Mitigating Risk

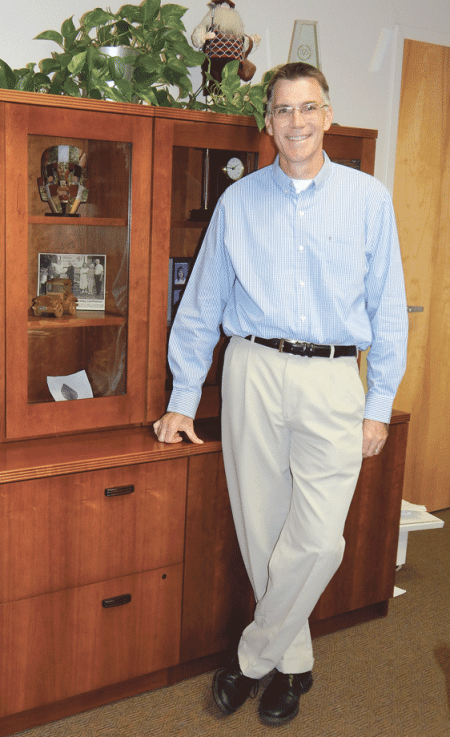

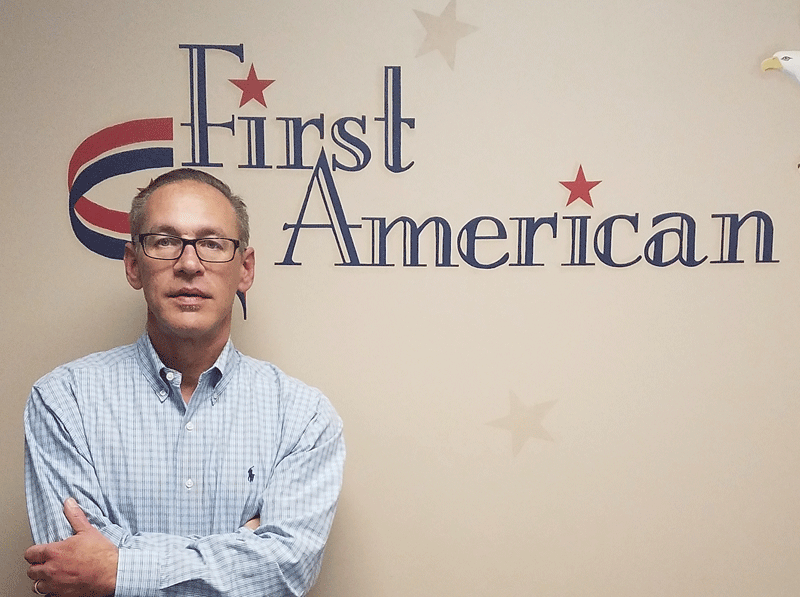

Robert Wilcox says the Team Concept program within Wilcox Insurance Agency has proved beneficial to clients.

While acknowledging that all insurance agencies strive for solid customer service, Robert Wilcox, the fourth-generation owner of the family business that bears his name, says he takes such efforts seriously, whether it’s monitoring how claims are handled, closely assessing risk to determine what clients need (or don’t need), or even running out to house fires at night. The goal, he said, is to use his experience to help others — and, in doing so, to help his agency stand out in a crowded field.

The call came at midnight.

Robert Wilcox was in bed, but when he heard the Westfield Fire Department was battling a blaze in a client’s multi-family house, he got up, went directly to the scene, and worked with the Red Cross to find a hotel to house the displaced tenants and answer all of their questions.

“I wanted to be right there; when a tragedy occurs, it’s part of my job to help people find some sort of peace of mind and comfort, reassure them that everything will be OK,” said the fourth-generation owner of Wilcox Insurance in Westfield and Agawam, adding that a second major fire had occurred a few days earlier, and he also went directly to that home.

In another instance, Wilcox went to battle for a client when an insurance claim was denied in a highly unusual situation. He told BusinessWest a tenant had died on the second floor of a two-story building, and there was more than $30,000 of damage as blood and body fluids had ruined the floors and carpeting and the stench permeated the unit.

“The insurance carrier tried to deny the claim on a pollution exclusion in the policy,” Wilcox said. “But I argued that it wasn’t pollution and got them to pay the claim.”

He cited a number of other situations when he went to bat for clients and won, including times when auto insurers didn’t want to pay for expensive parts needed to repair a vehicle.

“My goal is to do the right thing. Fighting for a client can involve a lot of frustration, but it’s worth it when I can hand them a check that relieves their anxiety,” Wilcox continued.

The father of six children aged 5 to 17 is very active in both the community and the insurance industry, and when the interview began, he immediately acknowledged that all insurance companies work hard to provide excellent customer service.

But rather than focusing on competitors or what the market is doing, Wilcox takes a different approach to business by focusing on how things are handled within his own agency, which ranges from monitoring phone calls and how claims are handled to alerting customers when changes need to be made to their policies or things such as accident forgiveness come into play, to closely assessing risk for new commercial clients by taking the time to understand exactly what they do and their ensuing exposure to risk.

“The ultimate purpose in life is to use your experience to help others. It’s all about being helpful, which is my goal,” Wilcox said.

For this issue and its focus on insurance, BusinessWest looks at the history of this family-owned company and the creative measures that have been instituted to ensure the agency continues to thrive in a time when polices sold via the Internet, or through TV ads generated by direct writers such as Allstate and Nationwide, have made competition especially fierce.

Storied History

Wilcox’s great grandfather, the late Raymond Wilcox, was a tobacco farmer before he founded Westfield Mutual Insurance Agency Inc.

The reason for his career change was devastation: his farm was hit by two hailstorms, and although he recovered from the first one, the second one marked the end of his business.

“At that point, he began knocking on doors and selling insurance,” Robert said, adding that Raymond opened his own insurance firm on Sept. 1, 1923.

In 1937, he was joined by his son, Malcolm Wilcox, and during the ’40s and ’50s, the agency underwent remarkable growth.

“My father, Scott Wilcox, came on board in 1962, and when I started in 1990, my grandfather was still working,” Robert recalled, adding that, when his dad retired in 2012, he bought the business from him.

His own entry into the firm came when he was a college student. He was living independently, and when he found he was $40 short of meeting his expenses each month, he called his father to ask for help and was told to show up at the agency on Monday morning.

Wilcox said he began working part-time, and has been at the agency ever since. He literally started at the bottom, sweeping the basement, and continued his college career while he worked, eventually earning an associate’s degree in business studies from Holyoke Community College and a bachelor’s degree in finance from Westfield State College.

Wilcox earned his license to sell insurance in 1993, and as his love for the business grew, he became active in the industry. Today, his history of service includes stints as president of the Independent Insurance Agents of Hampden County and the Massachusetts/Rhode Island User Group of Applied Systems.

In 1997, Wilcox and his father purchased Pomeroy Insurance Agency and Clem Insurance Agency, followed by Palczynski Insurance Agency in 2000. All three of these businesses were in Westfield, and in 2002, the name of the agency was changed to reflect how most of clients referred to the them, as well as the fact that they wrote so much business outside of Westfield.

“We didn’t want our image to limit our reach to Westfield only,” Robert said. “It also fit our goal to acquire other agencies outside of Westfield.”

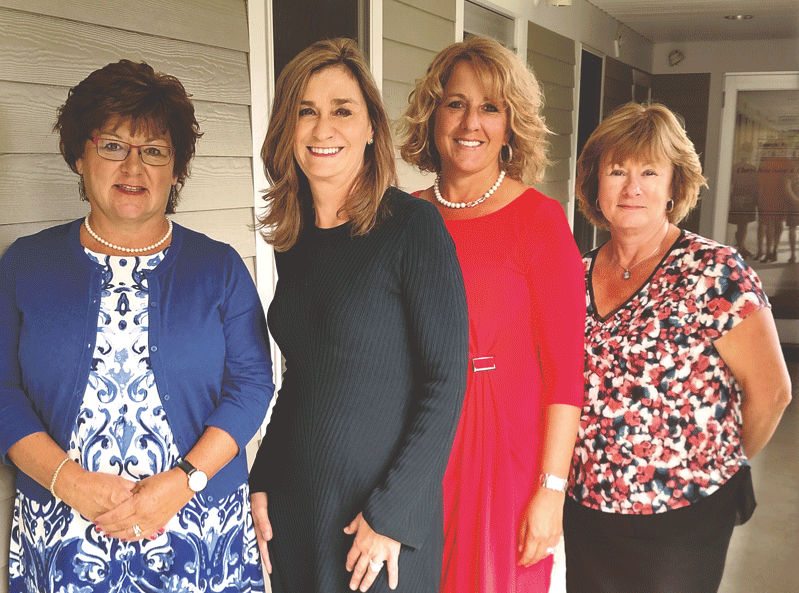

Members of the Team Concept program get together each month and go over practices that need to be continued and others that can be improved in order to provide the best service possible to customers.

In 2005 he built a new office for the company at its present location on Broad Street. The following year he acquired Foley Insurance Agency in Feeding Hills, and four years later he built a new office in Agawam to provide service for his agency’s new customers.

“My focus is on growth through acquisition, and I hope to be able to acquire additional agencies,” he told BusinessWest, adding that he has great respect for the companies he’s purchased.

The cornerstone of his own success is based on applying knowledge gleaned from personal experience and certifications to make sure each client has the coverage they need to fit their individual situations.

To that end, Wilcox and his employees inform current clients about any changes they may need to make to their policies, and spend an unusual amount of time working to determine exactly what each new client needs, which is especially important for commercial accounts due to their differing operations.

“You need to understand everything a business does, in addition to conducting a survey of their equipment and property,” Wilcox said, adding that he is a certified insurance counselor and licensed insurance advisor, and although few people in Western Mass. hold that designation, he chose to pursue it to increase his knowledge of risk assessment.

To that end, he learns all he can about a business and how it operates to make sure policies don’t contain exclusions that could prove costly. For example, a business that cleans carpets on site and offers storage needs accident coverage that doesn’t exclude the property of others.

The goal is to serve the client in the best way possible, and in some cases a close investigation can result in lower premiums. For example, Wilcox gained a client after talking to him about the 20-plus buildings he owned that contained 127 residential units.

“He had been told that he had to carry insurance on all of the buildings and wanted to know if he could self-insure the structures he owned outright,” Wilcox said, explaining that, although he needed liability insurance for every rental property, he did not need to insure buildings without a mortgage.

Since the prospect wasn’t concerned about losing buildings he owned to fire or other catastrophic events, he was able to save thousands in premiums.

“We are not a hard-sell agency; our approach is to build relationships and protect assets by understanding the client’s exposures and tailoring coverage to meet those needs,” he explained.

Innovative Change

Eighteen months ago, Wilcox devised a pilot program based on leadership that he designed to increase responsibility, determine practices that work well and should be continued, and examine instances where change could result in better customer service.

The program is called the Wilcox Service Team Concept, and four key account managers take turns acting as the team leader through a monthly rotation process. There are guidelines that promote objectivity and prevent judgment from occurring as they review situations that occurred during the month.

“It’s easy for employees in a small office to focus on what others are doing instead of looking at their own work,” he explained. “But our team works together for the betterment of clients.

“We focus on excellence; everything that is discussed is considered a teaching moment and is brought up from the position of being helpful,” he went on, adding that he wants his team to continuously think of innovative ways to serve clients and stay relevant in today’s business world.

Wilcox doesn’t attend most meetings; he considers himself a leader but trusts his employees and wants them to become leaders themselves.

Account Manager Lisa Fox finds Team Concept beneficial, and enjoys the fact that account managers do all they can to help one another, which she finds significant, as she never received any help when she worked in the claims department of two large, multiline carriers before coming to Wilcox.

“We’re comfortable bouncing ideas off one another and asking each other for help; we all have our own strengths, and Team Concept has really given us a chance to see what has worked well and where we can do better,” she told BusinessWest, adding that sharing information is educational for everyone.

For example, a client recently wanted to get a homemade trailer registered. It was never a problem in the past; the Registry of Motor Vehicles had complied with similar requests after they saw store receipts listing parts purchased to create the trailer. But in this instance, the client used parts that he already owned, which included a chassis with a serial number that the Wilcox agent found had to be traced.

Fox said sharing information about how to handle similar requests in the future prove educational to everyone concerned. “The team approach really brings things to light and has benefittd the agency.”

Marylinda Kruzel agrees. “I have never worked for a place that had anything like the Team Concept,” said the commercial lines account manager. “It took time to structure our thinking and keep to the facts without judgment during meetings, but it has resulted in open communication throughout the month as we aim to provide unified service to clients. We strive to handle every scenario in a way that is best for the client.”

Mary Russell added that Team Concept has led the agents to trust each other’s knowledge and abilities. “We always focus on the positive and how we can help the client,” she noted, citing an instance where it was pointed out that the time a client spent at the agency might have been shorter if the application process had been completed during a phone interview.

Such changes can be accomplished in a matter of minutes, but Wilcox is happy with the outcome. “The team members are thinking on an entirely different level than they were when they were just doing the job in front of them,” he noted.

Legacy of Service

Wilcox describes his 26 years in the insurance industry as a “very rich experience” and is grateful for what he has learned from his customers, knowledge gained from acquiring other companies and during the building process, and the relationships he has formed on the job and in the community, as service has been a long-standing family tradition.

He was a member of the Rotary Club of Westfield from 1995 to 2009 and served several terms on its board of directors, and is treasurer for Sarah Gillette Services for the Elderly and a trustee to Noble Visiting Nurse and Hospice Services.

“All of this experience has led the company to where we are today; we are not here to sell people policies, but to share our experiences with others and be helpful,” he explained. “No one knows where a business will end up, but I believe independent insurance agencies will continue operating in the future, and I want to make sure I am one of them.”

Which seems likely as the team works with Wilcox to perpetuate a legacy that began almost 100 years ago when his great-grandfather set out to help others after suffering his own devastating loss.

“No one plans on having anything bad happen,”Wilcox said, “but if it does, we want to make sure they have the right coverage.”

The story is a familiar one by now: hospitals across the U.S., hammered by COVID-19, began directing resources toward fighting the pandemic last spring and curtailed elective and non-emergency procedures. Meanwhile, patients, even when sick, stayed away from medical practices out of fear of infection.

The story is a familiar one by now: hospitals across the U.S., hammered by COVID-19, began directing resources toward fighting the pandemic last spring and curtailed elective and non-emergency procedures. Meanwhile, patients, even when sick, stayed away from medical practices out of fear of infection.

In the insurance world, an umbrella policy is exactly what it sounds like, sitting atop home, auto, and business insurance coverage and providing excess protection against liability risks. What is less clear, area insurance experts say, is why more people don’t avail themselves of this relatively inexpensive vehicle. After all, life’s storms can strike at any time, and when they do, no one wants to be totally exposed.

In the insurance world, an umbrella policy is exactly what it sounds like, sitting atop home, auto, and business insurance coverage and providing excess protection against liability risks. What is less clear, area insurance experts say, is why more people don’t avail themselves of this relatively inexpensive vehicle. After all, life’s storms can strike at any time, and when they do, no one wants to be totally exposed.

Gov. Charlie Baker announced that the

Gov. Charlie Baker announced that the

While major data breaches at national companies justifiably make news, small businesses may not recognize that hackers target businesses of all sizes and types. But awareness is on the rise, especially as insurance companies hone their products aimed at protecting against cyber threats — and help clients understand that buying insurance is only one line of defense, and that complete protection requires in-house diligence, too.

While major data breaches at national companies justifiably make news, small businesses may not recognize that hackers target businesses of all sizes and types. But awareness is on the rise, especially as insurance companies hone their products aimed at protecting against cyber threats — and help clients understand that buying insurance is only one line of defense, and that complete protection requires in-house diligence, too.

Winter weather brings a host of insurance risks to homes and businesses, from ice dams wreaking havoc on a building’s interior to frozen and burst pipes causing serious water damage, to liability issues if someone falls on the ice on the front sidewalk. Insurance policies help protect property owners against exposure to such events, but just as important are common-sense preparations to minimize such risks in the first place.

Winter weather brings a host of insurance risks to homes and businesses, from ice dams wreaking havoc on a building’s interior to frozen and burst pipes causing serious water damage, to liability issues if someone falls on the ice on the front sidewalk. Insurance policies help protect property owners against exposure to such events, but just as important are common-sense preparations to minimize such risks in the first place.

Mention insurance to someone, and chances are they’ll think of buying a certain level of coverage against loss, damage, or other adverse events. But when it comes to business insurance, that’s just one aspect of protecting a company. Just as important is risk management, which is essentially the process of implementing steps to reduce the probability of such dangers. It’s a win-win effort that saves money for both insurance companies and their clients — and often saves lives, too.

Mention insurance to someone, and chances are they’ll think of buying a certain level of coverage against loss, damage, or other adverse events. But when it comes to business insurance, that’s just one aspect of protecting a company. Just as important is risk management, which is essentially the process of implementing steps to reduce the probability of such dangers. It’s a win-win effort that saves money for both insurance companies and their clients — and often saves lives, too.