It’s Important to Understand Your Alternatives

By Eric Aasheim

Moving from home to a senior-living community is one of the most consequential decisions elder loved ones may be faced with in their lifetimes.

The move is usually permanent; is unfortunately often made in crisis mode or under duress, and involves a host of emotional and psychological implications around declining physical capabilities, perceived loss of independence, and financial worry.

“Moving from home to a senior-living community is one of the most consequential decisions elder loved ones may be faced with in their lifetimes.”

“Moving from home to a senior-living community is one of the most consequential decisions elder loved ones may be faced with in their lifetimes.”

Knowing the answers to these commonly asked questions will help seniors and their adult children plan ahead and ultimately put themselves in a position to make thoughtful and informed decisions about the most appropriate living and care options for their needs.

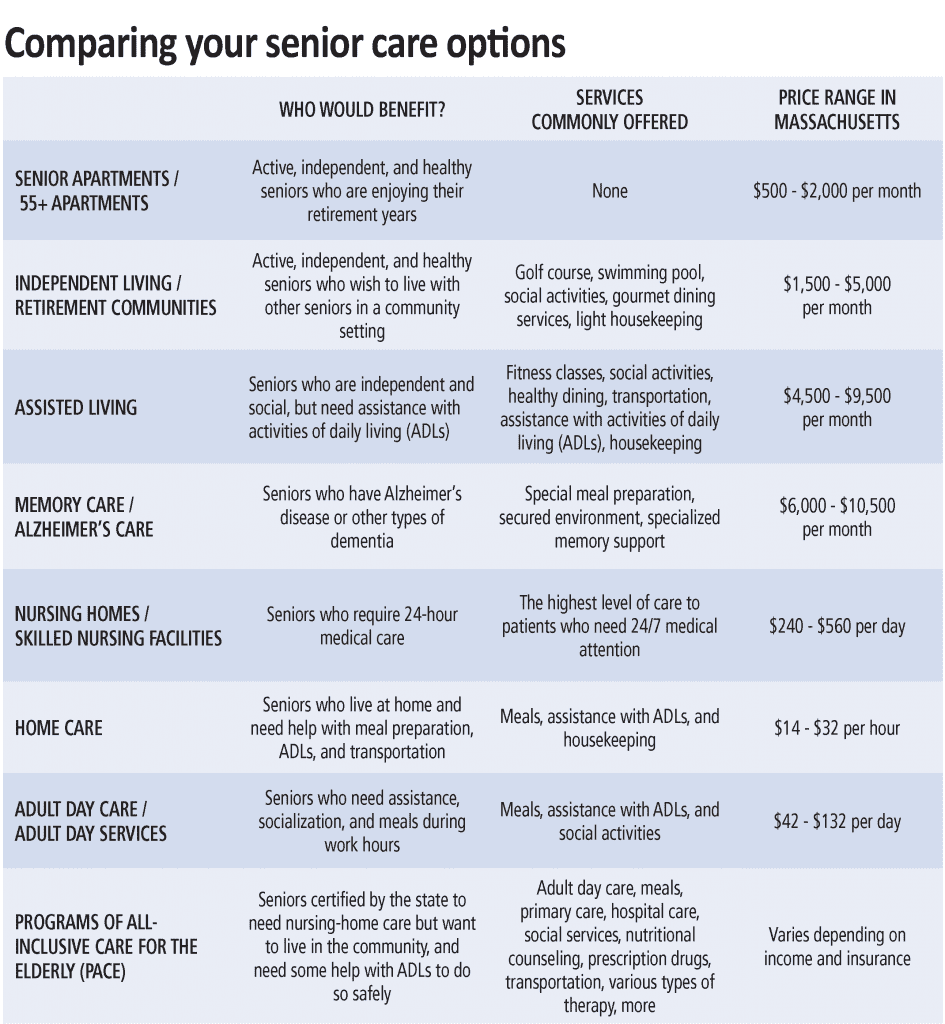

What is the difference between independent living, assisted living, memory care, and skilled nursing?

Independent living (IL) is intended for seniors who do not need assistance or supervision with independent activities of daily living (IADLs) like showering, dressing, toileting, eating, or transferring (mobility, bed to standing, sitting to standing, etc.).

Most IL communities provide apartments with full kitchens, and the monthly fee includes one main meal per day in the dining room. Independent living in Western Mass. ranges from $2,000 to $5,000 per month.

Assisted living (AL) communities are appropriate for seniors who require some level of assistance with two or more IADLs and help with medication management; apartments are typically equipped with a kitchenette only because the monthly fee includes three restaurant-style meals per day. Assisted living in Western Mass. ranges from $4,000 to $9,000 per month.

Memory care (MC) is intended for individuals who have dementia, Alzheimer’s, or other neurogenerative diseases and require an intensive or specialized program of care and supervision. Memory-care communities are secure settings with passcode entrances and enclosed outdoor spaces to keep residents on site, and can be stand-alone facilities or a separate wing or ‘neighborhood’ within a traditional assisted-living community. Memory-care communities most often provide private studio or shared companion suites for their residents. Memory care in Western Mass. ranges from $3,500 (companion suites) to $11,000 per month.

Skilled-nursing facilities (SNFs) are licensed healthcare residences for individuals who require a higher level of medical care than can be provided in an AL setting. Skilled-nursing staffs consisting of RNs, LPNs and CNAs (certified nursing assistants) provide 24-hour medical attention for their long-term and short-term rehabilitation residents. While private rooms are available in many SNFs, shared living arrangements with two or three residents to a hospital-style room are much more common. Skilled-nursing facilities in Western Mass. range from $250 to more than $500 per day.

Can I receive care at home rather than moving to a senior-living community?

Absolutely. There are any number of quality home-care companies that can provide a wide range of custodial and healthcare services in the comfort of your own home. Home care is often referred to as non-skilled care (grooming, dressing, bathing, cleaning, and other everyday tasks) and home health care as skilled care (skilled nursing and therapy).

Seniors who are largely independent but can benefit from limited home care or home-healthcare services may choose to continue living in their homes as long as these services help them do so safely. Unless you hire a full-time live-in, skilled and non-skilled care are typically provided for only a few hours per day a few days per week, meaning family members often are called upon to supplement the home-care schedule on their own.

Seniors who are at risk for (or have experienced) frequent falls or who require consistent overnight supervision or assistance may find that moving to an assisted-living community provides them with a more secure living environment.

The choice between home care and senior living is highly personal and almost always comes down to a question of safety, location, the desire and need for socialization, and finances.

What is a continuing-care retirement community (CCRC), and what are the benefits compared to other senior-living communities?

Continuing-care retirement communities (CCRCs) are senior-living communities that offer a complete continuum of care (IL, AL, MC, and SNF), usually on a single campus. The primary benefit of a CCRC is that you can stay in the same community and never have to move, even as your care requirements change as you age. CCRCs (also referred to as life-plan communities) do typically require a substantial up-front community fee that can range from $10,000 to $300,000 or more depending on the community, the structure of the life-care plan, and the size and type of apartment.

Many CCRCs offer declining, refundable options that can return 70% to 90% of the up-front community fee to the resident when he or she moves, or to her estate when the resident passes away. CCRCs do still charge monthly fees, but they are often lower and increase less from one level of care to the next than traditional senior-living communities. CCRCs also offer a potential tax-deduction benefit that many non-CCRCs do not provide.

Will my health insurance cover the cost of assisted living or memory care? What if I am eligible for Medicaid?

Medicare and private insurance plans do not cover the cost of assisted living or memory care. Medicare will cover short-term and intermittent home care or rehabilitation stays in a SNF following hospitalization, but will not pay for either long-term. Seniors generally must pay for assisted living, memory care, and home care privately unless they have long-term-care insurance with benefits specifically designed to cover these services.

Qualifying veterans and their spouses may be eligible for the aid and attendance benefit from the VA to help pay for the cost of assisted living, memory care, home care, and skilled-nursing facilities.

Some, but not most, assisted-living and memory-care communities do participate in programs administered by Medicare and Medicaid that are designed for low-income seniors who could otherwise not afford senior-living communities.

Medicaid does cover the cost of long-term care in Medicaid-certified skilled-nursing facilities and home healthcare services for recipients who would qualify for nursing-home care.

What other senior-living and care options are there?

• Residential care facilities (also called rest homes) provide meals, housing, supervision, and care for seniors who need assistance with activities of daily living but don’t yet require skilled nursing care.

• Congregate housing is a shared-living environment that combines housing, meals, and other services for seniors but does not provide 24-hour care or supervision. Public congregate housing is administered by municipal housing authorities and is partially subsidized by the state and federal government.

• Adult foster care is an alternative to residential care and matches seniors who can no longer live on their own with individuals or families who provide room, board, and personal care in their homes.

• Respite care is short-term care and supervision provided for seniors at home or in assisted-living or skilled-nursing facilities to provide family members who need some time off from their caregiver duties.

• Adult day health programs (also called adult day care) provide a wide array of community-based services for seniors during the day (skilled nursing, supervision, direct care, nutrition and dietary services, and therapeutic, social, and recreational activities) so that family members can work or attend to other responsibilities.

• Hospice care is available for individuals with life-threatening illnesses or a life expectancy of six months or less and can be provided in the home, in assisted-living or skilled-nursing facilities, in the hospital, or in specialized hospice facilities. When curative treatment is no longer an option, hospice professionals work to make a patient’s life as dignified and comfortable as possible and provide critical emotional and spiritual support services to the patient and family members.

How have senior-living and care options been impacted by COVID-19?

In short, the impact has been profound, and the ‘new normal’ is taking shape as we speak. Most home-care providers and senior-living communities have resumed services to current and new clients at some level. However, the provision of these services is governed by strict protocols to protect the health and safety of residents, staff, and family members.

For instance, many assisted-living communities are not currently offering in-person tours and assessments and instead facilitating these interactions virtually. Since most senior-living communities are observing social-distancing guidelines, new residents must quarantine for 14 days after move-in, and residents are dining in their apartments rather than in the community dining room. Social activities and outings have largely been modified or canceled, and visits from family members have been curtailed for the time being.

Eric Aasheim is a certified senior advisor and owner of Oasis Senior Living of Western Massachusetts. He assists seniors and family members through the entire process of transitioning from home to senior-living communities in Hampden, Hampshire, and Berkshire counties and surrounding areas.

“Someone develops Alzheimer’s disease every 68 seconds, with 5 million Americans affected, and the number expected to increase to 20 million by 2050.”

“Someone develops Alzheimer’s disease every 68 seconds, with 5 million Americans affected, and the number expected to increase to 20 million by 2050.” “Stacks of unopened mail, late-payment notices, unfilled prescriptions, and the lack of general upkeep of the house can all be signs that your loved one may need someone to assist with bill paying or homemaking.”

“Stacks of unopened mail, late-payment notices, unfilled prescriptions, and the lack of general upkeep of the house can all be signs that your loved one may need someone to assist with bill paying or homemaking.” “The goal is to support clients who prefer to remain at home, but need care that cannot easily or effectively be provided by family or friends.”

“The goal is to support clients who prefer to remain at home, but need care that cannot easily or effectively be provided by family or friends.”