Focus on the Fundamentals

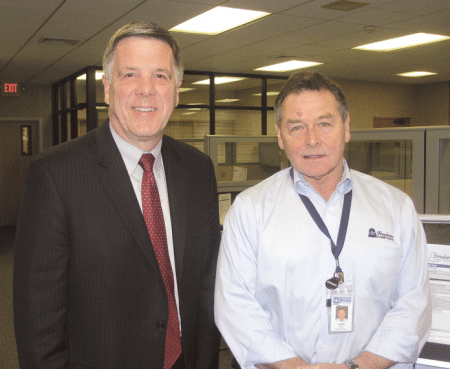

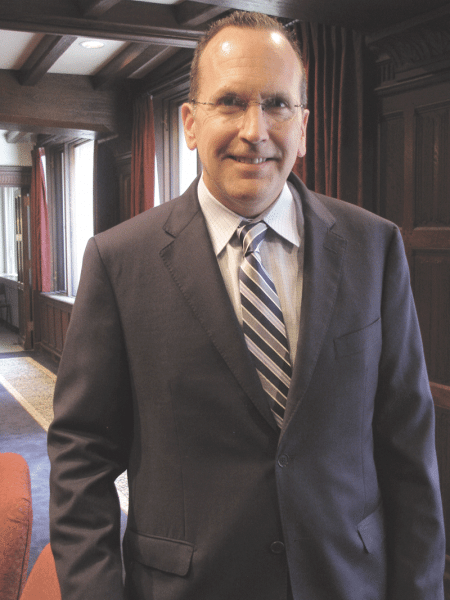

John Howland, far right, with team members (from left) Mark Grumoli, commercial loan officer, Denise Coyle, chief operating officer, and Tom Meshako, treasurer and chief financial officer.

Blocking and tackling.

Those are the fundamentals of winning football at any level, or so most coaches would say. But John Howland uses that phrase often as he talks about banking.

He uses it, as those on the gridiron do, in reference to maintaining a keen focus on the basics, the things one has to do right in order to achieve success. And in the case of financial institutions, that list includes some things that most would consider obvious — everything from good customer service to attractive products and services; from having competitive rates on those products to giving back within the community.

But there are also many items that fall into the category of ‘fundamentals’ that are perhaps less obvious, said Howland, president and CEO of Greenfield Savings Bank, a position he took roughly 16 months ago.

In that category would fall such things as imaginative new products, such as GSB’s ‘express business loan,’ a name that pretty much says it all (more on that later), as well as efforts to stay on the cutting edge of technology. Also fitting that description is the bank’s recent hosting of a meeting of the Franklin County Young Professionals Assoc. and other efforts to help foster leadership, as well as a somewhat related philosophy, said Denise Coyne, GSB’s executive vice president and COO, one centered on the notion that taking care of employees is as important as taking care of customers.

Then, there was the recent Asparagus Festival in Hadley, the town famous for its production of that vegetable. GSB was a sponsor of that event, said Howland, noting this alone constitutes blocking and tackling by supporting a local tradition and helping it continue. But the bank went further, renting additional space beyond that traditionally given to sponsors and awarding some of it to commercial customers who could benefit from the exposure and foot traffic.

“They were able to show their goods and gain awareness,” said Coyne. “It was a great opportunity for them, and for us as well, to show we’re working with businesses like that.

“We continue to do the blocking and tackling of banking — looking at updating technology, continually refining the offerings we have for our customers, and facilitating and expediting the interaction between the customer and the bank,” he added in an effort to sum things up. “We’re committed to organic growth through customer demand — it’s as simple as that.”

But there’s nothing inherently simple about executing all of that, and for this issue and its focus on banking and financial services, BusinessWest talked with several leaders at GSB about how it’s accomplished by a focus on fundamentals — and the expansion of that term as it applies to banking.

Sticking with the Game Plan

As he talked about his first 16 months at the helm and the bank’s broad strategic plan moving forward, Howland interspersed those thoughts with observations — and commentary — about the bank’s hometown of Greenfield.

Where once its economy was in many ways dominated by large manufacturers that employed hundreds who filled the downtown’s restaurants and lunch counters, it is now characterized by smaller businesses, many of them in an emerging ‘green’ energy sector as well as the centuries-old and still-stable agricultural sector.

“Going back 40 or 50 years, there might have been 30 or 40 fairly good-sized companies headquartered here,” he explained. “Most of those have consolidated and been rolled up into large, national organizations.

“What we see now is the next generation coming through,” he went on. “And this is in many areas — food service, manufacturing, green energy. We now have a large number of small companies that make product here and ship it elsewhere; we’ve created a new economy.”

In many respects, GSB is well-suited to meeting the needs of this changing business landscape, he said, adding that very large manufacturers would likely do business with a considerably larger institution. Meanwhile, the bank’s lending sweet spot and small-business focus positions it to serve these emerging ventures.

“We have an opportunity to fuel some of this growth,” he explained. “We can be the institution that can lend to these people when they need a piece of equipment or buy a piece of land. We can be there to assist them.”

That’s just one of many reasons why Howland and his team are optimistic about the prospects for the future — when it comes to the community and the bank. Both are at intriguing junctures in their history.

When he talked with BusinessWest soon after his arrival early last year, Howland, who came to Greenfield from First Bank of Greenwich, described the institution, and the cities and towns it served, with terms like ‘stability,’ ‘continuity,’ and ‘community-centered flavor,’ and what he’s seen and heard since has only reinforced those sentiments.

“This is a wonderful area, not just Greenfield but all of Franklin County,” he said, noting that he and his family have relocated there. “It’s an incredibly close-knit community, and one of the things I really like about this area is that multiple generations can live together; I’ve lived in areas where we have more transient populations where people come and people go. But in this part of the state, it’s not unusual to see parents and children living next door to each other. And that makes for a very special community.”

Later in that discussion with BusinessWest early last year, Howland said the bank was well-positioned for continued stability and growth because of its firm roots in the community, expanding commercial-loan portfolio, and presence in a region that was not as heavily banked — or ‘overbanked,’ as many would say — as other areas in Western Mass.

And, again, his experiences to date have only added figurative exclamation points to all of the above.

For these reasons, Howland said GSB doesn’t have to become preoccupied with gaining size and scale — as so many other institutions across the region have, as witnessed by the spate of mergers and acquisitions and rash of new branch openings — and remains focused on growing organically.

“Growth through acquisition is not really our strategy,” he continued. “We would consider an acquisition if we felt that it made sense, but we really are focused on enhancing our position within the markets that we serve and complementing the services we provide to our customers to expand our relationships with them.”

Gaining Ground

Overall, GSB is focused mostly on maintaining the status quo and growing market share across the spectrum of product lines — through more of that blocking and tackling.

“Our strategy is pretty straightforward, and there’s no magic to it, really; it’s about providing the best service we can provide for customers, and attracting both loans and deposits,” he explained. “There are no silver bullets, and no rabbits you can pull out of a hat.”

But there is plenty of room for innovation and creativity, he went on, pointing to products like the express business loan. Through the program, said Mark Grumoli, senior vice president and commercial loan officer, businesses can get up to $100,000, sometimes in 24 or 48 hours.

Products like this one have enabled the bank to maintain strong market share in Franklin County but also move well beyond ‘dabbling’ in neighboring Hampshire County and especially Northampton, a term he said he would apply a decade ago.

“Over the past eight years, much of the loan growth, especially on the commercial side, has come in Hampshire County,” he said, adding that this has been achieved through a combination of awareness, direct presence (new branches in Amherst and Northampton), and a relationship-driven focus.

There’s also — and this is quite timely — ‘Buy in July,’ a program the bank has staged for a quarter-century now that encourages homebuyers to step up during what is a traditionally the busiest time for that market through incentives such as a 25-year, biweekly product that is fairly unique.

“It’s programs like this that really help the mortgage department,” said Coyne, adding that, for the past 14 years, the bank has been the top residential lender in Franklin County and has registered 38% growth in that realm within neighboring Hampshire County. “It’s because of programs like this that really help borrowers out.”

But this business of blocking and tackling goes beyond products and services, said those we spoke with, a philosophy that brings Howland back to that meeting of the young professionals and, more importantly, a commitment that goes beyond making the lobby available for a meeting.

“We believe that this group is very important to the future of Franklin County,” he explained. “A lot of the outlying areas in the state, those outside the urban areas, are suffering from an aging population; in Amherst, the fastest-growing segment of the population is 80- to 90-year-olds.

“So we’re trying to support, in any we can, the environment for younger people in Franklin County,” he went on. “And we’re doing the same in Hampshire County. This is the kind of basic stuff a community bank needs to do. I’m not expecting any transactions out of this; it’s about building community and making the community stronger.”

Scoring Points

As he continued to talk about continuity and a desire to continue doing what the bank has always done, Howland pointed to the name over the door and on the stationery as perhaps the most visible example.

Indeed, at a time when almost every other institution has dropped the word ‘savings’ for one reason or another, GSB has no plans to follow suit.

“We were Greenfield Savings Bank then, and we’re Greenfield Savings Bank now,” he said, adding that this consistency has a lot to do with history, tradition, pride, and mission.

But also, it’s not really something that needs to be done to propel the bank forward and generate growth.

That assignment comes down to blocking and tackling — and the bank has no intention of losing its focus on those fundamentals.

George O’Brien can be reached at [email protected]

Instead, size is easily the most effective means with which to effectively cope with razor-thin margins and significantly deeper layers of regulation that resulted from the financial crisis — caused in good part by a lack of regulation of financial institutions — of nearly a decade ago.

Instead, size is easily the most effective means with which to effectively cope with razor-thin margins and significantly deeper layers of regulation that resulted from the financial crisis — caused in good part by a lack of regulation of financial institutions — of nearly a decade ago.

Here are some frequently asked questions to help explain the changes.

Here are some frequently asked questions to help explain the changes.