A chart of area accounting firms

Click HERE to download the PDF chart

By KRISTINA DRZAL HOUGHTON, CPA, MST

Kristina Drzal-Houghton

Since D.C. lawmakers are unlikely to pass, extend, or modify tax provisions anytime soon, tax planning may seem pointless. But, actually, careful planning is wise regardless of the situation and even more important during uncertain times.

Even though the federal tax laws haven’t changed much from last year, your circumstances may have changed. And some rules that expired on Dec. 31, 2013 may yet be restored, even retroactively, to Jan. 1, 2014. It could be the perfect time for you to get a fresh perspective.

To make sure you’re taking all the appropriate steps to minimize your individual and business taxes, you should anticipate possible changes with the informed guidance of your tax professional.

Tax Strategies for Individuals

Before you can make wise planning decisions about your individual taxes, you need to be aware of your current tax situation.

Can you control when you receive income, or at least determine when deductible expenses are paid? If you can control timing, you have a valuable planning tool that can enable you to reduce your taxable income and tax liability.

Maximize your tax strategies by forecasting income-tax positions for 2014 and, to the extent possible, subsequent years. Evaluate not only the amount of your income but also the types of income you anticipate generating, your marginal tax bracket, net investment income, wages and self-employment earnings, and capital gains and losses.

Before deciding to accelerate or defer income and prepay or delay deductible expenses, you need to gauge the possible effect of the alternative minimum tax (AMT) on these tax-planning strategies. Having a number of miscellaneous itemized deductions, personal exemptions, medical expenses, and state and local taxes can trigger AMT.

The opportunity to take advantage of income timing exists particularly for taxpayers who are:

• In a different tax bracket in 2014 than in 2015;

• Subject to the AMT in one year but not the other;

• Subject to the 3.8% net investment income (NII) tax in one year but not the other; or

• Subject to the additional 0.9% Medicare tax on earned income in one year but not the other.

The 3.8% NII tax and the 0.9% Medicare tax apply when your modified adjusted gross income exceeds threshold amounts. Net investment income includes dividends, rents, interest, passive activity income, capital gains, annuities, and royalties. Passive pass-through income is subject to the NII tax.

The NII tax does not apply to non-passive income, such as:

• Self-employment income;

• Income from an active trade or business;

• Portions of the gain on the sale of an active interest in a partnership or S corporation with investment assets; and

• IRA or qualified plan distributions.

Remember that the additional 0.9% Medicare payroll tax applies to earnings of self-employed individuals and wages in excess of the thresholds in the table above.

After analyzing your specific tax situation, if you anticipate that your income will be higher in 2015, you might benefit from accelerating income into 2014 and possibly postponing deductions, keeping the AMT threat in mind.

On the other hand, if you think you may be in a lower tax bracket in 2015, look for ways to defer some of your 2014 income. For example, you could delay into 2015:

• Collecting rents;

• Receiving payments for services;

• Accepting a year-end bonus; and

• Collecting business debts.

Also, if you itemize deductions, consider prepaying some of your 2015 tax-deductible expenses in 2014. The following expenses are commonly prepaid as part of year-end tax planning:

• Charitable contributions. You may take a tax deduction for cash contributions to qualified charities of up to 50% of adjusted gross income (AGI). When contemplating charitable contributions, consider contributing appreciated securities that you have held for more than one year. Usually, you will receive a charitable deduction for the full value of the securities, while avoiding the capital-gains tax that would be incurred upon sale of the securities.

• State and local income taxes. You may prepay any state and local income taxes normally due on Jan. 15, 2015 if you do not expect to be subject to the AMT in 2014.

• Real-estate taxes. You can prepay in 2014 any real-estate tax due early in 2015. But you should keep in mind how the AMT could affect both years when preparing to pay real-estate taxes on your residence or other personal real estate. However, real-estate tax on rental property is deductible and can be safely prepaid even if you are subject to the AMT.

• Mortgage interest. Your ability to deduct prepaid interest has limits. But, to the extent your January mortgage payment reflects interest accrued as of Dec. 31, 2014, a payment before year end will secure the interest deduction in 2014.

• Miscellaneous itemized deductions. These include unreimbursed employee business expenses, tax-return preparation fees, investment expenses, and certain other miscellaneous itemized deductions that together are in excess of 2% of AGI.

The amount of itemized deductions you can claim on your 2014 tax return is reduced by 3% of the amount by which your AGI exceeds the thresholds, which began as low as $152,000. However, deductions for medical expenses, investment interest, casualty and theft losses, and gambling losses are not subject to the limitation. Taxpayers cannot lose more than 80% of the itemized deductions subject to the phaseout.

Know Your Tax Rates, Exemptions, and Phaseouts

A personal exemption is usually available for you, your spouse if you are married and file a joint return, and each dependent (a qualifying child or qualifying relative who meets certain tests). The personal exemption for 2014 is $3,950.

But the total personal exemptions to which you are entitled will be phased out, or reduced, by 2% of the amount that your AGI exceeds the threshold for your filing status. The threshold amounts for the personal-exemption phaseout are the same as for itemized deductions.

Even when federal income-tax rates are the same for you in both years, accelerating deductible expenses into 2014 and/or deferring income into 2015 or later years can provide a longer period to benefit from money that you will eventually pay in taxes.

Beware the Alternative Minimum Tax Trap

As mentioned previously, determining whether you are subject to the alternative minimum tax in any given year figures prominently in tax planning.

Every year the IRS ties, or indexes, to inflation the AMT exemption and related thresholds based on filing status. If it’s apparent that you will be subject to the AMT in 2014, you should consider deferring certain tax payments that are not deductible for AMT purposes until 2015. For example, you may defer your 2014 state and local income taxes and real-estate taxes, except taxes on rental property, which are not subject to the AMT. Also consider deferring into 2015 your miscellaneous itemized deductions, such as investment expenses and employee business expenses.

However, if the AMT will not apply to your taxes in 2014, but could apply in 2015, you may want to prepay some of these expenses to lock in a 2015 tax benefit. Just be careful that your prepayment does not make you subject to AMT in 2014.

If you do not expect to be subject to the AMT in either year, the age-old strategy of deduction ‘bunching’ could apply. If this is expected to be a high year for miscellaneous itemized deductions, consider accelerating next year’s expenses into this year.

Or, if this is a low year for these deductions, try to defer these expenses for the rest of the year into next year. This method helps you maximize the likelihood that these deductions will result in a tax benefit.

Exploit Long-term Capital Gains

While avoiding or deferring tax may be your primary goal, to the extent there is income to report, the income of choice is long-term capital gain thanks to the favorable tax rate available. Short-term capital gain is taxed at your ordinary income tax rate.

If you hold a capital asset for more than one year before selling it, your capital gain is long-term. For most taxpayers, long-term capital gain is taxed at rates no higher than 15%. But taxpayers in the 10% to 15% ordinary income-tax bracket have a long-term capital-gain tax rate of 0%.

Taxpayers whose income exceeds the thresholds set for the relatively new 39.6% ordinary tax rate are subject to a 20% rate on capital gain.

If the long-term capital-gain rates of 0%, 15%, or 20% are not complicated enough, keep in mind that special rates of 25% can apply to certain real estate, and 28% to certain collectibles. Also, gains on the sale of certain C corporations held for more than five years can qualify for a 0% rate. Talk to your tax adviser before you assume the long-term capital gains rate that would apply.

Remember that you can use capital losses, including worthless securities and bad debts, to offset capital gains. If you lose more than you gain during the year, you can offset ordinary income by up to $3,000 of your losses. Then you can carry forward any excess losses into the next tax year.

However, you should be careful not to violate the ‘wash sale’ rule by buying an asset nearly identical to the one you sold at a loss within 30 days before or after the sale. Otherwise, the wash-sale rule will prevent you from claiming the loss immediately. While wash-sale losses are deferred, wash-sale gains are fully taxable. It’s important to discuss the meaning of nearly, or ‘substantially,’ identical assets with your tax adviser.

Contribute to a Retirement Plan

You may be able to reduce your taxes by contributing to a retirement plan. If your employer sponsors a retirement plan, such as a 401(k), 403(b), or SIMPLE plan, your contributions avoid current taxation, as will any investment earnings until you begin receiving distributions from the plan. Some plans allow you to make after-tax Roth contributions, which will not reduce your current income, but you will generally have no tax to pay when those amounts, plus any associated earnings, are withdrawn in future years.

You and your spouse must have earned income to contribute to either a traditional or Roth IRA. Only taxpayers with modified AGI below certain thresholds are permitted to contribute to a Roth IRA. If a workplace retirement plan covers you or your spouse, modified AGI also controls your ability to deduct your contribution to a traditional IRA.

If you would like to contribute to a Roth IRA, but your income exceeds the threshold, consider contributing to a traditional IRA for 2014, and convert the IRA to a Roth IRA in 2015. Be sure to inquire about the tax consequences of the conversion, especially if you have funds in other traditional IRAs.

In addition to the SIMPLE IRA, self-employed individuals can have a simplified employee pension (SEP) plan. They may contribute as much as 25% of their net earnings from self-employment, not including contributions to themselves. The contribution limit is $52,000 in 2014. The self-employed may set up a SEP plan as late as the due date, including extensions, of their 2014 income tax return.

An individual, or solo, 401(k) is another option for the self-employed. For 2014, a self-employed individual, as an employee, may defer up to $17,500 ($23,000 for age 50 or older) of annual compensation. Acting as the employer, the individual may contribute 25% of net profits, excluding the deferred $17,500, up to a maximum contribution of $52,000.

Withholding and Estimated Tax Payments

If you expect to be subject to an underpayment penalty for failure to pay your 2014 tax liability on a timely basis, consider increasing your withholding between now and the end of the year to reduce or eliminate the penalty. Increasing your final estimated tax deposit due Jan. 15, 2015 may reduce the amount of the penalty but is unlikely to eliminate it entirely.

Withholding, even if done on the last day of the tax year, is deemed withheld ratably throughout the tax year. Underpayment penalties can be avoided when total withholdings and estimated tax payments exceed the 2013 tax liability or, in the case of higher-income taxpayers, 110% of 2013 tax.

Tax Strategies for Business Owners

The main tax issue to keep in mind if you’re a business owner is that a number of tax provisions, such as 50% bonus depreciation, expired at the end of 2013. In addition, the Section 179 deduction has been limited significantly.

Congress may pass legislation to renew or modify these tax breaks — perhaps retroactively. Of course, you can’t count on that possibility, so if you have used these provisions to reduce your taxes in the past, it might be advisable to adjust your withholding and estimated tax payments for 2014.

Special 50% Bonus Depreciation

Through 2013, businesses could use the special bonus depreciation to deduct up to 50% of the cost of such assets as new equipment, computer software, and other qualifying property placed into service by year end. The 50% bonus depreciation did not apply to used equipment. Unless Congress acts, it will not be available at all in 2014.

Section 179 Deduction

Under Section 179 of the IRS Tax Code, businesses could expense the full cost of new and used equipment, including technology, in the year of purchase instead of over a number of years. They still can. However, the amount they can expense has dropped from an upper limit of $500,000 in 2013 to $25,000 in 2014 — a sizable difference. If your company has nearly reached the $25,000 expensing limit, you may want to postpone further purchases until 2015.

The 2014 limit on equipment purchases qualifying for Section 179 treatment is $200,000. After a business reaches the maximum amount, the available tax deduction phases out on a dollar-for-dollar basis. In other words, once a business buys $225,000 of equipment, the deduction is reduced to zero. You should monitor your company’s total purchases to prevent the phaseout.

Repair Regulations

The IRS and the U.S. Treasury have issued final tangible property regulations (TPRs) that become mandatory for tax year 2014. These TPRs will likely require most businesses to file additional tax returns and supporting statements and/or include in their returns certain annual elections. Those new, additional returns are referred to as IRS Form 3115, Change in Accounting Method.

If you have multiple trades or businesses, more than one building, or leasehold improvements, whether or not these are contained in separate legal entities, such as LLCs, or disregarded entities, we may have to prepare numerous, separate Form 3115s, as well as make numerous TPR annual elections. Since the changes required by the TPR are so widespread, starting on the various analysis prior to year end is highly suggested.

While the preparation of the IRS form 3115 will be done, in the majority of cases, by this 2014 tax-return filing, certain new annual elections related to the TPRs are anticipated to be required and/or chosen for every income-tax filing subsequent to your adoption of the new TPRs.

You should discuss with your tax adviser the TPR elections choices. While they will certainly advise you on the alternatives or choices that are available for you regarding these TPR annual method elections, please remember the final choices are yours to make. The three common annual method TPR elections are the following:

• The de minimis safe harbor for writeoff of property acquisitions and non-incidental material and supplies costing less than your book writeoff policy, such as items costing less than a certain dollar amount (for example, less than $500 per item);

• If applicable, the safe harbor for small taxpayers, where you can elect not to capitalize improvements or repairs on eligible building property (i.e., your buildings with depreciable basis less than $1 million per building; and

• The partial asset disposition elections under §1.168(i)-8(d)(2). This election is made annually to enable you to apply this section to a disposition of a portion of a prior asset that you have replaced with a subsequent improvement. An example of the application of this method is where you replace a roof on one of your buildings, and you are then able to write off the remaining depreciable basis of the prior roof. You’d make this election to avoid a situation where you will depreciate two roofs at the same time, instead of recording a loss on the disposition of the original roof.

In addition to filing these changes in accounting methods, and the making of the annual TPR elections outlined above, your internal processes that may have to be modified include:

• Accounting for ‘non-incidental’ material and supplies; and

• Establishment of a capitalization writeoff policy dictating a certain writeoff amount (e.g., “our policy is that we are going to expense all purchases under $500”). If you do not, you may be limited to a $200 per item write-off policy, including the creation of an internal writing of what actions, expenditures, or items would require capitalization (such as improvements, acquisitions, restorations, betterments, adaptions, etc.), as opposed to expenditures that would be categorized as repair and maintenance expenses.

If you do not currently have a written and communicated capitalization policy, we advise you that, in order to take advantage of the annual de minimis writeoff safe harbor described above, you must create and execute that writing and communication before Jan. 1, 2015, if you desire to employ the writeoff policy in next year’s tax returns, since the policy needs to be adopted prior to the beginning of the effected tax year. Also, review your depreciation schedules to see what assets on that list may qualify for writeoff in the 2014 tax year.

In preforming the analysis for these changes, you may find that, in applying the TPRs, your business can benefit from an additional deduction in 2014.

Conclusion

As the 2014 tax season approaches, taxpayers have a lot of questions. Will expired tax provisions be reinstated? If so, will they apply retroactively to the beginning of the year? Will they be altered? Will new tax laws make it through the legislative process?

Most importantly, how will these decisions affect your taxes?

These are legitimate concerns. Unfortunately, no one can predict the future. But we can suggest that you and your tax professionals should diligently watch the tax landscape for pending legislation that could have an impact on your taxes. Your safest course of action in the midst of uncertainty is to remain in close communication with your tax adviser for the latest guidance.

Kristina Drzal Houghton, CPA, MST is a partner with the Holyoke-based accounting firm Meyers Brothers Kalicka, and director of the firm’s Taxation Division; [email protected]

By Nicholas Yanouzas

Your property manager is awarding significant contracts to related parties.

He or she has changed the name of the payee on a check after the payee has been reported to owners.

Questionable leasing relationships have been developed by your property manager.

These are just some of the insights property owners might see if they were a fly on the wall of property managers who look out for their own best interests, instead of the owner’s.

Real-estate owners commonly hire property managers to run the day-to-day operations of an investment property with an implied trust that their manager will act ethically. A trusted property manager duly performs his or her tasks, and the owner earns the expected return on the investment. Conversely, a less scrupulous property manager takes advantage of a trustworthy owner who does not closely scrutinize transactions of their investments.

MGM Springfield’s plans to launch construction on an $800 million casino project in the spring of 2015 may just provide the confidence needed to inspire new investments in the Springfield area by out-of-town owners gaining interest in a market that is not overpriced compared to Boston and New York. Reviewing the financial operations of a property — the operational review — is often a missed opportunity by owners making real-estate investments. This checks-and-balance process gives owners the power to conduct a periodic review of the activities and transactions conducted by its property manager, details that might get overlooked in the rush of monthly and quarterly closings.

On a recent financial-operations review for a property owner in the Baltimore area, our team exposed various unexpected findings to a rather surprised owner. The owner learned that, upon review of some legal invoices, the property was being sued by the former cleaning company, which cited that the contract with the property was inappropriately terminated. On the same property, the spouse of the property manager owned a construction company that was providing in excess of $500,000 in services to the property without going out to bid and having their invoices paid within 24 hours of submission.

An operational review not only provides exposure to selected transactions, it affords the discretion of a third party to represent the owner when meeting with senior management of the property-management company. This separation allows for a candid and sometimes uncomfortable discussion about the current financial processes and procedures in place. Standardized processes and procedures would be introduced at this meeting, as needed, to provide positive business results for owners, while designing a best-practice model for property managers to implement.

While meeting with a national property-management firm regarding an apartment complex in Boston, it was determined that their process for reviewing tenant applications included a liberal policy on the credit worthiness of prospective tenants. Although this policy was beneficial to improving occupancy, the manager found that they were spending a lot of time and money on collections and evictions. The final recommendation of the operational review allowed the manager to develop a customized policy that protected the interests of the owner, while securing long-term tenants. Now the manager has additional time and resources to devote to the quality of the property, instead of chasing tenants down for rent.

Whether the real-estate investment is new or established, most owners prefer not to pay additional fees for property-management services, beyond the basic contractual terms. Operational reviews can assist owners in drilling down to see how their investment is being managed and what fees to property management are necessary or not. Knowing how assets are being managed, and what all the costs are, allows an owner to make better decisions and ask appropriate questions when selecting a property-management firm.

The ideal outcome for both owner and property manager is to have trust and transparency when issues arise and need to be communicated and resolved. And if that doesn’t happen naturally, then there’s always the operational review to intervene.

Nicholas Yanouzas is an audit partner and head of real estate at accounting and consulting firm Whittlesey & Hadley, P.C., with offices in Holyoke and Hartford, Conn.

Andrew (Drew) Andrews, managing partner of Whittlesey & Hadley

And for as long as he can remember, there have been at least a few bowls filled with various types of candy at the reception desk to tempt visitors as they arrive, depart, or, quite often, both.

“Our clients love the candy, and our employees love it as well,” he told BusinessWest, adding that, when the Hartford-based firm Whittlesey & Hadley initiated discussions to acquire Lester Halpern more than a year ago, he and others at the company — not to mention some customers — made it clear that this was one tradition they wanted to see survive a change in the name over the door.

They needn’t have worried.

Indeed, Andrew (Drew) Andrews, managing partner at Whittlesey & Hadley (or W&H, as it’s sometimes called) has long kept candy at his desk and understands its importance to the broad mission of keeping clients happy.

“I just have to stay away from it myself,” he said with a laugh, adding quickly that continuation of the candy tradition is merely one of many ways the merger with Lester Halpern — the vehicle by which W&H has made its long-planned entry into the Western Mass. market — has been smooth and essentially seamless.

Andrews said there were many things about the Lester Halpern firm that appealed to W&H as it explored various merger opportunities in this market, including its size (nearly 20 accountants and roughly $4 million in annual revenues), location in Holyoke, and the mix and size of clients in the portfolio, which includes a number of tax-exempt entities and closely held businesses.

But it was Lester Halpern’s culture that was perhaps most important to this exercise, because it closely resembles the one at Whittlesey & Hadley, said Andrews, who described it in a number of ways, starting with the word ‘collaborative.’

“At some firms, people are very protective, taking the attitude, ‘that’s my client,’” he explained. “The better answer is, ‘that’s the firm’s client,’ and what’s best for the firm’s client is what we’re going to do. That’s our philosophy, and it’s the philosophy that existed here [at Lester Halpern], and that’s one of the reasons why this transition has gone so well.”

The similarity in corporate cultures extends to the way the two firms treat staff members, he went on, adding that, at the new/old company, the preferred term is ‘team members,’ not ‘employees,’ and the phraseology speaks volumes.

“We’re very concerned about everyone’s welfare, and we have very low turnover in our shop in Hartford,” he explained. “And they [Lester Halpern]seem to have the same culture of being very concerned for their team members’ needs.”

There have been a few minor challenges to overcome since the acquisition became official on Aug. 1 — the receptionist sitting just behind the candy dish has to get in the habit of saying the company’s new name when people call, and it’s taken some practice to pronounce and spell Whittlesey properly, said Terry, adding that, overall, there have been few, if any, problems.

“You read in articles that there are always going to be some bumps and there are always going to be some issues,” he said of the transition process. “But this has gone as smoothly as a transition possibly can.”

Tom Terry says the merger of Lester Halpern and Whittlesey & Hadley has been essentially seamless.

He says to key to meeting this goal is to stress the additional resources that this ‘new’ firm can bring to the table through its operation in Hartford, and then deliver a broader array of services.

“We’re just a new player in town with added resources,” he explained. “We can provide more depth and other things that a 100-person firm can provide that a 20-person firm just can’t provide. So there’s more potential to the existing clients and the potential clients.”

For this issue and its focus on accounting and tax planning, BusinessWest talked with Andrews and Terry about this merger and what the future could hold. They both said that, while there is, indeed, a new name in this market, this is essentially the same old firm, only one that can now better serve clients.

By All Accounts

Tracing the history of the firm he joined as a staff accountant in 1984, Andrews said it was started by Bill Whittlesey in Hartford as a solo practice in 1961. He later expanded with the hiring of Bob Hadley as a staff accountant; he would become a partner in 1965.

The firm has achieved steady growth over the past 55 years or so, reaching $16 million in annual revenues and more than 100 employees at the start of this year.

Andrews, who became a partner in 1996 and managing partner in 2008, noted that, while the vast majority of clients’ firms are based in Connecticut, W&H has done some business in Western Mass. over the years, and recently made it a strategic initiative to do considerably more in the 413 area code.

Indeed, the question eventually became how, not if, the company would expand into this market, he told BusinessWest, adding that, while there were a few options, only one of them made real sense.

“We thought this was an area we really wanted to expand into, because we see a lot of similarities in culture to Hartford in this area,” he noted. “But, as in Hartford, if you’re not in the marketplace — even though it only took me 25 minutes to drive here from my office in Hartford — you’re a foreigner; you really need to live and breathe in the marketplace. I was invited once to an event that one of the banks held at the Basketball of Hall of Fame; I went with one of my partners. Everyone seemed to know each other, but no one knew us, and we felt like outsiders.

“We explored the possibility of simply opening an office, hanging out a shingle here — putting someone there and seeing what happens,” he went on. “But we didn’t think that would make a lot of headway, so we started exploring whether there was a local firm that had similarities to us in terms of how we deliver client service, how we treat employees, and wanted to get in with a larger firm so they could offer more services to their existing client base.”

W&H did some research, relying heavily on team members who lived in this area for insight, and eventually started talking with Terry and others at Lester Halpern.

“And, of course, with accounting firms, it takes a lot longer than with regular businesses to pull something like this off,” Andrews told BusinessWest, adding that talks began in January 2013, were then set aside for tax season, picked up again later in the year, and completed several months ago. “That’s because accountants, in general, are conservative, and accountants, in general, are very individualistic and like to do things their way, even though we all tend to do things in a similar fashion; it’s all about getting to know each other.”

Both Andrews and Terry said a good amount of due diligence went into making sure the fit was right between the two firms, and this research ultimately concluded that it would be an effective match.

“They [Whittlesey & Hadley] did their homework, but we did ours, too, as far as finding a partner to team up with,” he explained. “We were pretty confident that we picked the right partner, and that’s turned out to be the case. Our cultures match perfectly, our philosophy in terms of how we work with our clients — they’re very similar.

“And our clients are very similar as well,” he went on. “We both have a similar focus, with a strong not-for-profit sector in our work, but also an equally strong for-profit sector as well.”

Numbers Game

As he talked with BusinessWest about his firm’s prospects in this market, Andrews acknowledged that Western Mass. is generally considered a low- or no-growth area.

Which means that, if W&H is going to reach that goal of 7% to 8% growth for the Holyoke office, it will have to take market share from existing firms. And he believes it has the assets and attributes needed to do that.

For starters, it has the base that Lester Halpern has built over the years, he said, as well as accountants who are well-known in the Western Mass. market and understand the needs of clients here.

“We’ve tried to figure out a way to get into different markets without merging with a firm already in a market, and we haven’t been able to figure that out real well,” Andrews explained. “So that’s why we’ve gone this merger route. And one of the keys to it is to listen to the people that are already here, because they’re successful here.

“Even through we’re not that far away from each other, this is a different marketplace,” he went on. “And what succeeds in Hartford may not succeed in Western Mass. So we’re learning from our partners here, and we’re trying to do what they’ve been successful at doing since 1959 and leverage that.”

But Whittlesey & Hadley also has the resources of a much larger firm thanks to the staff, and it’s expertise, in Hartford, he went on, adding that these resources could become a strong selling point.

“As we’ve grown, pretty much organically, and become a larger firm, we’ve found that we’re better able to attract different types of talent and have in-house resources that traditionally aren’t available in smaller firms because there aren’t as many people,” he explained. “For instance, I have experts in different areas, and if my client has a complicated tax issue that’s very unique, I might have someone who’s dealt with it and is an expert on it. When you have a larger firm, you have different talents and skill sets, and you can provide a more-in-depth package of services to your existing client base.”

Terry agreed, and told BusinessWest that, in just the first 20 days of operating under the W&H umbrella, there were instances where he called on that expertise Andrews mentioned, and to the benefit of clients.

“There have been three instances already where clients have had questions that I would not have been able to answer,” he explained. “But because of the very strong tax department that’s located down in Hartford, I’ve been able to use those resources — and we’re only three weeks into it.

“We’re really just getting started,” he went on, “and to have that resource is extremely helpful.”

One of the challenges ahead for W&H is to make the region more familiar with the company’s name, acronym, and operating culture, said Andrews, adding that the firm intends to be visible, with some aggressive marketing as well as involvement with many area business organizations and their events and programs.

Ultimately, though, word of mouth will carry the most weight, he said, adding that, if the company can provide the depth and quality of service that he believes it will, that will be the best way to get the word out and build market share.

The Bottom Line

On the day BusinessWest visited the W&H facility on Bobala Road, the company’s new signage was not yet in place — it will be arriving later this month.

And outwardly, there were few, if any, signs (literally or figuratively) that anything had changed. Indeed, there were three bowls at the reception desk containing everything from chocolate to jellied candy.

But some change has come to the business beyond a new name, said Andrews and Terry, adding that, mostly, there is new opportunity to make this operation a stronger force in the local accounting market. n

George O’Brien can be reached at [email protected]

By CHRIS MARINI

Tax season can often be a stressful time of year for just about everyone. The key to reducing this stress is keeping records organized and accessible.

Christopher Marini

By following the eight tips below, your next tax return will be quicker and more accurate than ever before.

1. Keep All Documents Together

By ensuring that all tax-related documents are kept in the same spot, you can eliminate questions such as ‘where did I put that?’ or ‘did I ever receive that?’ This could potentially save hours spent searching a home or, even worse, weeks spent waiting for an additional copy to be mailed to you. Documents received throughout the year may include real-estate and excise-tax bills, medical bills, co-pays, and prescriptions. In addition to those documents, and your own records maintained throughout the year, here is a brief list of the most common forms people receive after year end:

• W2 (wages)

• 1099-MISC (independent contracting)

• 1099-DIV (dividend income)

• 1099-SSA (Social Security proceeds)

• 1098 (home mortgage taxes/interest)

• K1 (partnership income)

• 1099-INT (interest income)

• 1099-B (capital gains)

• 1099-R (retirement distributions)

• 1098-T (higher-education tuition)

2. Stay on Top of Withholdings

If you had a large amount of taxes due in past years, you may find yourself in a similar situation this year. There are several methods available to ensure you withhold enough taxes throughout the year to avoid the burden of having to make a single large payment and incurring any related penalties.

One potential way is to change how much you are withholding from your W2. Your company’s HR department can help you change this on your Form W4. Lower numbers mean more tax is withheld, so if you are claiming a 2 and owe taxes, consider changing to a 1 or 0. Another possible method to help withhold enough is by using estimated tax payments. Estimates are quarterly prepayments of taxes, which are often used by business owners or individuals with a high level of income. Also, remember to inform your tax preparer of any life changes, such as marriage, divorce, birth of a child, or death of a spouse, which can affect how much withholdings are needed.

3. Regularly Update Mileage Logs (Form 4562/2106)

If you own a small business or have unreimbursed mileage expenses from a job, you are able to claim this as a deduction on your return. You can claim this deduction using the standard mileage rate or actual expenses. The key to either method is having supporting documentation to help keep your audit trail accurate.

In order to calculate your deduction properly, it is important to keep detailed records of your mileage. One quick and easy strategy you might try is purchasing a small pocket notebook and keeping it in your center console. Whenever you use your vehicle for a business trip, simply set your odometer and jot down the miles (excluding commuting mileage).

If you forget to set the odometer, Google Maps is always a useful tool. At the end of the year, add up all the trips in the notebook to arrive at your total business mileage. Additionally, remember to keep your receipts for parking and tolls, and add them up at year end as well.

4. Summarize Higher-education Costs (Form 8863)

Each higher-education institution you or your child attends is required to issue a 1099-T; however, there is often additional information to consider that is not included on a 1099-T. This includes amounts paid for books, a well as scholarships and grants received that were not paid directly to the school.

Because it is important to capture all activity, consider making a summary sheet of all education costs and assistance received. Costs should include all amounts from the college bill in addition to textbooks. Remember to keep copies of all book receipts as backup documentation.

5. Keep Track of Fair Rental Days (Schedule E)

If you rent out a vacation home, it is necessary to know how many days it was rented at fair rental value. Your tax preparer will also need to know how many days the home was used by either yourself or any family member.

To do this, try keeping a miniature monthly calendar at home, exclusively for the purpose of keeping track of usage. For any day that it is used personally or by a family member, put a ‘P’on the day for ‘personal.’ For any day that it is rented to someone at fair rental value, put an ‘R’ on that day for ‘rented.’ At the end of the year, go through your calendar and determine the amount of days used personally and rented out.

6. Substantiate Business Revenue and Expenses

For small business owners who file a Schedule C, E, or F, it is important to keep detailed and supported records. Purchasing a computer program, such as QuickBooks, will help you keep better track of business data. To maintain a proper audit trail for your business, be sure to maintain supporting documentation for each transaction you enter into your software.

For the very small businesses, it may not be cost-effective to purchase financial software. If you fall into this category, try keeping a bin at your desk to store copies of each check for revenue and receipts for expenses. Then, on a monthly basis, use a blank spreadsheet or notebook to record all data from the bin. This will be much easier than trying to summarize all 12 months at once. Keep in mind that charge-card statements cannot be used to substantiate deductions; rather, detailed receipts are needed.

7. Keep a Log of Childcare Expenses (Form 2441)

Parents who both have earnings can deduct expenses paid to a childcare provider, which includes day cares, independent sitters, and summer camps. For each expense, keep records of which child the expense relates to. Additionally, you will need to request the EIN or SSN for each provider.

Keep a log of these expenses at home, and update it each time you write a childcare check. To create an even more effective audit trail, include copies of checks paid to each childcare provider or ask them to provide you with a statement of annual amounts paid. At year end, use the log to create a summary sheet, totaling by child and then provider.

8. Maintain Records of Charitable Contributions (Schedule A)

Make your donations with checks or online. The IRS will not allow a deduction for unsupported cash donations. Additionally, remember to take copies of each check or online payment as proof of each payee and amount. At the end of the year, create your summary sheet, breaking down the amounts paid to each organization, with the supporting copies attached behind as additional backup documentation. There are more stringent rules for larger donations, so be sure to consult your tax preparer.

Also, if any benefit is received as a direct result of the contribution, it must be subtracted from the contribution amount. For example, if you donated $1,000 to the Jimmy Fund and received two Red Sox tickets valued at $50 each, you could deduct only $900.

By following whichever of these eight tips apply to you, you will make your next tax return quicker and easier to prepare, and more accurate. Additionally, in the event you are ever audited, you can feel confident in the ability of your backup documentation to uphold the figures presented on your return.

So, this year, challenge yourself to get organized, and make your tax return a year-round commitment.

Chris Marini is an audit and accounting associate with the Holyoke-based public accounting firm Meyers Brothers Kalicka, P.C.; (413) 322-3549; [email protected]

By JAMES BARRETT

The first half of 2014 has produced little in the way of major tax legislation, but tax-planning opportunities still exist.

The first half of 2014 has produced little in the way of major tax legislation, but tax-planning opportunities still exist.

This mid-year tax-planning article focuses on plans that may take a little more time to implement rather than on strategies that must be executed in the limited time remaining at year-end.

Tax Planning for Individuals

Managing Your Income

Income-tax planning typically involves some combination of three strategies:

• Earn income taxed at favorable tax rates, such as long-term capital gains or qualified dividends;

• Avoid income bubbles, which can cause you to be subjected to a higher marginal tax rate in the ‘bubble year’ than your normal, or average, marginal tax rate; and

• Delay the payment of tax by deferring the receipt of income to a later year or accelerating the payment of deductible expenditures into the current year.

James Barrett

When you are estimating your income for 2014, you may want to consider several target figures:

Paying Your Income Taxes

If you do not pay enough tax throughout the year, penalties may apply. But with proper planning, the penalties are avoidable.

If it appears that you will be subject to an underpayment penalty, you may be able to reduce or eliminate the penalty by initiating or increasing your quarterly estimated tax payments. If you’re employed, instructing your employer to withhold more from your pay can even eliminate penalties that accrued earlier in the year. A quirk in the penalty rules treats withheld taxes — even withholding that occurs late in the year — as if they had been taken evenly throughout the year.

While most people want to avoid unnecessary penalties, it is seldom a good idea to pay more than the law requires or to pay your taxes earlier than necessary. Why let the government hold your money only to return it to you next year as a tax refund — with no interest?

Your goal should be to pay just enough to avoid an underpayment penalty but not so much as to create a large refund. If it looks as if you have been paying too much tax, cut back on your withholding or lower your remaining quarterly estimated tax payments.

Funding Your Retirement Plans

Contributing to a tax-qualified retirement plan can reduce your current tax obligations and help you save for your retirement in a tax-efficient manner. Contributions and the earnings on them provide tax deferral on earnings until you receive distributions.

In the case of Roth IRAs, the tax deferral may be permanent. So the sooner you make the contribution, the sooner your tax-deferred earnings begin. If you already have a plan in place, consider making a contribution now rather than waiting until the last minute.

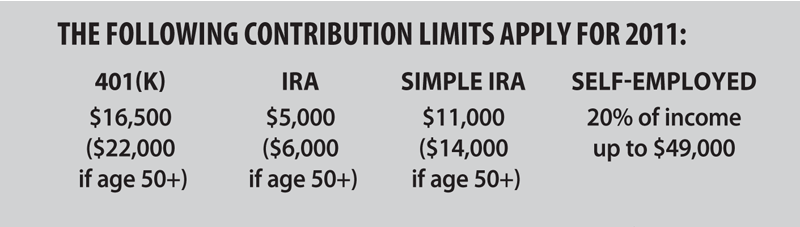

The following limits apply for the 2014 tax year:

• Participants in a 401(k) plan can defer up to $17,500 ($23,000 for ages 50 or older);

• The IRA contribution limit is $5,500 ($6,500 for ages 50 and older);

• Simple IRA participants can defer up to $12,000 ($14,500 for age 50 and older);

• Self-employed individuals can contribute 20% of their self-employment income up to $52,000.

IRAs and Roth Accounts

Anyone with earned income, including alimony, is generally eligible to contribute to an IRA. That means that a child who has a job can set up an IRA and begin saving for retirement.

Claiming a deduction for your contribution to a traditional IRA is another matter. It depends on your income and whether you (or your spouse if you are married) are covered by an employer-sponsored retirement plan. Contributions to a Roth IRA are never deductible.

• If neither you nor your spouse is covered by an employer’s plan, you may choose to deduct your contribution to your traditional IRA.

• At higher income levels — modified adjusted gross income above $70,000 for singles and $116,000 for joint filers — no deduction is allowed if you (and your spouse if you are married) are covered by an employer’s plan.

• If you are married and only one of you is covered by an employer’s plan, the spouse who is not covered may claim the deduction, unless your joint modified adjusted gross income exceeds $191,000.

Many people find the long-term benefits of contributing to a Roth IRA or a Roth 401(k) outweigh the short-term financial benefits of tax-deductible contributions. While Roth contributions are not tax-deductible, none of the income earned in the Roth account will ever be subject to income tax unless there are early distributions.

In addition, the Roth account is not subject to the lifetime required minimum distribution rules that apply when you reach age 70½.

Eligibility to contribute to a Roth IRA depends on the amount of your income. No contribution is allowed if your modified adjusted gross income for 2014 exceeds $129,000 for singles or $191,000 for joint filers.

You can make a direct rollover from your traditional IRA or other qualified retirement plan into a Roth IRA. However, you must pay tax on the rollover amount. There is no income limit associated with Roth rollovers.

‘Magic-age’ Years

Is 2014 a magic-age year for you? There are two ages that affect retirement plans, and both involve a ‘half birthday.’ Once you reach age 59½, the extra 10% penalty no longer applies to distributions from your qualified retirement plans, including IRAs.

But if you reach age 70½ during 2014, you must begin to receive minimum distributions from your traditional IRAs. Although the first annual distribution need not be taken until April 15, 2015, you may want to take the first distribution during 2014, to avoid the need for two distributions in 2015.

Changes to the 60-day Rollover Rule

This year (2014) will be the last year that you can obtain multiple short-term tax-free loans from your IRAs. A withdrawal from your IRA is treated as a tax-free transaction if you redeposit the amount into the same or another IRA no later than 60 days after the date you made the withdrawal. Note that the IRS may waive the 60-day requirement under some circumstances, for example, such as an error by your financial institution.

You are allowed only one tax-free rollover per year. The one-year waiting period begins on the date you receive the IRA distribution, not on the date you roll it back into another IRA.

For years, the IRS had said that the one-year waiting period applied separately to each of your IRAs. After the Tax Court interpreted the rule differently in its Bobrow decision (TC Memo 2014-21), the IRS decided to treat all of your IRAs as one IRA for the purposes of the one-year waiting period. However, the IRS says it will not apply this more restrictive interpretation to any rollover that involves a distribution from an IRA before Jan. 1, 2015.

Rollovers between Roth IRAs are subject to the same 60-day rule and one-year waiting period that apply to rollovers between traditional IRAs. After 2014, all of your Roth IRAs will be treated as one Roth IRA for purposes of the one-year waiting period between rollovers.

Rollovers from employer retirement plans to IRAs do not count for purposes of the one-year waiting period. Similarly, conversions of regular IRAs to Roth IRAs are not considered. The one-year waiting period also does not apply to trustee-to-trustee transfers between traditional IRAs or between Roth IRAs.

Making Your Home Energy-efficient

While most of the residential energy tax credits expired at the end of 2013, one remains in effect — the credit for qualified expenditures made for residential energy-efficient property placed in service before Jan. 1, 2017. The IRS defines qualified expenditures for residential energy-efficient property to include:

• Qualified solar electric property expenditures for use in a qualifying dwelling unit;

• Qualified solar water-heating property expenditures for property that heats water for use in a qualifying dwelling unit, if at least half of the energy used by the property for such purpose is derived from the sun;

• Certain qualified fuel-cell property expenditures;

• Qualified small wind-energy property expenditures for property that uses a wind turbine to generate electricity for use in connection with a qualifying dwelling unit; and

• Certain qualified geothermal heat-pump property used to heat a dwelling unit or as a thermal energy sink to cool the dwelling unit, which meets the requirements of the Energy Star program.

The residential alternative energy credit is equal to 30% of the cost of eligible solar water heaters, solar-electricity equipment, fuel-cell plants, small wind-energy property, and geothermal heat-pump property.

You may rely on a manufacturer’s certification that property is eligible for the credit, so long as the IRS has not withdrawn the manufacturer’s right to make the certification.

Complying with the ACA

Starting in 2014, lower-income individuals may be eligible for a tax credit to help pay for health-insurance coverage purchased through an affordable insurance exchange established by the Affordable Care Act. The credit is refundable, so those with little or no income-tax liability can still benefit. The credit also can be paid in advance to the insurance company to help cover the cost of premiums.

Starting in 2014, the individual shared-responsibility provision calls for each person to have minimum essential coverage for each month, qualify for an exemption, or make a payment when filing his or her federal income-tax return. The open-enrollment period to purchase health insurance coverage for 2014 through the Affordable Insurance Exchange ran from Oct. 1, 2013 through March 31, 2014.

Keeping Good Records

Every April, most people resolve that they are going to keep better tax records … next year. While it is obvious that, if you do not keep good records, you are likely to overlook legitimate tax deductions, the result could be even harsher.

In the Durden decision (TC Memo 2012-140), the Tax Court disallowed a couple’s charitable-contribution deduction to their church even though they could prove the payments with canceled checks. The tax law requires a contemporaneous written acknowledgment from the charity for gifts of $250 or more.

In this case, the couple obtained the required letter after their tax return was being examined by the IRS. The court denied the deduction because the letter was not issued prior to the due date of the tax return as required by the tax law.

Business Activities

Whether you own your business or work for someone else, a number of tax-saving opportunities could be available to you if you stay alert and keep good records.

Changing Jobs

Costs you incur in seeking new employment may be deductible if you itemize. And if you have to relocate, the cost of moving yourself and your family may be deductible — even if you don’t itemize.

As with most provisions of the tax law, a review of the technical rules is necessary to determine whether you qualify. Be sure to contact your tax adviser.

Hiring Your Children

If you own a business and have children, consider putting them to work during summer vacation or after school. You will be able to deduct their wages, as long as you make their pay commensurate with what you would pay non-family employees for the same services.

For 2014, each child can earn as much as $6,200 and pay zero income tax. A child who earns $11,700 and contributes $5,500 to a traditional IRA will also pay zero income tax.

Honing Your Job Skills

Parents of college-age students are generally aware of education tax credits like the American Opportunity Credit. If you undertake training to maintain or enhance your job skills or if you pursue an additional degree, you may qualify for the Lifetime Learning Credit or be able to deduct the cost of your education or training as an itemized deduction.

Talk with your tax adviser. Not only are you never too old to learn, but you’re also never too old to claim a tax benefit.

Working from Home

If you operate a business from your home and use a distinct room or area solely for business activities, you may qualify for a home-office deduction. The IRS has simplified the record-keeping requirements but not the qualification requirements. In rare cases, employees who are required by their employer to work from home may also qualify for this deduction.

Caring for Dependents

Working couples with young children and those caring for aged relatives often incur costs associated with hiring outside caregivers so that they can work or go to school. Some of these costs may qualify for the dependent-care tax credit. Qualifying costs may include day camp and similar activities during the summer months.

Establishing a Retirement Plan

If you own a business, you may be able to avail yourself of a defined-benefit type of retirement plan. These plans often allow higher retirement contributions than other types of plans. The higher retirement benefit must be weighed against the additional cost of providing comparable retirement benefits for your employees.

To qualify for a tax deduction in 2014, your retirement plan generally must be in place before the end of the year. Exceptions are IRA and SEP (simplified employee pension) plans, which can be set up through April 15, 2015.

Small employers — generally those with 100 or fewer employees — that set up a qualified retirement plan may be eligible for a tax credit of up to $500 per year for three years. The credit is limited to 50% of the qualified startup costs.

Writing Off Capital Expenditures

Generous business-tax write-off rules, like bonus depreciation, expired at the end of 2013. And the expensing election limit under Section 179 has been reduced to $25,000 for 2014, but only if the total amount of qualified asset purchases does not exceed $200,000.

Depreciating Vehicles

For passenger automobiles first placed in service during 2014, the deduction limitations for the first three tax years are $3,160, $5,100, and $3,050, respectively, and $1,875 for each succeeding year. For trucks and vans first placed in service in 2014, the depreciation limitations for the first three years are $3,460, $5,500, and $3,350, respectively, and $1,975 for each succeeding year.

In past years, bonus depreciation made the first-year limitation much higher. However, since bonus depreciation expired on Dec. 31, 2013, the new limits will apply for 2014 unless Congress acts to reinstate bonus depreciation retroactively to Jan. 1, 2014.

Repairing Older Assets

For tax years beginning in 2014, new rules are in effect for determining when expenditures can be deducted as a repair expense and when they must be treated as the cost of a new asset subject to depreciation. All businesses should review their repair/capitalization policies to assure that they are in compliance with the new rules.

Monitoring Passive Activities

Complex rules govern the tax treatment of business activities in which the owner does not materially participate. If these so-called passive activities produce a loss, that loss may not be currently deductible. If the passive activity is profitable, the income could be subject to the 3.8% surtax on net investment income.

If you are the owner of a business, it’s a good idea to keep detailed records of the hours you spend working in the business. This record keeping is especially important if you have another full-time job or if the potentially passive activity is not your primary business endeavor.

Estate Planning

For 2014, the unified credit for estate and gift taxes has been raised so that the tax applies only to estates greater than $5.34 million. And the estate-tax exclusion is portable, so if you and your spouse have combined estates that do not exceed $10.68 million, you can avoid the estate tax without the necessity of including language in your will creating a bypass trust.

The annual gift-tax exclusion for 2014 remains at $14,000 per person. Therefore, if you are married, you can gift up to $28,000 per donee, or recipient, this year without any federal gift-tax ramifications by using the gift-splitting rules. Gifting is a good way to reduce your taxable estate and may be an important element of your estate plan.

You may have executed your current will and estate plan without consideration of the increased unified credit amount and the portability feature of the new estate-tax law. If so, a review is in order to make sure your assets will be handled in the most tax-efficient manner.

Offshore Account Disclosures

If, during 2013, you had a financial interest in, or signature authority over, at least one financial account located outside the U.S., and the aggregate value of all your foreign financial accounts exceeded $10,000 at any time during the calendar year, you must file electronically with the Treasury Department a Financial Crimes Enforcement Network (FinCEN) Form 114, Report of Foreign Bank and Financial Accounts (FBAR).

The new Form 114 replaces TD F 90-22.1 and is due to the Treasury Department by June 30, 2014. The form must be filed electronically and is available only online through the BSA E-Filing System website (bsaefiling.fincen.treas.gov/main.html).

In Conclusion

Tax planning is an ongoing process. Your tax picture can change — sometimes dramatically — during the course of a year, and you need to react accordingly. Implementing thoughtful mid-year strategies now may help you lessen the taxes you face in April 2015.

One final thought: saving taxes is generally a good strategy. But making a bad business, investment, or personal decision just to save some tax dollars is never a good strategy.

James Barrett is managing partner of Meyers Brothers Kalicka in Holyoke; (413) 536-8510; [email protected]

By MARK J. COREY, CPA

Several well-known tax breaks have expired in 2014, and absent Congressional action to renew them, they will not be available for taxpayers in 2014.

There has been discussion by the Senate and the House to renew some or all of the expired provisions, but no laws have been passed. While indications are that at least some of these provisions may eventually be extended, if the expiration of these commonly used tax provisions has a significant impact on you or your business, you may want to prepare by adjusting withholdings and estimated tax payments just in case.

Expired Provisions Affecting Individuals

Mortgage-insurance Premium Deductions

Homeowners were allowed to deduct qualified mortgage-insurance premiums by treating them as home-mortgage interest.

Mortgage Debt Relief

Generally, cancelled or forgiven debt is considered taxable income. However, up to $2 million of cancelled principal-residence mortgage debt could be excluded from taxable income if the debt was discharged on or after Jan. 1, 2007, and before Jan. 1, 2014, as a result of foreclosure, short sale, or mortgage restructuring.

State and Local General Sales-tax Deduction

Taxpayers had the option to deduct sales tax instead of state income tax in years before 2014. This provision was especially beneficial for individuals who lived in states with no income tax.

Educator Out-of-pocket Expenses Deduction

For many years, elementary and secondary school teachers enjoyed an above-the-line deduction of up to $250 for out-of-pocket expenses for school and classroom-related expenses.

Tuition and Fees Deduction

Taxpayers were able to deduct above-the-line qualified higher education expenses. Taxpayers will no longer get this deduction for 2014, but the Lifetime Learning Credit and American Opportunity Credit will still be available for college students.

Non-business Energy Credit

This credit for the installation of qualified energy-efficiency improvements, such as insulation, windows, doors, and roofs, as well as certain water heaters and qualified heating and air-conditioning systems, expired Dec. 31, 2013.

Expired Provisions Affecting Businesses

Expanded IRC Section 179 Expensing

For tax years beginning in 2010 and through 2014, taxpayers were allowed to expense up to $500,000 for eligible property additions that they would have otherwise capitalized and depreciated over their useful lives, provided the eligible additions did not exceed $2 million. The Section 179 deduction dropped to $25,000 for tax years beginning on or after January 1, 2014.

Bonus Depreciation

A bonus depreciation deduction was allowed for qualifying fixed assets acquired and placed in service from 2007 through 2013. The rate was generally 50%; however, for qualifying assets placed in service from Sept. 9, 2010 through Dec. 31, 2011, the rate was 100%. For 2014 and future years, there is no current bonus depreciation allowed except on long-production property and certain non-commercial aircraft, for which the expiration was extended by one year to Dec. 31, 2014.

Retail and Restaurant Improvements

Certain qualified business assets were allowed a shorter life for depreciation purposes. Qualified leasehold improvements and restaurant improvements, placed in service from Oct. 23, 2004 through Dec. 31, 2013, were depreciated over 15 years. Qualified retail-store improvements, placed in service from Jan. 1, 2009 through Dec. 31, 2013,were also depreciated using a 15-year life. For these types of additions placed in service in 2014, the depreciable life generally reverts back to 39 years but depends upon the individual type of expenditure.

R & D Tax Credit

Taxpayers were allowed a tax credit equal to 20% of the excess of qualified research expenses for the current year over the prior year, basic research payments made to qualified organizations, and specific energy-research-consortium expenditures paid or incurred through Dec. 31, 2013.

Conclusion

There are many well-known and popular tax breaks that expired prior to 2014. On April 28, 2014, the Senate introduced the EXPIRE (Expiring Provisions Improvement, Reform, and Efficiency) Act of 2014 to extend more than 50 expired tax breaks and benefits. That same day, the bill was approved by the Senate Finance Committee but has advanced no further due to disagreements on procedural issues. The House has taken a different approach, and the House Ways and Means Committee has passed 12 separate tax bills, including seven for business-tax extenders and five related to charitable deductions.

One of the business-extender bills, a simplified research-credit bill which would make the extension permanent, was passed by the House, and it is expected that the remaining 11 bills will be considered prior to the August recess. Given the different approaches by the House and Senate, reaching agreement may be a challenge. n

Mark J. Corey is a senior tax manager in the Springfield office of Wolf & Co., P.C. Wolf is a leading regional certified public accounting firm with offices in Springfield, Boston, and Albany, N.Y., which provides accounting, tax, and consulting services to individual and business clients.

Kristina Drzal-Houghton

Individual Tax-rate Management

In prior years, the main concern was that, if you reduced your regular income tax too far, the alternative minimum tax (AMT) would step in to appropriate your hard-earned tax savings. There are now additional dynamics to consider, when certain thresholds are exceeded, in the form of a 3.8% net-investment-income (NII) tax levied on investment income, a 0.9% Medicare payroll tax levied on wages and self-employment earnings, and a multi-tiered, long-term capital-gains tax-rate structure.

These new taxes, beginning in 2013, apply when adjusted gross income exceeds certain thresholds ranging from $200,000 for single filers to $250,000 for married taxpayers. For these thresholds and most others mentioned in this article, married filing separate uses one-half the married threshold.

Additionally, the 39.6% tax bracket returns this year after a long hiatus for taxpayers above thresholds ranging from $400,000 of taxable income for single filers to $450,000 for married filers.

Net investment income tax. The 3.8% NII tax now applies to most investment income. For individuals, the amount subject to the tax is the lesser of (1) the net investment income; or (2) the excess of modified adjusted gross income (MAGI) over the applicable threshold amount.

NII includes dividends, rents, interest, passive-activity income, capital gains, annuities, and royalties. Passive pass-through income will be subject to this new tax, but non-passive will not. Self-employment income, income from an active trade or business, and portions of the gain on the sale of an active interest in a partnership or S corporation with investment assets, as well as IRA or qualified plan distributions, are not subject to the NII tax.

• Planning point: Weighing a decision about selling marketable securities to meet current cash needs? Consider using margin debt for replacement securities. The interest on the debt will be deductible, subject to the investment-interest limitation, which could reduce your NII for purposes of the new tax.

• Planning point: To the extent your NII is income from a passive activity, increasing your material participation in the activity between now and the end of the year can reduce the amount of income subject to the NII tax. Proceed with caution, though, because a change in participation level may impact other short- and long-term tax obligations.

• Planning point: As you near the applicable threshold, consider revising the timing of distributions from retirement plans to manage your net investment income. While the distributions themselves are not NII, the distributions increase your MAGI, which could subject more of your investment income to the NII tax.

Increased maximum tax rates on long-term capital gains. While avoiding or deferring tax may be your primary goal, to the extent there is income to report, the income of choice is long-term capital gain income thanks to the favorable tax rates available. The available rates differ depending on the taxpayer’s tax bracket.

Taxpayers in the 39.6% bracket will now pay a 20% long-term capital gains and qualified dividends rate. Additionally, those above the previously noted thresholds will pay the 3.8% tax in addition to the increased capital-gains rate.

• Planning point: The netting rules provide an opportunity to manage the net gain or loss subject to taxation, making it prudent to review your investment gains and losses before the close of year to determine whether additional transactions prior to year-end may improve your tax outlook.

Recognition of same-sex marriage for federal tax purposes. Beginning in 2013, legally married same-sex couples must file a joint or married-filing-separately return. The rules do not extend to cover domestic partnerships. The ruling is retroactive, opening up a refund opportunity in certain circumstances for those who were previously prohibited from joint filing. Amended returns may be, but are not required to be, filed for tax years still open by statute of limitations.

Year-end Timing Strategies

Managing the alternative minimum tax. The AMT applies when income, as adjusted for certain preference items, exceeds certain exemptions, but the rate applied to that income falls below the AMT rate, essentially acting as a tax-leveling mechanism. Residents of states with high income and property taxes, like Connecticut and Massachusetts, are more likely to be subject to the AMT because these state taxes are not deductible when computing AMT income.

The AMT exemptions are subject to phaseouts when AMT income exceeds $115,400 for single filers and $153,900 for married joint filers.

Delaying or prepaying expenses. As a cash-method taxpayer, you can deduct expenses when you pay them or charge them to your credit card. Payment by credit card is considered paid in the year the charge is incurred. Expenses that are commonly prepaid in connection with year-end tax planning include:

Charitable contributions. A tax deduction is available for cash contributions to qualified charities of up to 50% of adjusted gross income (AGI) and up to 30% (20% for gifts to private operating foundations) of your AGI for charitable gifts of appreciated property.

• Planning point: Consider contributing appreciated securities that you have held for more than one year. Usually, you will receive a charitable deduction for the full value of the securities, while avoiding the capital-gains tax that would be incurred upon sale of the securities.

State and local income taxes. Consider prepaying any state and local income taxes normally due on Jan. 15, 2014, or with the filing of the return if you do not expect to be subject to the AMT.

• Planning Point: If you expect to owe state and/or local income tax when you file your return for 2013, consider paying that amount before Dec. 31, 2013. Although you relinquish your cash in advance, the benefit from accelerating the tax deduction and lowering your current federal income tax could be significant. It is particularly powerful if the deduction could be lost through the AMT in 2014. Just be careful that your prepayment does not make you subject to AMT in 2013.

Real-estate taxes. Like state and local income taxes, real-estate tax levies due early in 2014 can often be prepaid in 2013. For real-estate taxes on your residence or other personal real estate, just be mindful of the AMT in both years. Real-estate tax on rental property is deductible whether or not you are subject to AMT, and it can be safely prepaid.

Mortgage interest. There are limits on your ability to deduct prepaid interest. However, to the extent your January mortgage payment reflects interest accrued as of Dec. 31, 2013, a payment prior to year-end will secure the interest deduction in 2013.

Other itemized deductions. Miscellaneous itemized deductions, like many deductions, are deductible only if you itemize your deductions and are not subject to AMT. Where miscellaneous itemized deductions differ is with the requirement that the total deductions exceed 2% of your AGI to be deductible.

Itemized deduction phaseout. After a three-year hiatus, 2013 marks the return of the phaseout of certain itemized deductions for higher-income taxpayers. For affected taxpayers, itemized deductions are reduced by 3% of the amount by which AGI exceeds thresholds ranging from $250,000 for a single filer to $300,000 for married joint filers.

However, deductions for medical expenses, investment interest, casualty and theft losses, and gambling losses are not subject to the limitation. Taxpayers cannot lose more than 80% of the itemized deductions subject to the phaseout.

Exemption phaseout. A personal exemption is generally available for you, your spouse if you are married and file a joint return, and each dependent (a qualifying child or qualifying relative who meets certain tests). In 2013, the exemption amount is $3,900, subject to a reinstated phaseout of the exemption for higher-income taxpayers. These phaseout thresholds begin at the same AGI limits discussed for itemized deductions above.

Retirement-plan distributions. If you are over age 59½ and your 2013 income is unusually low, consider taking a taxable distribution from your retirement plan, even if it is not required, to use the unusually low tax rate for the period. More powerful still, consider converting the funds to a Roth account.

• Planning point: If you expect to be in a higher tax bracket in the future, consider converting your traditional IRA into a Roth IRA during your lower-income years. You will be paying taxes early, but future appreciation of the assets in your account may escape income taxes entirely.

IRA distributions to charity. If you are over age 70½, you can make a tax-free distribution of up to $100,000 from your IRA to a qualified charity before Dec. 31, 2013. Under current law, this opportunity will not be available for 2014.

Note that this opportunity is doubly powerful beginning in 2013. In addition to prior tax benefits, now the IRA is not included in your MAGI, and thus this strategy may reduce exposure to the new 3.8% NII tax.

Worthless securities and bad debts. Both worthless securities and bad debts could give rise to capital losses. Since no transaction generally alerts you to this deduction, you should review your portfolio carefully.

• Planning point: If you own securities that have become worthless or made loans that have become uncollectible, ensure that the losses are deductible in the current year by obtaining substantive documentation to support the deduction.

Contributing to a retirement plan. You may be able to reduce your taxes by contributing to a retirement plan. If your employer sponsors a retirement plan, such as a 401(k), 403(b), or SIMPLE plan, your contributions avoid current taxation, as will any investment earnings until you begin receiving distributions from the plan. Some plans allow you to make after-tax Roth contributions, which will not reduce your current income, but you will generally have no tax to pay when those amounts, plus any associated earnings, are withdrawn in future years.

You and your spouse must have earned income to contribute to either a traditional or a Roth IRA. Only taxpayers with modified AGI below certain thresholds are permitted to contribute to a Roth IRA. If a workplace retirement plan covers you or your spouse, modified AGI also controls your ability to deduct your contribution to a traditional IRA. There is no AGI limit on your or your spouse’s deduction if you are not covered by an employer plan. If your modified AGI falls within the phaseout range, a partial contribution/deduction is still allowed.

• Planning point: If you would like to contribute to a Roth IRA, but your income exceeds the threshold, consider contributing to a traditional IRA for 2013, and convert the IRA to a Roth IRA in 2014. Be sure to inquire about the tax consequences of the conversion, especially if you have funds in other traditional IRAs.

Other Personal Tax-planning Considerations

Withholding/estimated tax payments. With higher rates in effect for 2013, more taxpayers may find themselves exposed to an underpayment penalty. Underpayment penalties can be avoided when total withholdings and estimated tax payments exceed the 2012 tax liability or, in the case of higher-income taxpayers, 110% of 2012 tax.

• Planning point: If you expect to be subject to an underpayment penalty for failure to pay your 2013 tax liability on a timely basis, consider increasing your withholding between now and the end of the year to reduce or eliminate the penalty. Increasing your final estimated tax deposit due Jan. 15, 2014 may reduce the amount of the penalty, but is unlikely to eliminate it entirely. Withholding, even if done on the last day of the tax year, is deemed withheld ratably throughout the tax year.

Losses from pass-through business entities. If your ability to deduct current-year losses from a partnership, LLC, or S corporation may be limited by your tax basis or the ‘at-risk’ rules, consider contributing capital to the entity or, in some cases, making a loan to the entity prior to Dec. 31, 2013, to secure your deduction this year.

• Planning point: If you anticipate a net loss from business activities in which you do not materially participate, consider disposing of the loss activity by Dec. 31, 2013. Assuming sufficient basis exists, all suspended losses become deductible when you dispose of the activity. Even if there is a gain on the disposition, you may still benefit from having the long-term capital gain taxed at 23.8% (inclusive of the NII tax) with the previously suspended losses offsetting other ordinary income.