Stay on the Right Side of the IRS and Minimize Your Tax Liability

By JAMES BARRETT

Tax planning for 2015 is a venture in uncertainty.

Tax planning for 2015 is a venture in uncertainty.

Last December, Congress passed legislation extending a number of expired tax provisions. Unfortunately, they were extended only until Dec. 31, 2014. At this point, we don’t know their status for 2015 and beyond.

There has been a great deal of talk about tax simplification, but currently, it appears to be all talk with no substance and little momentum for achieving true reform.

On April 16, the U.S. House of Representatives voted to repeal the estate tax, but this was seen as a largely symbolic gesture because the U.S. Senate does not appear to have enough votes to pass the legislation. Even if the bill were to survive the Senate, President Obama is likely to veto it. The House is apparently attempting to keep the issue in the forefront with an eye to repeal in 2017.

Rules regarding IRA rollovers have changed. As of 2015, taxpayers may make only one IRA-to-IRA rollover per year. This does not limit direct rollovers from trustee to trustee.

James Barrett

It should also be pointed out that the penalty for failure to maintain qualifying health insurance takes a big leap in 2015. The penalty is the greater of $325 for each adult and $162.50 for each child (but no more than $975) or 2% of household income minus the amount of the taxpayer’s tax-filing threshold.

Dealing with the IRS has become more difficult as a result of budget cuts that make it difficult to reach IRS personnel by phone or in person at most offices. On the flip side, the chances of being audited by the IRS are at the lowest they have been for years. However, the IRS remains quite proficient at sending out computer-generated notices, usually from document-matching processes.

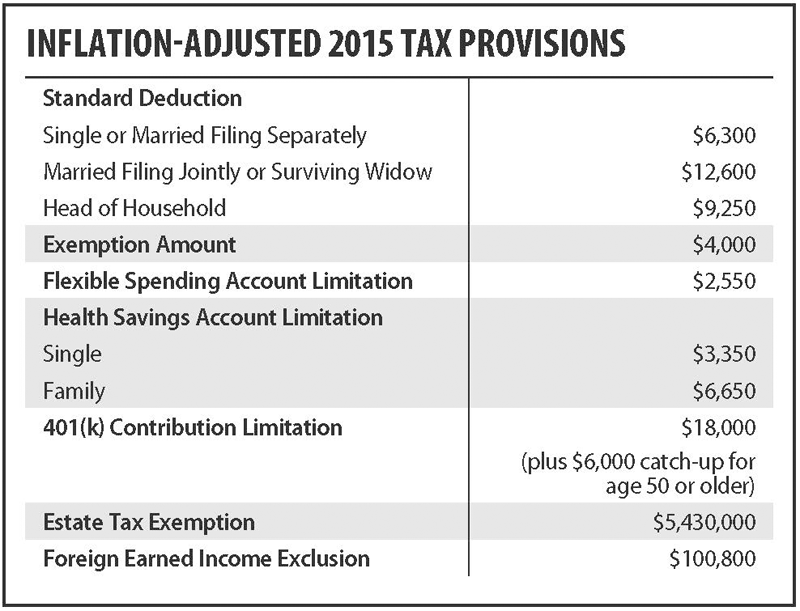

Inflation Adjustments

As usual, there are some adjustments to a number of tax-related amounts for 2015.

The personal and dependency exemptions were increased by $50 per individual. The standard deduction for all filing statuses increased between $100 and $200, while the additional standard deduction for taxpayers who are age 65 and over or blind increased $50 for both married statuses but did not increase for head-of-household or single filers.

Tax brackets, along with phase-out ranges for itemized deductions, personal exemptions, the AMT exemption, IRAs, and several credits, were increased slightly for inflation.

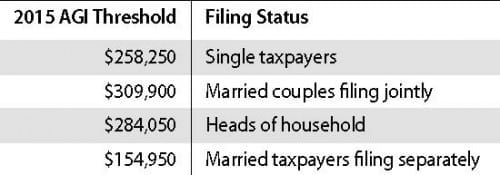

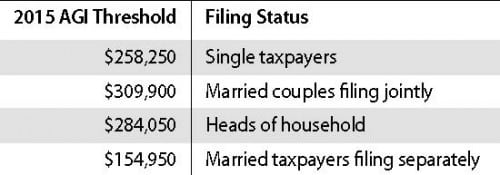

The personal exemption and itemized deduction phase-out threshold for married filing jointly is now an adjusted gross income of $309,900. For single filers, it is $258,250.

The itemized-deduction phase-out reduces otherwise-allowable itemized deductions by 3% of the itemized deductions exceeding the threshold amount. The reduction cannot reduce itemized deductions below 80% of the otherwise deductible amount.

Certain itemized deductions are not subject to the phase-out — medical expenses, investment-interest expense, casualty and theft losses, and gambling losses.

Business mileage increased Jan. 14 to 57.5 cents a mile, while the deduction for medical or moving mileage dropped by a half-cent to 23 cents. The deduction for charitable mileage remains unchanged at 14 cents.

The new limits for some of the major items are outlined in the accompanying table.

Timing of Deductions

As the standard deduction continues to increase each year, fewer and fewer taxpayers are finding that they can itemize deductions.

Statistically, only about one-third of all taxpayers use Schedule A, Itemized Deductions. In addition to the inflation factor, some other influences make itemizing a less attractive option.

First is the increase in the threshold for deducting medical expenses. This threshold had remained at 7.5% of adjusted gross income for a number of years. However, for most taxpayers, the threshold has increased to 10% under the Affordable Care Act.

Another factor affecting itemizing is the decrease in interest rates. As interest rates have declined, so has the amount of interest taxpayers are paying. As a result, the mortgage-interest deduction has declined. Many taxpayers are now finding they no longer have enough deductions to itemize.

When taxpayers find themselves in a situation where they are close to the itemization threshold, they can often decrease their tax liability through the timing of their deductions. This strategy simply involves speeding up or delaying certain deductions, bunching them as much as possible in a particular year.

For example, in a year in which the taxpayer has enough medical expenses to deduct, a good strategy is to pay as many of these bills as possible in that year to take advantage of greater medical deductions.

Another area open to the timing of the deduction is charitable contributions. By delaying or speeding up such contributions, taxpayers can bunch them into one year for maximum benefit. While regarding charitable giving, do not overlook the tax benefit to be derived from non-cash charitable contributions.

Depending on the local property tax laws, it may be possible to pay two years of property tax bills in one calendar year to get maximum benefit from the deduction. However, be aware of early-payment discounts and late-payment penalties that would wipe out the benefits from taking the itemized deduction.

Another related strategy is to consider if you are in the itemized-deduction phase-out area for the current year. If you have an unusually large amount of income in the current year, it may be beneficial to maximize itemized deductions in the following year, when you are not subject to the phase-out.

Keep in mind that the items in question can be deducted only in the year in which they are considered paid. You cannot choose which year to deduct the item if it has been paid.

Bills paid with a credit card can be deducted in the year in which the credit card is charged, not when the amount is paid to the credit-card company. If the provider of the goods or services has been paid, you may take the amount as an itemized deduction.

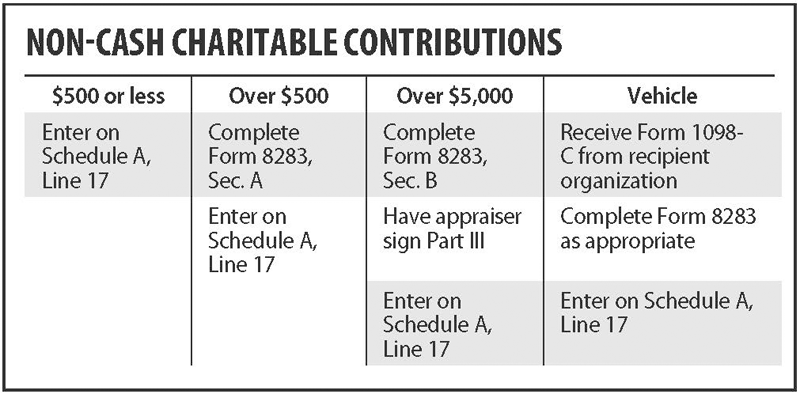

Non-cash Contributions Can Be Money in Your Pocket

We live in a throwaway society. We buy something, use it, and then discard it when it no longer suits our needs.

Frequently, these items are in good condition and can be useful to others. Making a contribution of these items to a qualified tax-exempt charitable organization is a win-win-win situation. The organization benefits from the revenues generated by the contribution, the donor gets a tax deduction, and someone gets a usable item at a good price.

The accompanying table illustrates the process of deducting the contribution on Form 1040. It is a fairly simple reporting model, with increasing requirements as the dollar value of the contribution increases.

If the contribution exceeds $5,000 in value, an appraisal must be obtained. The cost of this appraisal is deductible as a miscellaneous itemized deduction subject to the 2% limitation. The appraisal requirement does not apply to registered securities.

If the donated item is a vehicle, boat, or airplane, the recipient organization is required to issue the donor a Form 1098-C, and the deduction amount will be the proceeds the organization received from the sale of the vehicle or the Blue Book value if it was retained for use in the organization.

Securities and certain other capital assets that have been held for more than 12 months can be donated, and the donor can take a deduction for the fair market value of the asset instead of the donor’s basis. This can yield a large deduction at little cost for assets that have significantly increased in value.

When donating household items, many people have a tendency to stuff their goods into a large garbage bag and tell the tax preparer that they donated “three bags of clothing and household goods, and here’s my receipt from the organization.” This haphazard approach will not stand up to an IRS audit. The taxpayer is required to have an itemized list of the items donated.

Valuing the items that are donated can be a problem and somewhat time-consuming. But a little time can pay significant rewards. Both the Salvation Army and Goodwill publish a valuation guide for donated items, which may be downloaded for free from their respective websites.

Another approach is to use computer programs. Intuit offers It’s Deductible, which is free online at www.itsdeductible.com.

There is also a mobile app for Apple. You simply input information about the charity, proceed to list your donated items, and let the program value them for you. The IRS generally accepts the values assigned by these guides or programs.

Using one of the above methods, a simple spreadsheet or some other system will help keep your donation records up to date and simplify your document gathering at tax time. An organized list may mean a larger deduction for you.

Capital-gain Rates and Net Investment Income Tax

If someone were to ask, “what is the capital-gain tax rate?” the best answer would have to be: “it depends.”

First, you should determine whether the sale is subject to taxation at the ordinary income rate or at the preferred capital-gain rate. A capital asset must be held for more than 12 months to qualify for capital-gain treatment. Otherwise, it is taxed at ordinary income rates, which vary from 10% to 39.6%.

Even if the sale of the asset meets the criteria for capital-gain treatment, the rate can be zero, 15%, 20%, 25%, or 28%. Then there may be an additional 3.8% net investment income tax levied on top of those rates.

It should be noted that the capital-gain rate is a rate that substitutes for the ordinary income rate. The sale is not subject to both regular income tax and the capital-gain tax.

Generally, a capital gain arises from the sale of investment property or real estate. In addition to gains from the sale of capital assets being subject to the capital-gain rate, qualified dividends are taxed at that rate but are not capital gains. The highest capital-gain rate is 28%, levied on gains from the sale of collectibles or qualified small-business stock. Next would be the tax on unrecaptured Section 1250 gains at 25%.

This brings us to the more common capital-gain rates, which are applied to most capital asset sales. This rate varies.

Taxpayers in the 39.6% (highest) bracket will be subject to a 20% capital-gain rate. Those not in the highest bracket but in the 25% or higher bracket must pay at the 15% rate. Taxpayers in the 10% or 15% brackets have a zero capital-gain rate applied.

These rates can be somewhat misleading since some taxpayers will be subject to the 3.8% net investment income tax. This is a surtax on taxpayers whose modified adjusted gross income exceeds $250,000 for married couples filing jointly ($125,000 for married filing single and $200,000 for everyone else).

Estates and trusts are subject to this tax, which can be significant. They will be subject to this tax on the lesser of:

• Undistributed net investment income; or

• Adjusted gross income over the amount at which the highest tax bracket for a trust or an estate begins (currently $12,300).

This tax makes the effective capital gain rate as high as 23.8%.

However, estates and trusts can avoid the tax by making income distributions to the beneficiaries. Since the threshold subject to the tax is significantly higher for individuals, this option could eliminate the tax altogether.

The net investment income tax is levied on income in addition to capital gains. Net investment income includes most dividends, interest, annuities, royalties, rents, and the taxable portion of gains from the sale of property. The regulations defining net investment income take 159 pages to define the term, so consult with your CPA regarding your liability for this tax.

A separate tax was enacted as a part of the Affordable Care Act that also applies to individuals with high incomes. The 0.9% additional Medicare tax is levied on earned income in excess of certain threshold amounts. The thresholds are the same as the ones for the net investment income tax.

However, collecting the tax is somewhat complex. If an individual has wages in excess of $200,000, the employer is required to withhold the tax on earnings in excess of that amount. If neither spouse exceeds the $200,000 threshold but they have a combined earned income in excess of $250,000, they must pay the tax when they file their Form 1040.

As with the additional Medicare tax, taxpayers are advised to consult with their CPA to take steps to mitigate this tax — or at least to be prepared for it.

Home-office Safe Harbor

If your business operates out of your home, the IRS will allow you to take a tax deduction for your home office.

To qualify for the deduction, you are required to:

• Have an area in your home that is exclusively and regularly used as a home office; and

• Use the home as your principal place of business.

If you are an employee, you are subject to these same two criteria. In addition, your home office must be for the convenience of the employer. An employee cannot rent a portion of the home to the employer, use the rented portion to perform services as an employee for that employer, and take a home-office deduction.

The home-office deduction is based on the portion of the home that is used for business. A percentage of many home expenditures can be allocated to the cost of the office. In addition, a depreciation deduction may be included in the cost.

The IRS now offers a simplified safe-harbor option for deducting home-office expenses. Rather than determining the actual expenses incurred in the home, taxpayers may simply deduct $5 per square foot used as an office for the deduction. Keep in mind that using the safe-harbor method means there will be no depreciation recapture when the home is sold.

A taxpayer may choose either deduction method each year. The election is made by filing the return using the method of choice for that year.

Home-office Deduction for a Corporation

The home-office deduction is designed for a sole proprietorship filing a Schedule C. Business owners who choose to incorporate their businesses will lose the advantage of deducting the expenses of a home office because the corporation and the taxpayer become two separate, distinct entities at the time of incorporation.

Three alternatives can be chosen that would allow a home-office deduction in these situations. First, assuming that corporation owners are also employees of their corporations, they could take the employee home-office deduction on their Schedule A as a miscellaneous itemized deduction.

However, this approach has two disadvantages. First, the deduction is subject to the 2% limitation on miscellaneous itemized deductions, potentially eliminating some or all of the deduction. Secondly, taxpayers who do not itemize cannot obtain a home-office deduction.

The second choice is for corporations to pay rent to their owners for use of a home office. This rent is deductible by the corporations, and the owners must report the rent on their Form 1040, Schedule E.

However, an owner can set the amount of rent equal to the expenses associated with the home office and show no gain or loss on the rental activity on the Form 1040. Using this method, the owner can create some personal cash flow since deducting depreciation on the office is an allowable expense.

The third alternative is to have the corporation pay the owner for any out-of-pocket costs of a home office under an accountable plan. Reimbursed expenses must be actual job-related expenses that the owner must substantiate by providing the corporation with receipts or other documentation.

These expenses can include a portion of mortgage interest, property taxes, utilities, insurance, security service, and repairs. They would be reimbursed based on the percentage of the home that is represented by the office area.

These last two methods require some rigorous record keeping. But the bottom line is that either of these approaches can yield benefits to the taxpayer and the corporation.

Tangible Property Regulations

New tangible property regulations went into effect on Jan. 1, 2014. These regulations are far-reaching and designed to guide taxpayers in determining whether an expenditure can be classified as an expense or must be capitalized and depreciated.

In many cases, the answer is clear. Routine ‘ordinary and necessary’ business expenses are normally expensed. These include supplies, payroll, purchased inventory (when sold), small tools, insurance, licenses and fees, and routine maintenance.

At the other extreme are items that are clearly long-lived assets and must be capitalized and depreciated — vehicles, machinery and equipment, buildings, etc. Companies may use a de minimis safe-harbor election to simplify accounting records. This amount is $5,000 if the company has an applicable financial statement (AFS), and $500 otherwise. Expenditures below these amounts may be expensed. An AFS is generally an audited statement filed with the SEC or with a government agency.

Where the major issues come into play is in considering whether a repair can be classified as an improvement to the asset. Under IRS regulations, property is improved if it undergoes a betterment, an adaptation, or a restoration. If it is an improvement, it should be depreciated.

Betterment:

• Fixes a ‘material condition or defect’ in the property that existed before acquisition of the asset;

• Results in a material addition to the property; or

• Results in a material increase in the property’s capacity.

Restoration:

• Returns a property to its normal, efficient operating condition after falling into disrepair;

• Rebuilds the property to like-new condition after the end of its economic life;

• Replaces a major component or substantial structural part of the property;

• Replaces a component of the property for which the owner has taken a loss; or

• Repairs damage to the property for which the owner has taken a basis adjustment for a casualty loss.

Adaptation:

• Fits a unit of property to a new or different use.

The definition of the unit of property (UOP) is critical. It helps determine whether an expenditure should be capitalized or expensed.

For example, a building may be defined as a UOP, or each of the enumerated building systems may be defined as a UOP. For non-buildings, the UOP is defined by the IRS as all components that are functionally interdependent, unless the taxpayer used a different depreciation method or recovery period for a component at the time it was placed into service.

There are two additional safe harbors — an election for small taxpayers and a routine-maintenance safe harbor.

Conclusion

Tax laws change at an amazing pace. It is estimated that more than 5,000 changes to federal tax laws have been made since 2001. That’s an average of more than one change per day. The Internal Revenue Code was 73,954 pages in 2013, which makes War and Peace look like a short story.

The information contained in this article was current at the time it was published. However, it is by no means certain that it will remain current for the rest of 2015.

Why bring this up? Simply to emphasize how incredibly complex our tax laws have become. Tax planning is necessary in today’s complex world so that you can stay on the right side of the IRS and minimize your tax liability.

James Barrett is managing partner of Meyers Brothers Kalicka in Holyoke; (413) 536-8510; [email protected]

“If you are one of those businesses who started selling direct to consumers on your website or if you turned a previous hobby into a business venture that markets using an online marketplace that does not collect sales tax for you, you might have a significant tax exposure you’re not even aware of.”

“If you are one of those businesses who started selling direct to consumers on your website or if you turned a previous hobby into a business venture that markets using an online marketplace that does not collect sales tax for you, you might have a significant tax exposure you’re not even aware of.” “Under the Biden administration’s proposal, transfers of appreciated property upon death, or by gift, may result in the realization of capital gain to the donor or decedent at the time of the transfer. This means tax may be triggered at the date of the transfer regardless of whether the property is subsequently sold.”

“Under the Biden administration’s proposal, transfers of appreciated property upon death, or by gift, may result in the realization of capital gain to the donor or decedent at the time of the transfer. This means tax may be triggered at the date of the transfer regardless of whether the property is subsequently sold.”

It’s called the Setting Every Community Up for Retirement Enhancement Act, and it was signed into law just a few weeks ago and took effect on Jan. 1. It is making an impact on taxpayers already, and individuals should know and understand its many provisions.

It’s called the Setting Every Community Up for Retirement Enhancement Act, and it was signed into law just a few weeks ago and took effect on Jan. 1. It is making an impact on taxpayers already, and individuals should know and understand its many provisions.

Year-end tax planning in 2019 remains as complicated as ever. Notably, we are still coping with the massive changes included in the biggest tax law in decades — the Tax Cuts and Jobs Act (TCJA) of 2017 — and pinpointing the optimal strategies. This monumental tax legislation includes myriad provisions affecting a wide range of individual and business taxpayers.

Year-end tax planning in 2019 remains as complicated as ever. Notably, we are still coping with the massive changes included in the biggest tax law in decades — the Tax Cuts and Jobs Act (TCJA) of 2017 — and pinpointing the optimal strategies. This monumental tax legislation includes myriad provisions affecting a wide range of individual and business taxpayers.

Section 199A of the Tax Cuts and Jobs Act was created to level the playing field when it comes to lowering the corporate tax rate for those businesses not acting as C corporations. For most profit-seeking ventures, qualifying for the deduction is not difficult, but for rental real estate, it becomes more difficult.

Section 199A of the Tax Cuts and Jobs Act was created to level the playing field when it comes to lowering the corporate tax rate for those businesses not acting as C corporations. For most profit-seeking ventures, qualifying for the deduction is not difficult, but for rental real estate, it becomes more difficult.

There are many changes that businesses and individuals should be aware of under The Tax Cuts and Jobs Act (TCJA), the most significant tax legislation in the U.S. in more than 30 years. Here are the 10 changes that will have the most significant impact this tax season.

There are many changes that businesses and individuals should be aware of under The Tax Cuts and Jobs Act (TCJA), the most significant tax legislation in the U.S. in more than 30 years. Here are the 10 changes that will have the most significant impact this tax season.

The Tax Cuts and Jobs Act represents a seismic shift within the broad realm of accounting and tax planning, and some of the aftershocks may not be felt, and fully understood, for some time. But some things are known, and individuals and businesses should understand their implications.

The Tax Cuts and Jobs Act represents a seismic shift within the broad realm of accounting and tax planning, and some of the aftershocks may not be felt, and fully understood, for some time. But some things are known, and individuals and businesses should understand their implications.

In 2018, nonprofit organizations face implementation of the first major overhaul of accounting standards in two decades. The goal of the overhaul is to improve the communication of financial results for donors and other outside stakeholders and to emphasize transparency in financial reporting.

In 2018, nonprofit organizations face implementation of the first major overhaul of accounting standards in two decades. The goal of the overhaul is to improve the communication of financial results for donors and other outside stakeholders and to emphasize transparency in financial reporting.

Since its introduction more than 30 years ago, the data-driven process-improvement methodology known as Six Sigma has been most closely associated with the manufacturing sector. But, as recent initiatives undertaken by the accounting firm

Since its introduction more than 30 years ago, the data-driven process-improvement methodology known as Six Sigma has been most closely associated with the manufacturing sector. But, as recent initiatives undertaken by the accounting firm

Tax planning can be a guessing game, especially in a year when new leadership in Washington could make significant changes to the tax code. But there are a number of basic strategies that businesses and individuals may put in play as year end approaches.

Tax planning can be a guessing game, especially in a year when new leadership in Washington could make significant changes to the tax code. But there are a number of basic strategies that businesses and individuals may put in play as year end approaches.

The rise of Uber and similar transportation services like Lyft have been a boon for people looking to make some extra money on their own schedule. But they have also given rise to a number of taxation issues. For anyone looking to turn their personal vehicle into a part-time taxi service, here’s a handy guide to IRS rules for tax filing, expense deductions, and more.

The rise of Uber and similar transportation services like Lyft have been a boon for people looking to make some extra money on their own schedule. But they have also given rise to a number of taxation issues. For anyone looking to turn their personal vehicle into a part-time taxi service, here’s a handy guide to IRS rules for tax filing, expense deductions, and more.

It’s obvious that taxpayers across the spectrum are affected by these tax provisions. The delayed action on the part of Congress has left taxpayers with questions about how to proceed.

It’s obvious that taxpayers across the spectrum are affected by these tax provisions. The delayed action on the part of Congress has left taxpayers with questions about how to proceed. Also deductible are unreimbursed employee business expenses, tax-return-preparation fees, investment expenses, and certain other miscellaneous itemized deductions that together are in excess of 2% of AGI

Also deductible are unreimbursed employee business expenses, tax-return-preparation fees, investment expenses, and certain other miscellaneous itemized deductions that together are in excess of 2% of AGI