A Hunger to Do More

The Food Bank of Western Massachusetts Dramatically Grows Its Operations

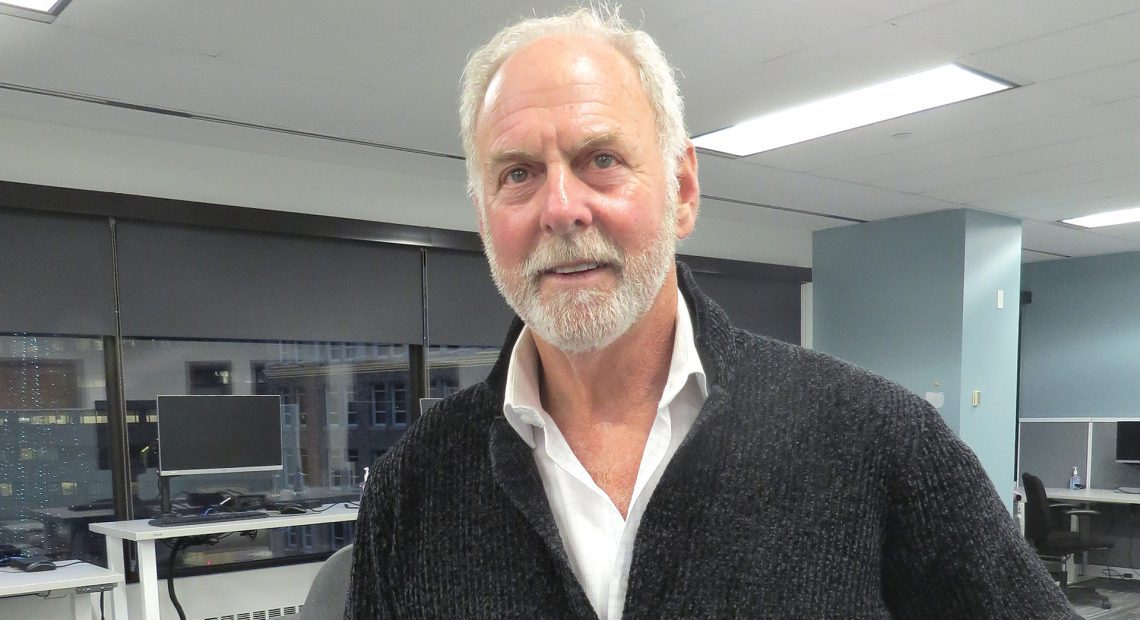

Executive Director Andrew Morehouse

It’s long been a tenet among nonprofits — successful ones, anyway — that they need to think entrepreneurally in order to thrive and grow. To think, in other words, like successful for-profit businesses do, in terms of resource allocation, financial planning, workforce management, and day-to-day operations.

And no nonprofit has been more entrepreneurial — and more ambitious — over the past few years than the Food Bank of Western Massachusetts, whose $30 million project to build a new, larger headquarters in Chicopee culminated not only in last month’s grand-opening ceremony, but in the dramatic expansion of its capacity to perform work it was already doing on a massive scale.

The project — and the accompanying campaign that raised about $15 million of that cost from private donors and $15 million from state and federal governments — started just before the pandemic and continued through those challenging years, making the successful conclusion especially gratifying to Executive Director Andrew Morehouse and his team, and earning the Food Bank recognition from BusinessWest as its Top Entrepreneur for 2023.

“The Food Bank of Western Massachusetts’ new, state-of-the-art facility will allow their dedicated team to provide greater access to healthy, nutritious foods to thousands more of our neighbors in need and expand service routes to partners throughout the area.”

“We have to be innovative. We have to be able to adapt to circumstances,” he said. “We have a strategic plan, and every year, we have specific objectives — and all that can go out the window if something happens, like a pandemic, and then we have to pivot.”

That applies to any entity — for-profit or nonprofit — of this size, Morehouse added, noting that the Food Bank has a $9 million annual operating budget, and the value of the food that comes through is about $18 million, so this is essentially a $27 million operation, with a staff of 67, and plans to hire another 14 by the end of 2024.

Andrew Morehouse addresses guests at the Food Bank’s grand-opening ceremony last month.

“We acknowledge that it’s the dedication and talent of our staff that’s the source of our success,” he told BusinessWest. “That’s our ethos as a business — that we can succeed in our mission when we acknowledge and invest in our staff and the hard work that they’re doing.”

The new food-distribution center, located at 25 Carew St. in Chicopee, is twice the size of its previous Hatfield location, with an additional 18,000 square feet in the warehouse alone. Floor-to-ceiling warehouse racks and expanded refrigeration and freezer sections enhance efficiencies and enable the Food Bank to store and quickly distribute more healthy food than ever before to 175 member food pantries, meal sites, and emergency shelters across all four counties of Western Mass.

The new site also features a dedicated community space with a working kitchen for cooking and nutrition classes and other educational events. Other efficiencies include electric charging stations, an expanded member pick-up area, and plenty of parking for staff and volunteers. In 2024, the Food Bank will add a solar array on the roof and a canopy over part of its parking, along with backup battery storage that will fully support all electricity needs of the building.

“That will make it a greener building, so there are efficiencies to be gained,” Morehouse said. “We expect that building to be near-carbon-neutral and generate most of the electricity that we need.”

The investment in the relocation project and its capital campaign is already bringing palpable returns. In just the first three months since moving in, the Food Bank has already provided 25% more healthy food than the same period last year — the equivalent of more than a half-million meals. In all, the Food Bank provides a little more than 1 million pounds of food every month, or the equivalent of 850,000 meals.

“The more we thought about moving to Hampden County, the more we realized that was what we needed to do.”

“The Food Bank of Western Massachusetts’ new, state-of-the-art facility will allow their dedicated team to provide greater access to healthy, nutritious foods to thousands more of our neighbors in need and expand service routes to partners throughout the area,” U.S. Rep. Jim McGovern said at the grand opening. “I’m proud of the Food Bank’s 40 years of history serving our community and their continued leadership on the national stage in our movement to end hunger now.”

An Overstuffed Facility

The Food Bank, which traces its history back to 1981, expanded its facility in Hatfield just before the Great Recession, and then maxed it out as food-insecurity needs exploded during the ensuing years of difficult economic conditions.

“We had no available space, and we continued to see heightened demand, and that left no space at all for continued growth,” Morehouse said, noting that the Food Bank has grown its operations by about 6% annually between 2006 and last year.

The new Chicopee headquarters doubles the size of the former Hatfield site.

“We knew around 2016 that it was unsustainable, that we would need a larger space in order to continue to accommodate more food and to address increasing food insecurity whenever there was another adverse impact on the economy, whether it be a recession or … who would have known?”

Who, indeed. When COVID struck, the Food Bank had already been scoping out properties — and considering numerous options, such as a two-location model that was rejected because of its expense. But soon after, in 2020, the nonprofit found its ideal spot in Chicopee, launched the capital campaign in 2021, and started building in 2022.

The site had a couple of advantages, one being its proximity to two interstate highways, another being the county’s population and demographic makeup, Morehouse explained.

“The more we thought about moving to Hampden County, the more we realized that was what we needed to do — not only because of the proximity to the largest concentration of people who are faced with insecurity, but also because, quite frankly, it would enable us to strengthen our relationships with communities of color, which, unfortunately, face food insecurity disproportionately relative to the rest of society.”

As for the campaign, it drew the support of 246 individuals, businesses, and foundations — but there was some anxiety early on, especially since it was launching during a challenging economic time, year two of the pandemic.

“If we don’t acknowledge that the problem exists and we don’t, as a society, want to do something about it, we’re not going to make any progress.”

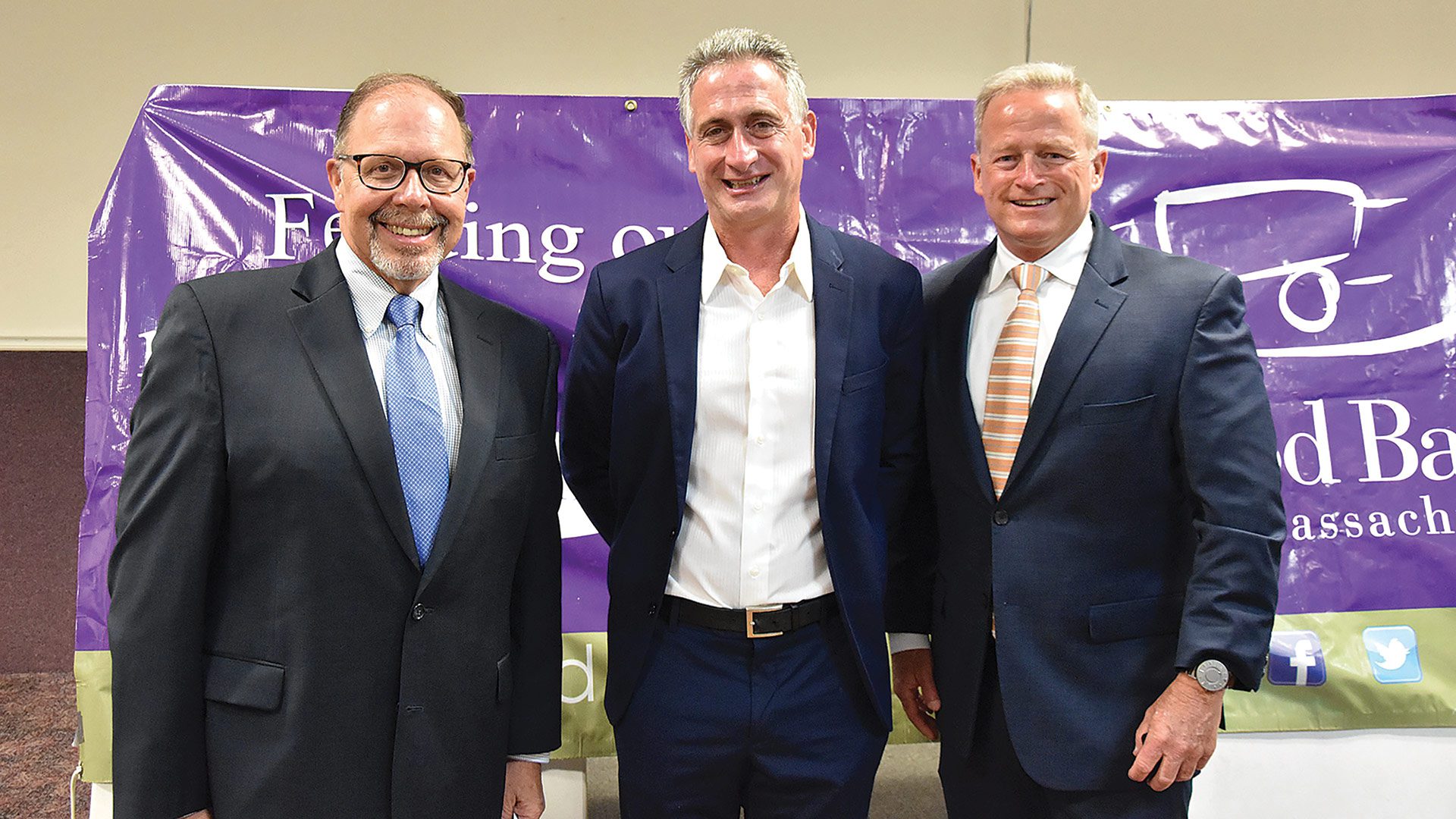

Morehouse credited the early, significant support by Big Y and MassMutual in “grounding” the campaign and lending confidence that it could succeed. After that, the entire banking community stepped in, as did and a host of other businesses, foundations, and individuals, including major contributions from the Irene E. and George A. Davis Foundation and C&S Wholesale Grocers.

“Before we had launched the campaign, there was a lot of internal discussion and planning, and I just had the faith that we could accomplish it and that the community would rally behind us, and they did,” he said. “Our board felt the same way, so we went public after we secured some of those large commitments. So we had something to start with, and then we were able to inspire and persuade the rest of the community to jump on board, and they did.”

One factor, he noted, was that the pandemic focused more attention nationally on the issue of food insecurity across the country — attention that was needed even before COVID, but was definitely in the public eye now.

Andrew Morehouse (center) with Big Y President and CEO Charlie D’Amour (left) and Dennis Duquette, MassMutual Foundation president, when they announced large pledges to the Food Bank’s capital campaign in 2021.

“If we don’t acknowledge that the problem exists and we don’t, as a society, want to do something about it, we’re not going to make any progress,” he said. “So it was gratifying that the community rallied behind our campaign to help us to be successful. And now we have this facility, this community resource, that can make even greater impact in addressing food insecurity, but also to serve as a place for convening, for learning, for collaborating, for taking action.”

The ‘action’ part of that goal is clearly the most important.

“If we’re ever going to end hunger, we need to raise awareness, and that happens through education and dialogue, but also through the power of public policy and the changes that we can make to public policy and investments in people, families, and communities to ensure that everyone can lead a healthy and productive life,” Morehouse said.

“That means addressing not only the food assistance that people need today, but the underlying causes of hunger,” he went on. “Do people have access to affordable housing, childcare, transportation, education, jobs that pay a meaningful wage to support families? All of those are things we need to be looking at as a society.”

After 19 years in charge of the Food Bank, it’s a lesson that has grown clearer every year. “I’ve been in the nonprofit world for over 30 years,” he said, “and I’ve always enjoyed building things, building capacity, because that’s how, ultimately, I think you create social change and economic change for the better, for families and communities.”

In and Out

The Food Bank’s reach is impressive, serving as a clearinghouse of emergency food for the region, most distributed to local food pantries, meal sites, and shelters.

Much of the food the organization collects is purchased, using state and federal funds, from wholesalers, local supermarkets, and dozens of local farms; farmers also donate more than a half-million pounds of food each year.

“We then turn that food around — we store it here and distribute it through a vast network of about 175 food pantries, meal sites, and shelters across all four counties of Western Massachusetts,” Morehouse explained. “That’s how about 85% of the food that we receive flows through, ultimately to individuals in need of food assistance.”

In addition, the Food Bank operates a mobile food bank for direct-to-household distribution at 26 sites once or twice a month, plus a brown-bag program for elders that boasts 52 partners, mainly senior centers. The nonprofit also receives reimbursements to provide some individuals with supermarket gift cards, in addition to referring them to food-pantry meal sites.

And because food insecurity is often entangled with other economic and social needs, “we do refer individuals to some other nonprofit partners who can provide them with affordable-housing assistance, transportation, childcare, job training, things of that sort,” Morehouse added, noting that the Food Bank uses the 413Cares system to coordinate referrals with partners. “We’re all trying to figure it out and find a way to help people lead healthy, productive lives.”

Some of the Food Bank’s top supporters recognize the importance of those efforts.

“Our goal, our mission, is to feed families,” outgoing Big Y President and CEO Charlie D’Amour (see story on page 4) said when announcing financial support for the Food Bank early in the campaign. “We have people in our communities that are really struggling to get food on their table. The role of food banks serving local neighborhoods has never been more important.”

Country Bank President Paul Scully felt the same when announcing a large donation in 2021. “With everything we’re hearing these days about the shortage of food and the high expense of food … the need is real out there,” he said. “As a community partner, we care deeply about the sustainability of our communities and the people who live in them.”

What they were acknowledging was a nonprofit that has been entrepreneurial in its efforts to tackle a widening problem.

“We’re very much like a for-profit business to the extent that we have overhead, we have trucks, we have inventory, and we have staff,” Morehouse said, noting that the Food Bank doesn’t have customers, exactly, but it does have key stakeholders, from the households facing insecurity to the meal sites and shelters that receive 85% of those distributions, to the federal and state agencies that pay for the food. “We have an obligation to those agencies to ensure that we’re delivering on our agreement with them.”

In addition, the Food Bank maintains contracts with the Department of Transitional Assistance to provide SNAP assistance and with MassHealth to provide food assistance to individuals who have chronic illnesses and are referred from hospitals and community health centers.

While the Great Recession and the COVID pandemic marked times of spiking need, that need never goes away, although it does fluctuate, Morehouse said.

“Inflation is coming down, and that might help … but folks are still struggling,” he added. “And, you know, we’re here to help them, give them a hand up.”

And at a higher level than ever before, thanks to an ambitious goal, some very entrepreneurial thinking, and a lot of community support.