Dena Hall Takes Regional President’s Role at United Bank

Dena Hall was talking about some of the many things that have changed since she was promoted to Western Mass. regional president at United Bank roughly a month ago.

Dena Hall was talking about some of the many things that have changed since she was promoted to Western Mass. regional president at United Bank roughly a month ago.

She said her phone calls are being returned more frequently and more promptly now. Meanwhile, she’s taking more calls, including some from people who want to know if the attractive positions that once dominated her business card — senior vice president of marketing and community relations and president of the United Bank Charitable Foundation, are “up for grabs.” They are not — she’ll still have those duties.

She said she’s had more invitations for lunch — often to hear requests for monetary donations, from a board member from the bank, or both — and has accepted a good number of them, a slight departure from her previous practice, because she desired to be in the office as much as possible.

And her 6-year-old son isn’t shy about telling anyone and everyone that his mother is now president of the bank. “He leaves off the word ‘regional,’ and we just him let him run with that,’” she said with a laugh.

But mostly, Hall, now arguably the highest-ranking female bank executive in the Western Mass. region, is focused mostly on what hasn’t changed.

“A lot of what I’m doing in this new role I was doing before, between my role with the United Bank Charitable Foundation and being involved in the community, because … that’s who I am,” she told BusinessWest. “I’ve always been one of the faces of the bank, and I’ve always been interacting with the community, fielding customer complaints and compliments. It was happening before; it’s just happening more now.”

Indeed, Hall doesn’t expect much of a learning curve as she moves on with life as regional president. But there is a lot to do as she takes this lead role with what is being called the ‘new United Bank.’

That’s the marketing term that’s been used since a merger of equals between United and Glastonbury, Conn.-based Rockville Financial was announced several months ago, and especially since the union became official on May 1. As with any merger of this type, there is change, she noted, and helping customers and employees understand and cope with it has become a big part of her job description.

“There’s a huge change-management component to what we’re going through right now,” she told BusinessWest. “It’s hard to change, and people need some leadership through change, and that’s one of the things we’ve been doing all along, as a team, and myself in particular — guiding the people here through the change process that’s happening, because some things are different.”

Overall, the task at hand is taking two roughly $2.5 billion banks and shaping them into an efficient, competitive, growth-driven $5 billion bank, a number that means different things to different people, she acknowledged.

“A lot of people have said we’ve turned into a big bank because we have $5 billion in assets,” Hall noted, referring specifically to the many community banks populating Western Mass. and Northern and Central Conn. “But we’re still so tiny when compared to Bank of America or Santander or even TD Bank. Our value proposition is that we create a good alternative to those banks. We’re big enough to manage all the necessary regulatory burdens that are put on us as a bank, but small enough to deliver that really good customer service.”

The broad goal for all those at the merged bank is realization of what Hall called a “new normal,” something that won’t be achieved until probably early next year after the second of two data conversions, this one involving Rockville Bank customers, is complete.

For this issue and its focus on banking and financial services, BusinessWest spoke at length with Hall about her new — and continuing — responsibilities with the bank, and how this process of establishing a new normal will play itself out.

Balance Statement

“Day 61.” That’s how, after doing some quick math, Hall referred to July 1, the day she spoke with BusinessWest.

That means it was the 61st day since the merger between United and Rockville became official, or legal. There was a lengthy countdown before May 1, she noted, and the day counting has gone on since, at least internally.

“We counted down to legal day 1 — from the time this merger was announced until the day the companies came together, there was a countdown, like ‘what do we need to do to get to legal day 1?’” she explained. “Now that we’ve hit that, and there were struggles — everyone has struggles coming together — we’re still counting, saying ‘this is day 14’ or ‘this is day 30 — let’s figure out how, by day 40, we can be in a better spot.’”

It was day 31 when it was announced by the new bank that Jeff Sullivan, then serving as the combined entity’s president, was leaving to pursue “other opportunities.” In the same press release, it was announced that Hall, who joined United just nine years earlier, would add the title ‘regional president’ to those she already had, and that Michael Moriarty, previously senior vice president and team leader, would become executive vice president and Western Mass. commercial banking executive.

Hall told BusinessWest that a press release was being readied to announce that she would be assuming the roles of ‘executive vice president and chief marketing officer’ and ‘head of Community Strategy,’ but Sullivan’s decision brought about a quick change of plans — and titles.

She acknowledged that Sullivan’s departure just a month or so after the merger became official was “certainly not ideal,” because Sullivan was, in many respects, the face of the old United Bank, or what she called the “legacy United,” which he served as executive vice president and chief operating officer, and also because it undoubtedly raised eyebrows concerning how well the banks were coming together as one.

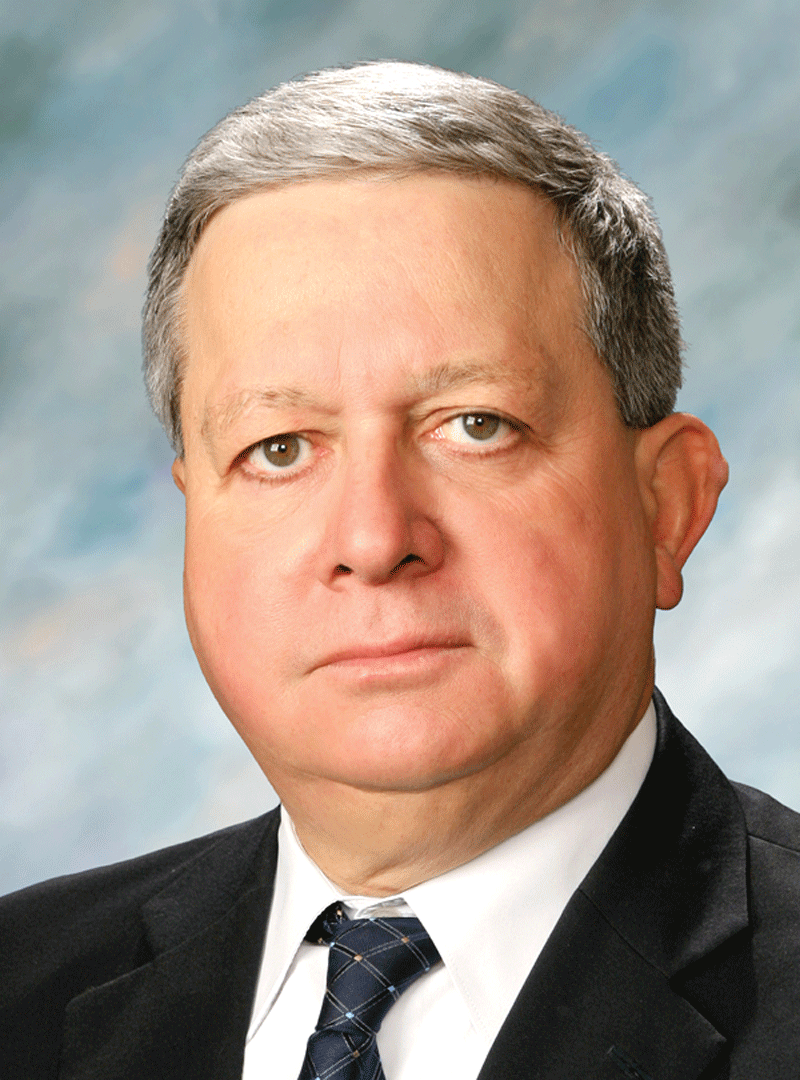

Dena Hall says that creating a “new normal” at what is being called the new United Bank is at the top of her current to-do list.

But she noted that, in mergers of equals, there are often differences of opinion about how the combined institution is to be managed, and this was this case with Sullivan’s decision to move on.

“Our merger of equals is so much different than a traditional acquisition, because you’re bringing two companies, two cultures, two management teams, and, in our case, two boards together,” she explained. “And in theory, we were evaluating the practices that each one had and taking the best one.

“What we learned, and what we’re still learning, is that what worked for a $2.5 billion bank isn’t going to work for a $5 billion bank growing to $7 billion, $9 billion, or $10 billion, wherever we go down the road,” she continued. “We’re still working through all the pieces that are necessary to build this new company, because we’re really building a new bank; we’re keeping what was good about both companies, but we’re building something new.”

Sullivan’s departure did leave a critical void in the form of a strong local presence in a top leadership role, said Hall, adding that William Crawford IV, the CEO of the new United and Robert Stewart Jr., chairman of the bank’s board, recognized the need to fill it.

“They decided that local presence and geographic leadership is important,” she noted. “And it’s particularly important here in Springfield, because when you look at the legacy United, 70% of our business is here in Springfield, so if there’s a place where we need some strong geographic leadership, especially at a time when the banks are merging, it’s in Springfield.”

Hall and Moriarty, serving in their respective roles, fill the void left by Sullivan’s departure and provide that geographic leadership, she said, adding that the bank’s decision to place her in the regional president’s position sends a clear message — actually, several of them.

For starters, it demonstrates that the bank is progressive — there are few women in top leadership positions at area banks, and none around Hall’s age — 40.

Also, the decision confirms the importance of this region to the merged bank moving forward.

“With mergers like this, jobs like this one often go out of the area,” she explained. “When there’s a merger, the geographic leader either comes in from the outside or the geographic leadership role goes away, and the president’s role goes somewhere else.

“The fact that our company has created this role, placed it in West Springfield, and given it to me speaks a lot for where the company is going,” she went on. “We’re both community banks with 120-plus years of history, but at the same time, we’re progressive, and we’re leaning toward maintaining our current customer base, but also attracting a younger customer base, going online, and going more mobile. Putting Mike and I in these roles when we’re both young and local makes a statement.”

Hall acknowledged that, traditionally, such positions within the banking industry have not gone to those from the marketing realm, but rather to commercial lenders. But the priority in all cases is to choose someone who knows the community and has created relationships within it.

“What banks are looking for in regional leaders now are people who are connected to the community — that’s the most important thing,” she noted. “Whenever you go through a merger, the automatic response is, ‘you’re leaving the community; you’re pulling out of the community.’ So regardless of the previous role, putting someone in this role who has a good connection in the community already is the driving factor behind making it successful.”

By All Accounts

It hasn’t rained much on Fridays in recent weeks, and that’s bad — in probably only one respect — because there’s a new policy in place at United’s regional operations facility in the center of West Springfield.

It’s called ‘rainy day Friday pizza,’ which pretty much says it all. If it rains on Friday — actually, even if it’s just cloudy and there’s a decent chance of rain — then Hall orders pizza for the entire building. OK, someone else does the ordering (probably 12 pizzas), and Hall pays the tab.

“This is something they do down in Glastonbury, and we thought it was kind of fun,” she told BusinessWest. “It’s only rained one Friday since we started it, but people really enjoy it. And it’s just one of the ways we’re trying to make sure that people feel valued in our new company and reaffirming to them that their role is still important even through perhaps their supervisor has changed or their job has changed.”

Implementing this new program — she’s also researching how to get a Ding Dong cart to stop by the headquarters building regularly — is clearly the least stressful of the myriad assignments facing Hall in her new role as regional president, and also with those other roles she still carries out.

Chief among them is leading the work to create that new normal she described, adding that this will be a work in progress as two bank cultures and two bank staffs are melded into one.

Hall has considerable experience with this, not only from when United acquired Worcester-based Commonwealth National Bank in 2009 and Enfield-based New England Bancshares in 2012, but also from when Woronoco Savings, which she served as assistant vice president and director of marketing, was acquired by Berkshire Bank a decade ago, a move that ultimately eliminated her job and prompted her to join United.

“I’m spending a lot of time helping people understand some of the things that are happening and why,” she told BusinessWest. “Communication is good at some levels and not so good at other levels, and decisions are made, and people may not understand why, and they instantly jump to the ‘blame the merger’ answer.

“It’s not usually ‘blame the merger,’” she went on, “but rather, ‘let’s look at the process and figure out what the best way is to accomplish what we need to accomplish, and if that means changing a process that we’ve had in place for a long time for the betterment of the organization, let’s have a conversation about it.’”

Creating greater efficiency is the ultimate goal with most of this change, she went on, adding that there have been some staffing reductions designed to eliminate redundancies across the board. And some operations have been moved, such as the loan center, which was relocated from West Springfield to South Windsor, Conn., and others that will be moved to West Springfield from Connecticut.

Beyond her work as change agent, Hall will play a key role in a rebranding initiative that will unfold in September. There will be a new logo and a new identity, she said, and not because of the merger, but because it was simply time for a new look.

“It’s time to give United Bank a facelift, and also position ourselves so that customers understand a little more about who we are, not necessarily here in Springfield, but in other areas,” she explained. “We have to make ourselves known in Connecticut. Because we just acquired New England Bank two years ago, no one really knows who we are; if you’re in one of the branch towns, like Cheshire or Southington, you know who United Bank is, but if you’re in West Hartford, you don’t know who United Bank or Rockville bank are.

“So we’re going to spend some time and money in Connecticut,” she went on, “making sure that everybody knows who United Bank is, what we do, what we offer, and why we’re a good alternative to the big banks.”

The new logo, which has been finalized but not unveiled, will be phased in, starting with the Rockville branches, which must become ‘United,’ by early October, said Hall, adding that there will be other changes, including new products, that are part and parcel of the process of becoming a new bank.

“We’re keeping some products and introducing new products, on both sides, so I’ll certainly have a number of conversations with people in the community and customers about the changes we’re making,” she said in conclusion. “And that’s OK. We need to have an open dialogue; I don’t every want someone to think they can’t walk in here and talk to any member of our staff about something that they’re feeling is not necessarily how they want it to be with their bank.”

Topping the List

As she talked with BusinessWest, Hall was getting ready to head out on a vacation for a few weeks. One of the things she did before leaving was make it clear who was responsible for ordering pizza if it rained on Friday.

That’s because continuing that new policy is one of the many components that go into the process of working through change and building a new bank.

In many respects, that process is just beginning, said Hall, noting while there will now be a number of titles crowding the business cards she’s awaiting, they can perhaps all be summed up with the phrase ‘change agent.’

It’s a role she’s excited about, and for all those reasons mentioned much earlier — from the phone calls being returned to her son getting some new bragging rights.

George O’Brien can be reached at [email protected]