they provide their private and financial information. Further, it is more important than ever for businesses to be extra diligent in the safeguarding of that information. Massachusetts General Law CMR 17 mandates that organizations maintaining private information do so with strict accordance to the law. Therefore, ask how your lawyer, accountant, tax preparer, medical center, new or used car dealer, mortgage lender, bank, etc., safeguards your personal information.

I don’t believe it is unreasonable to predict that random, educational ‘spot testing’ by taxing authorities, in the form of actual physical visits, is in the future to help alleviate the hemorrhaging of personal information. As such, the best advice I can offer to everyone is to prepare to be able to explain to clients, customers, and the IRS, for that matter, exactly how you safeguard private information.

Here’s an example. Our office is on the top floor of our building, and there is no elevator access after working hours or weekends and holidays without an access key. Besides the small fortune we invested in electronic security, our office is equipped with motion alarms and continuously recording cameras. We have a camera in our file room. With the permission of our building owner, we even have cameras outside of our leased office space. That’s how serious we have become with security.

Although this whole issue is due to unscrupulous individuals, I believe both the IRS and the Commonwealth of Massachusetts bear some responsibility here. The rush to mandate e-filing for everyone obviously happened faster than the IRS and the Commonwealth’s ability to monitor it, as we can see from the epidemic of tax-return identity theft. At least with paper returns, W-2s were attached, and the returns were signed by taxpayers and preparers. Presently, none of these safeguards are required by thieves, and the proverbial rooster is in the electronic hen house.

Tax returns can be filed electronically from anywhere; interestingly, one of the great tax-return identity-theft operations originated out of the Dominican Republic. The only reason this operation was discovered was because several New York City postal employees were contracted by the thieves to deliver tax refunds to certain P.O. boxes. The only ones captured were the postal employees, because the organizers of the fraud were never caught.

Even the IRS inadvertently discloses personal information. I am personally aware of a very recent situation where an IRS letter was inadvertently sent to the wrong address. As a safeguard, the IRS letter indicated only the last four digits of the taxpayer’s Social Security number. The recipient wanted to do the right thing and wrote a letter to the IRS with a copy of the original letter, in the hopes that the IRS would understand that they had the wrong address. The IRS responded with a “thank you, we’ll get back to you” and, as an added bonus, provided the entire Social Security number of the taxpayer to this complete stranger. Now that is a very serious breach of security. We have notified the IRS Commissioner in Washington of this particular situation, and we hope we are able to help prevent an unfortunate security breach from occurring again.